{"title":"加密资产:现行《国际财务报告准则》框架下的定义和会计处理方法","authors":"Luz Parrondo","doi":"10.1002/isaf.1543","DOIUrl":null,"url":null,"abstract":"<p>This paper provides a first comprehensive definition of cryptoassets for accounting purposes in the types of payment tokens, electronic money (e-money) tokens, utility tokens and security tokens. The delivery of definitions for accounting purposes addresses some of the concerns raised by the European Financial Reporting Advisory Group (EFRAG) discussion paper and helps accounting regulators adapt current International Financial Reporting Standards (IFRS) standards to blockchain-based tokens' taxonomy and nature. The paper helps policymakers reconcile Markets in Cryptoassets Regulation Proposal's (MiCA) definitions and classification of cryptoassets with the EFRAG's specific needs for clarification and/or amendment in the IFRS standards and contributes to providing an accounting guide for practitioners in their financial disclosure.</p>","PeriodicalId":53473,"journal":{"name":"Intelligent Systems in Accounting, Finance and Management","volume":"30 4","pages":"208-227"},"PeriodicalIF":0.0000,"publicationDate":"2023-12-06","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1002/isaf.1543","citationCount":"0","resultStr":"{\"title\":\"Cryptoassets: Definitions and accounting treatment under the current International Financial Reporting Standards framework\",\"authors\":\"Luz Parrondo\",\"doi\":\"10.1002/isaf.1543\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>This paper provides a first comprehensive definition of cryptoassets for accounting purposes in the types of payment tokens, electronic money (e-money) tokens, utility tokens and security tokens. The delivery of definitions for accounting purposes addresses some of the concerns raised by the European Financial Reporting Advisory Group (EFRAG) discussion paper and helps accounting regulators adapt current International Financial Reporting Standards (IFRS) standards to blockchain-based tokens' taxonomy and nature. The paper helps policymakers reconcile Markets in Cryptoassets Regulation Proposal's (MiCA) definitions and classification of cryptoassets with the EFRAG's specific needs for clarification and/or amendment in the IFRS standards and contributes to providing an accounting guide for practitioners in their financial disclosure.</p>\",\"PeriodicalId\":53473,\"journal\":{\"name\":\"Intelligent Systems in Accounting, Finance and Management\",\"volume\":\"30 4\",\"pages\":\"208-227\"},\"PeriodicalIF\":0.0000,\"publicationDate\":\"2023-12-06\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://onlinelibrary.wiley.com/doi/epdf/10.1002/isaf.1543\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Intelligent Systems in Accounting, Finance and Management\",\"FirstCategoryId\":\"1085\",\"ListUrlMain\":\"https://onlinelibrary.wiley.com/doi/10.1002/isaf.1543\",\"RegionNum\":0,\"RegionCategory\":null,\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q1\",\"JCRName\":\"Economics, Econometrics and Finance\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Intelligent Systems in Accounting, Finance and Management","FirstCategoryId":"1085","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1002/isaf.1543","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q1","JCRName":"Economics, Econometrics and Finance","Score":null,"Total":0}

Cryptoassets: Definitions and accounting treatment under the current International Financial Reporting Standards framework

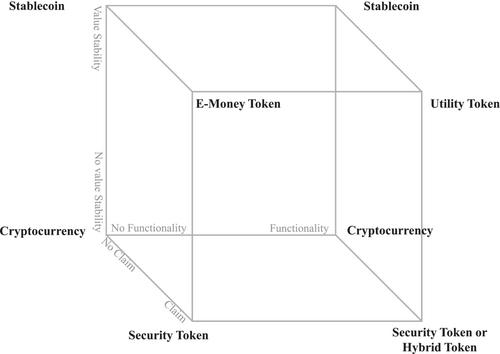

This paper provides a first comprehensive definition of cryptoassets for accounting purposes in the types of payment tokens, electronic money (e-money) tokens, utility tokens and security tokens. The delivery of definitions for accounting purposes addresses some of the concerns raised by the European Financial Reporting Advisory Group (EFRAG) discussion paper and helps accounting regulators adapt current International Financial Reporting Standards (IFRS) standards to blockchain-based tokens' taxonomy and nature. The paper helps policymakers reconcile Markets in Cryptoassets Regulation Proposal's (MiCA) definitions and classification of cryptoassets with the EFRAG's specific needs for clarification and/or amendment in the IFRS standards and contributes to providing an accounting guide for practitioners in their financial disclosure.

期刊介绍:

Intelligent Systems in Accounting, Finance and Management is a quarterly international journal which publishes original, high quality material dealing with all aspects of intelligent systems as they relate to the fields of accounting, economics, finance, marketing and management. In addition, the journal also is concerned with related emerging technologies, including big data, business intelligence, social media and other technologies. It encourages the development of novel technologies, and the embedding of new and existing technologies into applications of real, practical value. Therefore, implementation issues are of as much concern as development issues. The journal is designed to appeal to academics in the intelligent systems, emerging technologies and business fields, as well as to advanced practitioners who wish to improve the effectiveness, efficiency, or economy of their working practices. A special feature of the journal is the use of two groups of reviewers, those who specialize in intelligent systems work, and also those who specialize in applications areas. Reviewers are asked to address issues of originality and actual or potential impact on research, teaching, or practice in the accounting, finance, or management fields. Authors working on conceptual developments or on laboratory-based explorations of data sets therefore need to address the issue of potential impact at some level in submissions to the journal.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们