{"title":"反映几何布朗运动的套利问题","authors":"Dean Buckner, Kevin Dowd, Hardy Hulley","doi":"10.1007/s00780-023-00525-x","DOIUrl":null,"url":null,"abstract":"<p>Contrary to the claims made by several authors, a financial market model in which the price of a risky security follows a reflected geometric Brownian motion is not arbitrage-free. In fact, such models violate even the weakest no-arbitrage condition considered in the literature. Consequently, they do not admit numéraire portfolios or equivalent risk-neutral probability measures, which makes them unsuitable for contingent claim valuation. Unsurprisingly, the published option pricing formulae for such models violate classical no-arbitrage bounds.</p>","PeriodicalId":50447,"journal":{"name":"Finance and Stochastics","volume":"70 1","pages":""},"PeriodicalIF":1.6000,"publicationDate":"2023-12-20","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"","citationCount":"0","resultStr":"{\"title\":\"Arbitrage problems with reflected geometric Brownian motion\",\"authors\":\"Dean Buckner, Kevin Dowd, Hardy Hulley\",\"doi\":\"10.1007/s00780-023-00525-x\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>Contrary to the claims made by several authors, a financial market model in which the price of a risky security follows a reflected geometric Brownian motion is not arbitrage-free. In fact, such models violate even the weakest no-arbitrage condition considered in the literature. Consequently, they do not admit numéraire portfolios or equivalent risk-neutral probability measures, which makes them unsuitable for contingent claim valuation. Unsurprisingly, the published option pricing formulae for such models violate classical no-arbitrage bounds.</p>\",\"PeriodicalId\":50447,\"journal\":{\"name\":\"Finance and Stochastics\",\"volume\":\"70 1\",\"pages\":\"\"},\"PeriodicalIF\":1.6000,\"publicationDate\":\"2023-12-20\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Finance and Stochastics\",\"FirstCategoryId\":\"96\",\"ListUrlMain\":\"https://doi.org/10.1007/s00780-023-00525-x\",\"RegionNum\":2,\"RegionCategory\":\"经济学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q3\",\"JCRName\":\"BUSINESS, FINANCE\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Finance and Stochastics","FirstCategoryId":"96","ListUrlMain":"https://doi.org/10.1007/s00780-023-00525-x","RegionNum":2,"RegionCategory":"经济学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q3","JCRName":"BUSINESS, FINANCE","Score":null,"Total":0}

Arbitrage problems with reflected geometric Brownian motion

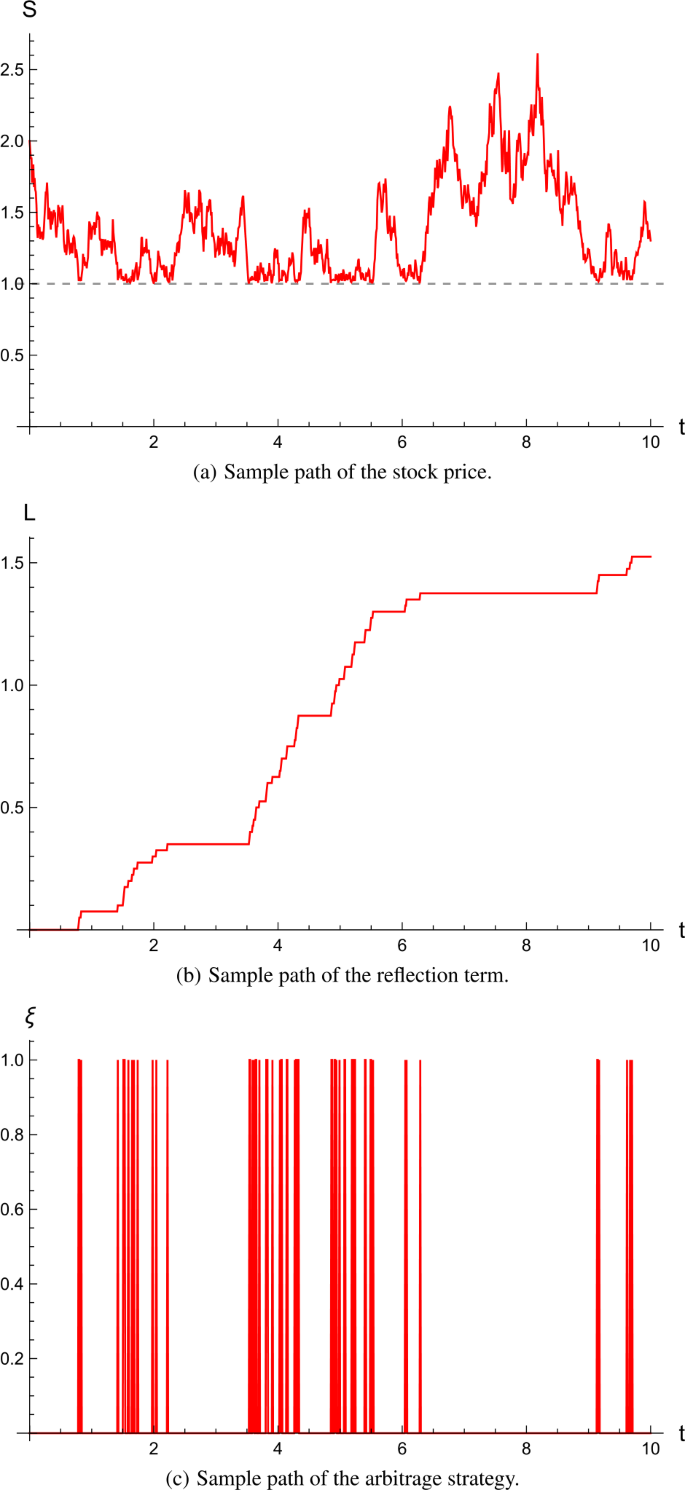

Contrary to the claims made by several authors, a financial market model in which the price of a risky security follows a reflected geometric Brownian motion is not arbitrage-free. In fact, such models violate even the weakest no-arbitrage condition considered in the literature. Consequently, they do not admit numéraire portfolios or equivalent risk-neutral probability measures, which makes them unsuitable for contingent claim valuation. Unsurprisingly, the published option pricing formulae for such models violate classical no-arbitrage bounds.

期刊介绍:

The purpose of Finance and Stochastics is to provide a high standard publication forum for research

- in all areas of finance based on stochastic methods

- on specific topics in mathematics (in particular probability theory, statistics and stochastic analysis) motivated by the analysis of problems in finance.

Finance and Stochastics encompasses - but is not limited to - the following fields:

- theory and analysis of financial markets

- continuous time finance

- derivatives research

- insurance in relation to finance

- portfolio selection

- credit and market risks

- term structure models

- statistical and empirical financial studies based on advanced stochastic methods

- numerical and stochastic solution techniques for problems in finance

- intertemporal economics, uncertainty and information in relation to finance.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们