{"title":"对 \"高层基调 \"评估中审计员假设检验策略的研究:诊断性知识结构的证据","authors":"Regan N. Schmidt","doi":"10.1111/ijau.12340","DOIUrl":null,"url":null,"abstract":"<p>This study examines the tests auditors design to assess a client's ‘tone at the top’. By exploiting conceptual differences in the constructs of ethicality and competence, the study investigates auditor knowledge structures by disentangling auditor hypothesis testing strategies. The results of an experiment document that auditors design tests to yield evidence of unethical and competent, rather than ethical and incompetent, client management behaviour. This overall pattern of results, and in particular auditors' focus on seeking evidence of client management competence, is consistent with a diagnostic hypothesis testing strategy and is not consistent with a conservative testing strategy. Collectively, these results provide insights into how auditors' ‘tone at the top’ knowledge is organized and used.</p>","PeriodicalId":47092,"journal":{"name":"International Journal of Auditing","volume":"28 3","pages":"562-581"},"PeriodicalIF":1.4000,"publicationDate":"2024-01-15","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1111/ijau.12340","citationCount":"0","resultStr":"{\"title\":\"An examination of auditor hypothesis testing strategies in ‘tone at the top’ evaluations: Evidence of diagnostic knowledge structures\",\"authors\":\"Regan N. Schmidt\",\"doi\":\"10.1111/ijau.12340\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>This study examines the tests auditors design to assess a client's ‘tone at the top’. By exploiting conceptual differences in the constructs of ethicality and competence, the study investigates auditor knowledge structures by disentangling auditor hypothesis testing strategies. The results of an experiment document that auditors design tests to yield evidence of unethical and competent, rather than ethical and incompetent, client management behaviour. This overall pattern of results, and in particular auditors' focus on seeking evidence of client management competence, is consistent with a diagnostic hypothesis testing strategy and is not consistent with a conservative testing strategy. Collectively, these results provide insights into how auditors' ‘tone at the top’ knowledge is organized and used.</p>\",\"PeriodicalId\":47092,\"journal\":{\"name\":\"International Journal of Auditing\",\"volume\":\"28 3\",\"pages\":\"562-581\"},\"PeriodicalIF\":1.4000,\"publicationDate\":\"2024-01-15\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://onlinelibrary.wiley.com/doi/epdf/10.1111/ijau.12340\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"International Journal of Auditing\",\"FirstCategoryId\":\"91\",\"ListUrlMain\":\"https://onlinelibrary.wiley.com/doi/10.1111/ijau.12340\",\"RegionNum\":4,\"RegionCategory\":\"管理学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q2\",\"JCRName\":\"BUSINESS, FINANCE\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"International Journal of Auditing","FirstCategoryId":"91","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1111/ijau.12340","RegionNum":4,"RegionCategory":"管理学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q2","JCRName":"BUSINESS, FINANCE","Score":null,"Total":0}

An examination of auditor hypothesis testing strategies in ‘tone at the top’ evaluations: Evidence of diagnostic knowledge structures

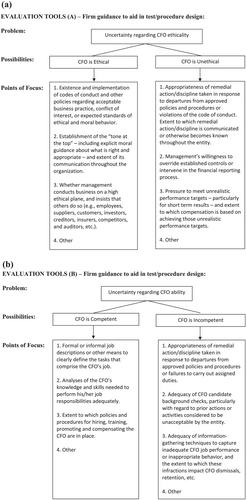

This study examines the tests auditors design to assess a client's ‘tone at the top’. By exploiting conceptual differences in the constructs of ethicality and competence, the study investigates auditor knowledge structures by disentangling auditor hypothesis testing strategies. The results of an experiment document that auditors design tests to yield evidence of unethical and competent, rather than ethical and incompetent, client management behaviour. This overall pattern of results, and in particular auditors' focus on seeking evidence of client management competence, is consistent with a diagnostic hypothesis testing strategy and is not consistent with a conservative testing strategy. Collectively, these results provide insights into how auditors' ‘tone at the top’ knowledge is organized and used.

期刊介绍:

In addition to communicating the results of original auditing research, the International Journal of Auditing also aims to advance knowledge in auditing by publishing critiques, thought leadership papers and literature reviews on specific aspects of auditing. The journal seeks to publish articles that have international appeal either due to the topic transcending national frontiers or due to the clear potential for readers to apply the results or ideas in their local environments. While articles must be methodologically and theoretically sound, any research orientation is acceptable. This means that papers may have an analytical and statistical, behavioural, economic and financial (including agency), sociological, critical, or historical basis. The editors consider articles for publication which fit into one or more of the following subject categories: • Financial statement audits • Public sector/governmental auditing • Internal auditing • Audit education and methods of teaching auditing (including case studies) • Audit aspects of corporate governance, including audit committees • Audit quality • Audit fees and related issues • Environmental, social and sustainability audits • Audit related ethical issues • Audit regulation • Independence issues • Legal liability and other legal issues • Auditing history • New and emerging audit and assurance issues

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们