{"title":"广泛正交依存样本下尾部风险价值估计器的强一致性及相应的一般结果","authors":"Jinyu Zhou, Jigao Yan, Dongya Cheng","doi":"10.1007/s00362-023-01525-x","DOIUrl":null,"url":null,"abstract":"<p>In this paper, strong consistency of tail value-at-risk (TVaR) estimator under widely orthant dependent (WOD) samples is established, and a numerical simulation is performed to verify the validity of the theoretical results. To reveal the essence of the result, theoretical discussion on complete and complete moment convergence corresponding to the Baum–Katz law, as well as the Marcinkiewicz–Zygmund type strong law of large numbers (MZSLLN) for maximal weighted sums and maximal product sums of widely orthant dependent (WOD) random variables are investigated. The results obtained in the context extend the corresponding ones for independent and some dependent random variables.</p>","PeriodicalId":51166,"journal":{"name":"Statistical Papers","volume":"1 1","pages":""},"PeriodicalIF":1.1000,"publicationDate":"2024-01-17","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"","citationCount":"0","resultStr":"{\"title\":\"Strong consistency of tail value-at-risk estimator and corresponding general results under widely orthant dependent samples\",\"authors\":\"Jinyu Zhou, Jigao Yan, Dongya Cheng\",\"doi\":\"10.1007/s00362-023-01525-x\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>In this paper, strong consistency of tail value-at-risk (TVaR) estimator under widely orthant dependent (WOD) samples is established, and a numerical simulation is performed to verify the validity of the theoretical results. To reveal the essence of the result, theoretical discussion on complete and complete moment convergence corresponding to the Baum–Katz law, as well as the Marcinkiewicz–Zygmund type strong law of large numbers (MZSLLN) for maximal weighted sums and maximal product sums of widely orthant dependent (WOD) random variables are investigated. The results obtained in the context extend the corresponding ones for independent and some dependent random variables.</p>\",\"PeriodicalId\":51166,\"journal\":{\"name\":\"Statistical Papers\",\"volume\":\"1 1\",\"pages\":\"\"},\"PeriodicalIF\":1.1000,\"publicationDate\":\"2024-01-17\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Statistical Papers\",\"FirstCategoryId\":\"100\",\"ListUrlMain\":\"https://doi.org/10.1007/s00362-023-01525-x\",\"RegionNum\":3,\"RegionCategory\":\"数学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q2\",\"JCRName\":\"STATISTICS & PROBABILITY\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Statistical Papers","FirstCategoryId":"100","ListUrlMain":"https://doi.org/10.1007/s00362-023-01525-x","RegionNum":3,"RegionCategory":"数学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q2","JCRName":"STATISTICS & PROBABILITY","Score":null,"Total":0}

Strong consistency of tail value-at-risk estimator and corresponding general results under widely orthant dependent samples

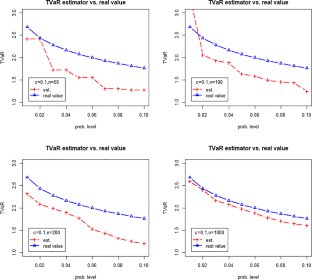

In this paper, strong consistency of tail value-at-risk (TVaR) estimator under widely orthant dependent (WOD) samples is established, and a numerical simulation is performed to verify the validity of the theoretical results. To reveal the essence of the result, theoretical discussion on complete and complete moment convergence corresponding to the Baum–Katz law, as well as the Marcinkiewicz–Zygmund type strong law of large numbers (MZSLLN) for maximal weighted sums and maximal product sums of widely orthant dependent (WOD) random variables are investigated. The results obtained in the context extend the corresponding ones for independent and some dependent random variables.

期刊介绍:

The journal Statistical Papers addresses itself to all persons and organizations that have to deal with statistical methods in their own field of work. It attempts to provide a forum for the presentation and critical assessment of statistical methods, in particular for the discussion of their methodological foundations as well as their potential applications. Methods that have broad applications will be preferred. However, special attention is given to those statistical methods which are relevant to the economic and social sciences. In addition to original research papers, readers will find survey articles, short notes, reports on statistical software, problem section, and book reviews.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们