Luigi De Cesare, Lucianna Cananà, Tiziana Ciano, Massimiliano Ferrara

{"title":"用最优停止法建立融资租赁模型","authors":"Luigi De Cesare, Lucianna Cananà, Tiziana Ciano, Massimiliano Ferrara","doi":"10.1007/s10203-023-00429-7","DOIUrl":null,"url":null,"abstract":"<p>Leasing valuation is a topic that has aroused considerable interest in business circles. This paper examines leasing from the point of view of the lessor who can decide to leave the contract due to default. We analyze in introducing a model in which the lessor decides whether or not to terminate the contract at a given point in time, comparing it with the cost of capital of alternative investments. The proposed model is stochastic, and it is strongly based on correlated random walks, making it more adaptable to real-world circumstances. Furthermore, we propose a recombinant binomial tree based on correlated random walks, performing numerical simulations starting from CIR and Vasicek models. We will point out that as the rate of cost of capital of an alternative investment increases, the optimal boundary curve decreases, so the lessor leaves, while as the past interest rates increases, the curve rises and the lessor will have a concrete interest in maintaining the contract.</p>","PeriodicalId":43711,"journal":{"name":"Decisions in Economics and Finance","volume":"11 1","pages":""},"PeriodicalIF":0.7000,"publicationDate":"2024-01-22","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"","citationCount":"0","resultStr":"{\"title\":\"Modeling financial leasing by optimal stopping approach\",\"authors\":\"Luigi De Cesare, Lucianna Cananà, Tiziana Ciano, Massimiliano Ferrara\",\"doi\":\"10.1007/s10203-023-00429-7\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>Leasing valuation is a topic that has aroused considerable interest in business circles. This paper examines leasing from the point of view of the lessor who can decide to leave the contract due to default. We analyze in introducing a model in which the lessor decides whether or not to terminate the contract at a given point in time, comparing it with the cost of capital of alternative investments. The proposed model is stochastic, and it is strongly based on correlated random walks, making it more adaptable to real-world circumstances. Furthermore, we propose a recombinant binomial tree based on correlated random walks, performing numerical simulations starting from CIR and Vasicek models. We will point out that as the rate of cost of capital of an alternative investment increases, the optimal boundary curve decreases, so the lessor leaves, while as the past interest rates increases, the curve rises and the lessor will have a concrete interest in maintaining the contract.</p>\",\"PeriodicalId\":43711,\"journal\":{\"name\":\"Decisions in Economics and Finance\",\"volume\":\"11 1\",\"pages\":\"\"},\"PeriodicalIF\":0.7000,\"publicationDate\":\"2024-01-22\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Decisions in Economics and Finance\",\"FirstCategoryId\":\"1085\",\"ListUrlMain\":\"https://doi.org/10.1007/s10203-023-00429-7\",\"RegionNum\":0,\"RegionCategory\":null,\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q3\",\"JCRName\":\"SOCIAL SCIENCES, MATHEMATICAL METHODS\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Decisions in Economics and Finance","FirstCategoryId":"1085","ListUrlMain":"https://doi.org/10.1007/s10203-023-00429-7","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q3","JCRName":"SOCIAL SCIENCES, MATHEMATICAL METHODS","Score":null,"Total":0}

Modeling financial leasing by optimal stopping approach

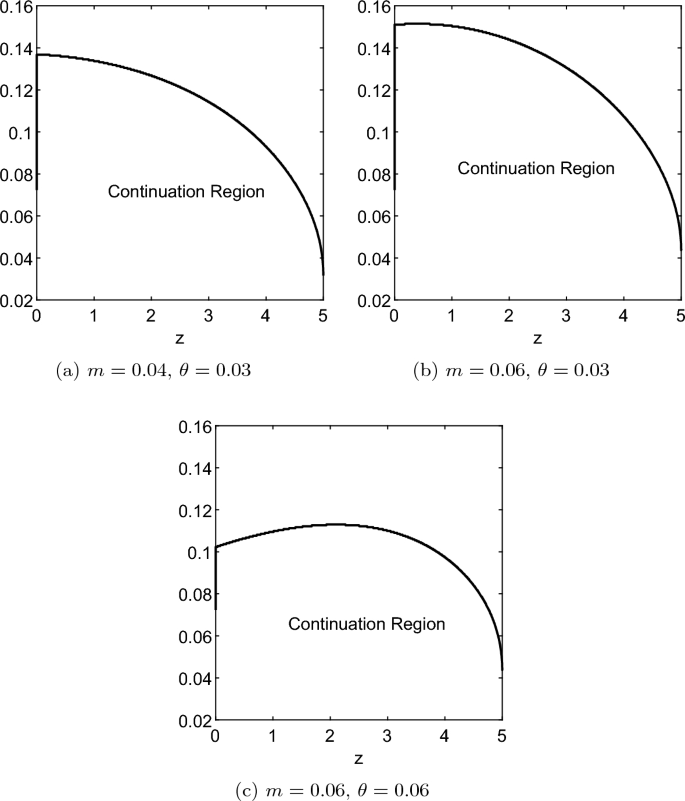

Leasing valuation is a topic that has aroused considerable interest in business circles. This paper examines leasing from the point of view of the lessor who can decide to leave the contract due to default. We analyze in introducing a model in which the lessor decides whether or not to terminate the contract at a given point in time, comparing it with the cost of capital of alternative investments. The proposed model is stochastic, and it is strongly based on correlated random walks, making it more adaptable to real-world circumstances. Furthermore, we propose a recombinant binomial tree based on correlated random walks, performing numerical simulations starting from CIR and Vasicek models. We will point out that as the rate of cost of capital of an alternative investment increases, the optimal boundary curve decreases, so the lessor leaves, while as the past interest rates increases, the curve rises and the lessor will have a concrete interest in maintaining the contract.

期刊介绍:

Decisions in Economics and Finance: A Journal of Applied Mathematics is the official publication of the Association for Mathematics Applied to Social and Economic Sciences (AMASES). It provides a specialised forum for the publication of research in all areas of mathematics as applied to economics, finance, insurance, management and social sciences. Primary emphasis is placed on original research concerning topics in mathematics or computational techniques which are explicitly motivated by or contribute to the analysis of economic or financial problems.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们