{"title":"休伯损失与空间自回归模型:利用先验信息的稳健变量选择方法","authors":"Yunquan Song, Minmin Zhan, Yue Zhang, Yongxin Liu","doi":"10.1007/s11067-024-09614-6","DOIUrl":null,"url":null,"abstract":"<p>In recent times, the significance of variable selection has amplified because of the advent of high-dimensional data. The regularization method is a popular technique for variable selection and parameter estimation. However, spatial data is more intricate than ordinary data because of spatial correlation and non-stationarity. This article proposes a robust regularization regression estimator based on Huber loss and a generalized Lasso penalty to surmount these obstacles. Moreover, linear equality and inequality constraints are contemplated to boost the efficiency and accuracy of model estimation. To evaluate the suggested model’s performance, we formulate its Karush-Kuhn-Tucker (KKT) conditions, which are indicators used to assess the model’s characteristics and constraints, and establish a set of indicators, comprising the formula for the degrees of freedom. We employ these indicators to construct the AIC and BIC information criteria, which assist in choosing the optimal tuning parameters in numerical simulations. Using the classic Boston Housing dataset, we compare the suggested model’s performance with that of the model under squared loss in scenarios with and without anomalies. The outcomes demonstrate that the suggested model accomplishes robust variable selection. This investigation provides a novel approach for spatial data analysis with extensive applications in various fields, including economics, ecology, and medicine, and can facilitate the enhancement of the efficiency and accuracy of model estimation.</p>","PeriodicalId":501141,"journal":{"name":"Networks and Spatial Economics","volume":"12 1","pages":""},"PeriodicalIF":0.0000,"publicationDate":"2024-01-27","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"","citationCount":"0","resultStr":"{\"title\":\"Huber Loss Meets Spatial Autoregressive Model: A Robust Variable Selection Method with Prior Information\",\"authors\":\"Yunquan Song, Minmin Zhan, Yue Zhang, Yongxin Liu\",\"doi\":\"10.1007/s11067-024-09614-6\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>In recent times, the significance of variable selection has amplified because of the advent of high-dimensional data. The regularization method is a popular technique for variable selection and parameter estimation. However, spatial data is more intricate than ordinary data because of spatial correlation and non-stationarity. This article proposes a robust regularization regression estimator based on Huber loss and a generalized Lasso penalty to surmount these obstacles. Moreover, linear equality and inequality constraints are contemplated to boost the efficiency and accuracy of model estimation. To evaluate the suggested model’s performance, we formulate its Karush-Kuhn-Tucker (KKT) conditions, which are indicators used to assess the model’s characteristics and constraints, and establish a set of indicators, comprising the formula for the degrees of freedom. We employ these indicators to construct the AIC and BIC information criteria, which assist in choosing the optimal tuning parameters in numerical simulations. Using the classic Boston Housing dataset, we compare the suggested model’s performance with that of the model under squared loss in scenarios with and without anomalies. The outcomes demonstrate that the suggested model accomplishes robust variable selection. This investigation provides a novel approach for spatial data analysis with extensive applications in various fields, including economics, ecology, and medicine, and can facilitate the enhancement of the efficiency and accuracy of model estimation.</p>\",\"PeriodicalId\":501141,\"journal\":{\"name\":\"Networks and Spatial Economics\",\"volume\":\"12 1\",\"pages\":\"\"},\"PeriodicalIF\":0.0000,\"publicationDate\":\"2024-01-27\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Networks and Spatial Economics\",\"FirstCategoryId\":\"1085\",\"ListUrlMain\":\"https://doi.org/10.1007/s11067-024-09614-6\",\"RegionNum\":0,\"RegionCategory\":null,\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"\",\"JCRName\":\"\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Networks and Spatial Economics","FirstCategoryId":"1085","ListUrlMain":"https://doi.org/10.1007/s11067-024-09614-6","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"","JCRName":"","Score":null,"Total":0}

Huber Loss Meets Spatial Autoregressive Model: A Robust Variable Selection Method with Prior Information

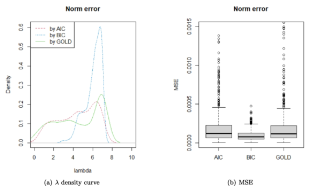

In recent times, the significance of variable selection has amplified because of the advent of high-dimensional data. The regularization method is a popular technique for variable selection and parameter estimation. However, spatial data is more intricate than ordinary data because of spatial correlation and non-stationarity. This article proposes a robust regularization regression estimator based on Huber loss and a generalized Lasso penalty to surmount these obstacles. Moreover, linear equality and inequality constraints are contemplated to boost the efficiency and accuracy of model estimation. To evaluate the suggested model’s performance, we formulate its Karush-Kuhn-Tucker (KKT) conditions, which are indicators used to assess the model’s characteristics and constraints, and establish a set of indicators, comprising the formula for the degrees of freedom. We employ these indicators to construct the AIC and BIC information criteria, which assist in choosing the optimal tuning parameters in numerical simulations. Using the classic Boston Housing dataset, we compare the suggested model’s performance with that of the model under squared loss in scenarios with and without anomalies. The outcomes demonstrate that the suggested model accomplishes robust variable selection. This investigation provides a novel approach for spatial data analysis with extensive applications in various fields, including economics, ecology, and medicine, and can facilitate the enhancement of the efficiency and accuracy of model estimation.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们