Mellouli Dhoha, Wael Dammak, Hind Alnafisah, Ahmed Jeribi

{"title":"健康和政治危机期间天然气与金砖国家股市之间的动态溢出效应","authors":"Mellouli Dhoha, Wael Dammak, Hind Alnafisah, Ahmed Jeribi","doi":"10.1007/s40822-023-00254-8","DOIUrl":null,"url":null,"abstract":"<p>Previous research has primarily focused on external factors to refine predictions of natural gas volatility, a prominent cleaner fossil fuel. Yet, there's a gap in the literature regarding the intrinsic factors impacting the volatility of natural gas returns, especially during crises. Using the TVP-VAR frequency connectedness method, we uncover a pronounced dynamic integration and return transmission between natural gas and BRICS stock markets. Our findings emphasize a strong interconnectedness in both the lower and upper extremes of the return distribution, indicating the profound effects of both negative and positive extreme shocks. We also document symmetric spillover effects in tumultuous market conditions. Short-term spillovers are critical in transmitting shocks, while long-term ones define interconnectedness patterns. Notably, we identify assets that are net-receivers and net-transmitters, with natural gas consistently being a net receiver. Our results provide valuable insights for investors and portfolio managers, emphasizing the need for stringent risk management during crises like COVID-19 and the Russia–Ukraine conflict due to the presence of non-diversifiable systematic risks.</p>","PeriodicalId":45064,"journal":{"name":"Eurasian Economic Review","volume":"308 1","pages":""},"PeriodicalIF":2.5000,"publicationDate":"2024-02-16","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"","citationCount":"0","resultStr":"{\"title\":\"Dynamic spillovers between natural gas and BRICS stock markets during health and political crises\",\"authors\":\"Mellouli Dhoha, Wael Dammak, Hind Alnafisah, Ahmed Jeribi\",\"doi\":\"10.1007/s40822-023-00254-8\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>Previous research has primarily focused on external factors to refine predictions of natural gas volatility, a prominent cleaner fossil fuel. Yet, there's a gap in the literature regarding the intrinsic factors impacting the volatility of natural gas returns, especially during crises. Using the TVP-VAR frequency connectedness method, we uncover a pronounced dynamic integration and return transmission between natural gas and BRICS stock markets. Our findings emphasize a strong interconnectedness in both the lower and upper extremes of the return distribution, indicating the profound effects of both negative and positive extreme shocks. We also document symmetric spillover effects in tumultuous market conditions. Short-term spillovers are critical in transmitting shocks, while long-term ones define interconnectedness patterns. Notably, we identify assets that are net-receivers and net-transmitters, with natural gas consistently being a net receiver. Our results provide valuable insights for investors and portfolio managers, emphasizing the need for stringent risk management during crises like COVID-19 and the Russia–Ukraine conflict due to the presence of non-diversifiable systematic risks.</p>\",\"PeriodicalId\":45064,\"journal\":{\"name\":\"Eurasian Economic Review\",\"volume\":\"308 1\",\"pages\":\"\"},\"PeriodicalIF\":2.5000,\"publicationDate\":\"2024-02-16\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Eurasian Economic Review\",\"FirstCategoryId\":\"1085\",\"ListUrlMain\":\"https://doi.org/10.1007/s40822-023-00254-8\",\"RegionNum\":0,\"RegionCategory\":null,\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q2\",\"JCRName\":\"ECONOMICS\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Eurasian Economic Review","FirstCategoryId":"1085","ListUrlMain":"https://doi.org/10.1007/s40822-023-00254-8","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q2","JCRName":"ECONOMICS","Score":null,"Total":0}

Dynamic spillovers between natural gas and BRICS stock markets during health and political crises

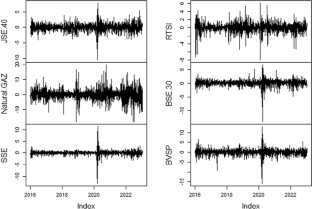

Previous research has primarily focused on external factors to refine predictions of natural gas volatility, a prominent cleaner fossil fuel. Yet, there's a gap in the literature regarding the intrinsic factors impacting the volatility of natural gas returns, especially during crises. Using the TVP-VAR frequency connectedness method, we uncover a pronounced dynamic integration and return transmission between natural gas and BRICS stock markets. Our findings emphasize a strong interconnectedness in both the lower and upper extremes of the return distribution, indicating the profound effects of both negative and positive extreme shocks. We also document symmetric spillover effects in tumultuous market conditions. Short-term spillovers are critical in transmitting shocks, while long-term ones define interconnectedness patterns. Notably, we identify assets that are net-receivers and net-transmitters, with natural gas consistently being a net receiver. Our results provide valuable insights for investors and portfolio managers, emphasizing the need for stringent risk management during crises like COVID-19 and the Russia–Ukraine conflict due to the presence of non-diversifiable systematic risks.

期刊介绍:

The mission of Eurasian Economic Review is to publish peer-reviewed empirical research papers that test, extend, or build theory and contribute to practice. All empirical methods - including, but not limited to, qualitative, quantitative, field, laboratory, and any combination of methods - are welcome. Empirical, theoretical and methodological articles from all fields of finance and applied macroeconomics are featured in the journal. Theoretical and/or review articles that integrate existing bodies of research and that provide new insights into the field are highly encouraged. The journal has a broad scope, addressing such issues as: financial systems and regulation, corporate and start-up finance, macro and sustainable finance, finance and innovation, consumer finance, public policies on financial markets within local, regional, national and international contexts, money and banking, and the interface of labor and financial economics. The macroeconomics coverage includes topics from monetary economics, labor economics, international economics and development economics.

Eurasian Economic Review is published quarterly. To be published in Eurasian Economic Review, a manuscript must make strong empirical and/or theoretical contributions and highlight the significance of those contributions to our field. Consequently, preference is given to submissions that test, extend, or build strong theoretical frameworks while empirically examining issues with high importance for theory and practice. Eurasian Economic Review is not tied to any national context. Although it focuses on Europe and Asia, all papers from related fields on any region or country are highly encouraged. Single country studies, cross-country or regional studies can be submitted.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们