{"title":"分布稳健的可能性优化框架","authors":"Romain Guillaume, Adam Kasperski, Paweł Zieliński","doi":"10.1007/s10700-024-09420-2","DOIUrl":null,"url":null,"abstract":"<p>In this paper, an optimization problem with uncertain constraint coefficients is considered. Possibility theory is used to model the uncertainty. Namely, a joint possibility distribution in constraint coefficient realizations, called scenarios, is specified. This possibility distribution induces a necessity measure in a scenario set, which in turn describes an ambiguity set of probability distributions in a scenario set. The distributionally robust approach is then used to convert the imprecise constraints into deterministic equivalents. Namely, the left-hand side of an imprecise constraint is evaluated by using a risk measure with respect to the worst probability distribution that can occur. In this paper, the Conditional Value at Risk is used as the risk measure, which generalizes the strict robust, and expected value approaches commonly used in literature. A general framework for solving such a class of problems is described. Some cases which can be solved in polynomial time are identified.</p>","PeriodicalId":55131,"journal":{"name":"Fuzzy Optimization and Decision Making","volume":"65 1","pages":""},"PeriodicalIF":4.8000,"publicationDate":"2024-02-07","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"","citationCount":"0","resultStr":"{\"title\":\"A framework of distributionally robust possibilistic optimization\",\"authors\":\"Romain Guillaume, Adam Kasperski, Paweł Zieliński\",\"doi\":\"10.1007/s10700-024-09420-2\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>In this paper, an optimization problem with uncertain constraint coefficients is considered. Possibility theory is used to model the uncertainty. Namely, a joint possibility distribution in constraint coefficient realizations, called scenarios, is specified. This possibility distribution induces a necessity measure in a scenario set, which in turn describes an ambiguity set of probability distributions in a scenario set. The distributionally robust approach is then used to convert the imprecise constraints into deterministic equivalents. Namely, the left-hand side of an imprecise constraint is evaluated by using a risk measure with respect to the worst probability distribution that can occur. In this paper, the Conditional Value at Risk is used as the risk measure, which generalizes the strict robust, and expected value approaches commonly used in literature. A general framework for solving such a class of problems is described. Some cases which can be solved in polynomial time are identified.</p>\",\"PeriodicalId\":55131,\"journal\":{\"name\":\"Fuzzy Optimization and Decision Making\",\"volume\":\"65 1\",\"pages\":\"\"},\"PeriodicalIF\":4.8000,\"publicationDate\":\"2024-02-07\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Fuzzy Optimization and Decision Making\",\"FirstCategoryId\":\"94\",\"ListUrlMain\":\"https://doi.org/10.1007/s10700-024-09420-2\",\"RegionNum\":2,\"RegionCategory\":\"计算机科学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q1\",\"JCRName\":\"COMPUTER SCIENCE, ARTIFICIAL INTELLIGENCE\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Fuzzy Optimization and Decision Making","FirstCategoryId":"94","ListUrlMain":"https://doi.org/10.1007/s10700-024-09420-2","RegionNum":2,"RegionCategory":"计算机科学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q1","JCRName":"COMPUTER SCIENCE, ARTIFICIAL INTELLIGENCE","Score":null,"Total":0}

A framework of distributionally robust possibilistic optimization

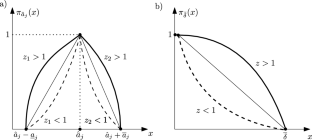

In this paper, an optimization problem with uncertain constraint coefficients is considered. Possibility theory is used to model the uncertainty. Namely, a joint possibility distribution in constraint coefficient realizations, called scenarios, is specified. This possibility distribution induces a necessity measure in a scenario set, which in turn describes an ambiguity set of probability distributions in a scenario set. The distributionally robust approach is then used to convert the imprecise constraints into deterministic equivalents. Namely, the left-hand side of an imprecise constraint is evaluated by using a risk measure with respect to the worst probability distribution that can occur. In this paper, the Conditional Value at Risk is used as the risk measure, which generalizes the strict robust, and expected value approaches commonly used in literature. A general framework for solving such a class of problems is described. Some cases which can be solved in polynomial time are identified.

期刊介绍:

The key objective of Fuzzy Optimization and Decision Making is to promote research and the development of fuzzy technology and soft-computing methodologies to enhance our ability to address complicated optimization and decision making problems involving non-probabilitic uncertainty.

The journal will cover all aspects of employing fuzzy technologies to see optimal solutions and assist in making the best possible decisions. It will provide a global forum for advancing the state-of-the-art theory and practice of fuzzy optimization and decision making in the presence of uncertainty. Any theoretical, empirical, and experimental work related to fuzzy modeling and associated mathematics, solution methods, and systems is welcome. The goal is to help foster the understanding, development, and practice of fuzzy technologies for solving economic, engineering, management, and societal problems. The journal will provide a forum for authors and readers in the fields of business, economics, engineering, mathematics, management science, operations research, and systems.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们