{"title":"偏斜寻求行为与金融投资","authors":"Matteo Benuzzi, Matteo Ploner","doi":"10.1007/s10436-023-00437-y","DOIUrl":null,"url":null,"abstract":"<div><p>Recent theoretical and empirical advancements highlight the pivotal role played by higher-order moments, such as skewness, in shaping financial decision-making. Nevertheless, contemporary experimental research predominantly relies on limited-outcome lotteries, an oversimplified representation distant from real-world investment dynamics. To bridge this research gap, we conducted a rigorously pre-registered experiment. Our study delves into individuals’ preferences for investment opportunities, examining the influence of skewness of continuous probability distributions of returns. We document an inclination towards positively skewed outcome distributions. Furthermore, we uncovered a substitution effect between risk appetite and the sign of skewness. Finally, we unveiled a robust positive correlation between skewness-seeking behavior and a propensity for speculative behavior. Simultaneously, a distinct negative correlation surfaced between skewness-seeking behavior and the perceived risk associated with positive skewness.</p></div>","PeriodicalId":45289,"journal":{"name":"Annals of Finance","volume":"20 1","pages":"129 - 165"},"PeriodicalIF":0.7000,"publicationDate":"2024-02-26","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://link.springer.com/content/pdf/10.1007/s10436-023-00437-y.pdf","citationCount":"0","resultStr":"{\"title\":\"Skewness-seeking behavior and financial investments\",\"authors\":\"Matteo Benuzzi, Matteo Ploner\",\"doi\":\"10.1007/s10436-023-00437-y\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<div><p>Recent theoretical and empirical advancements highlight the pivotal role played by higher-order moments, such as skewness, in shaping financial decision-making. Nevertheless, contemporary experimental research predominantly relies on limited-outcome lotteries, an oversimplified representation distant from real-world investment dynamics. To bridge this research gap, we conducted a rigorously pre-registered experiment. Our study delves into individuals’ preferences for investment opportunities, examining the influence of skewness of continuous probability distributions of returns. We document an inclination towards positively skewed outcome distributions. Furthermore, we uncovered a substitution effect between risk appetite and the sign of skewness. Finally, we unveiled a robust positive correlation between skewness-seeking behavior and a propensity for speculative behavior. Simultaneously, a distinct negative correlation surfaced between skewness-seeking behavior and the perceived risk associated with positive skewness.</p></div>\",\"PeriodicalId\":45289,\"journal\":{\"name\":\"Annals of Finance\",\"volume\":\"20 1\",\"pages\":\"129 - 165\"},\"PeriodicalIF\":0.7000,\"publicationDate\":\"2024-02-26\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://link.springer.com/content/pdf/10.1007/s10436-023-00437-y.pdf\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Annals of Finance\",\"FirstCategoryId\":\"1085\",\"ListUrlMain\":\"https://link.springer.com/article/10.1007/s10436-023-00437-y\",\"RegionNum\":0,\"RegionCategory\":null,\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q4\",\"JCRName\":\"BUSINESS, FINANCE\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Annals of Finance","FirstCategoryId":"1085","ListUrlMain":"https://link.springer.com/article/10.1007/s10436-023-00437-y","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q4","JCRName":"BUSINESS, FINANCE","Score":null,"Total":0}

Skewness-seeking behavior and financial investments

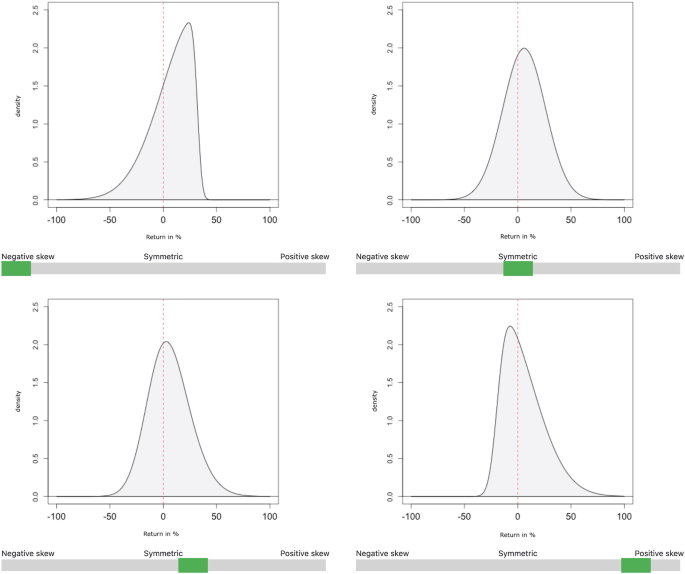

Recent theoretical and empirical advancements highlight the pivotal role played by higher-order moments, such as skewness, in shaping financial decision-making. Nevertheless, contemporary experimental research predominantly relies on limited-outcome lotteries, an oversimplified representation distant from real-world investment dynamics. To bridge this research gap, we conducted a rigorously pre-registered experiment. Our study delves into individuals’ preferences for investment opportunities, examining the influence of skewness of continuous probability distributions of returns. We document an inclination towards positively skewed outcome distributions. Furthermore, we uncovered a substitution effect between risk appetite and the sign of skewness. Finally, we unveiled a robust positive correlation between skewness-seeking behavior and a propensity for speculative behavior. Simultaneously, a distinct negative correlation surfaced between skewness-seeking behavior and the perceived risk associated with positive skewness.

期刊介绍:

Annals of Finance provides an outlet for original research in all areas of finance and its applications to other disciplines having a clear and substantive link to the general theme of finance. In particular, innovative research papers of moderate length of the highest quality in all scientific areas that are motivated by the analysis of financial problems will be considered. Annals of Finance''s scope encompasses - but is not limited to - the following areas: accounting and finance, asset pricing, banking and finance, capital markets and finance, computational finance, corporate finance, derivatives, dynamical and chaotic systems in finance, economics and finance, empirical finance, experimental finance, finance and the theory of the firm, financial econometrics, financial institutions, mathematical finance, money and finance, portfolio analysis, regulation, stochastic analysis and finance, stock market analysis, systemic risk and financial stability. Annals of Finance also publishes special issues on any topic in finance and its applications of current interest. A small section, entitled finance notes, will be devoted solely to publishing short articles – up to ten pages in length, of substantial interest in finance. Officially cited as: Ann Finance

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们