{"title":"工作超负荷、工作与生活的平衡以及审计人员的离职意向:动机的调节作用","authors":"Iryna Alves, Miguel Limão, Sofia M. Lourenço","doi":"10.1111/auar.12417","DOIUrl":null,"url":null,"abstract":"<p>Auditor turnover remains a persistent concern for regulatory bodies and auditing firms. Past research on auditors’ turnover intention has explored various factors influencing auditors’ turnover intention, including job satisfaction, organisational commitment, work overload and work–life balance. However, the potential role of motivation in mitigating the adverse effects of work overload and work–life imbalance has been overlooked. Our study addresses this gap in the existing literature by revealing the crucial role of motivation and identifying differences between Big4 and Non-Big4 firms. Using questionnaire data from 301 auditors, analysed using structural equation modelling, we find that work overload is positively but indirectly related to turnover intention via work–life balance. Additionally, organisational commitment (job satisfaction) is directly (indirectly) and negatively related to turnover intention. Moreover, and considering that, due to work overload, a lack of work–life balance can be responsible for increasing auditors’ turnover intention, our study suggests that motivation can mitigate this effect. Finally, our study suggests that work–life balance can directly reduce turnover intention for Big4 firms, while for Non-Big4 firms this reduction can only occur via organisational commitment (a channel that is weaker for Big4 firms).</p>","PeriodicalId":51552,"journal":{"name":"Australian Accounting Review","volume":"34 1","pages":"4-28"},"PeriodicalIF":2.8000,"publicationDate":"2024-02-29","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1111/auar.12417","citationCount":"0","resultStr":"{\"title\":\"Work Overload, Work–Life Balance and Auditors' Turnover Intention: The Moderating Role of Motivation\",\"authors\":\"Iryna Alves, Miguel Limão, Sofia M. Lourenço\",\"doi\":\"10.1111/auar.12417\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>Auditor turnover remains a persistent concern for regulatory bodies and auditing firms. Past research on auditors’ turnover intention has explored various factors influencing auditors’ turnover intention, including job satisfaction, organisational commitment, work overload and work–life balance. However, the potential role of motivation in mitigating the adverse effects of work overload and work–life imbalance has been overlooked. Our study addresses this gap in the existing literature by revealing the crucial role of motivation and identifying differences between Big4 and Non-Big4 firms. Using questionnaire data from 301 auditors, analysed using structural equation modelling, we find that work overload is positively but indirectly related to turnover intention via work–life balance. Additionally, organisational commitment (job satisfaction) is directly (indirectly) and negatively related to turnover intention. Moreover, and considering that, due to work overload, a lack of work–life balance can be responsible for increasing auditors’ turnover intention, our study suggests that motivation can mitigate this effect. Finally, our study suggests that work–life balance can directly reduce turnover intention for Big4 firms, while for Non-Big4 firms this reduction can only occur via organisational commitment (a channel that is weaker for Big4 firms).</p>\",\"PeriodicalId\":51552,\"journal\":{\"name\":\"Australian Accounting Review\",\"volume\":\"34 1\",\"pages\":\"4-28\"},\"PeriodicalIF\":2.8000,\"publicationDate\":\"2024-02-29\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://onlinelibrary.wiley.com/doi/epdf/10.1111/auar.12417\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Australian Accounting Review\",\"FirstCategoryId\":\"91\",\"ListUrlMain\":\"https://onlinelibrary.wiley.com/doi/10.1111/auar.12417\",\"RegionNum\":3,\"RegionCategory\":\"管理学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q2\",\"JCRName\":\"BUSINESS, FINANCE\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Australian Accounting Review","FirstCategoryId":"91","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1111/auar.12417","RegionNum":3,"RegionCategory":"管理学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q2","JCRName":"BUSINESS, FINANCE","Score":null,"Total":0}

Work Overload, Work–Life Balance and Auditors' Turnover Intention: The Moderating Role of Motivation

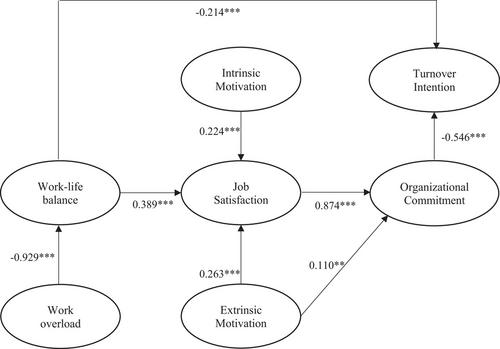

Auditor turnover remains a persistent concern for regulatory bodies and auditing firms. Past research on auditors’ turnover intention has explored various factors influencing auditors’ turnover intention, including job satisfaction, organisational commitment, work overload and work–life balance. However, the potential role of motivation in mitigating the adverse effects of work overload and work–life imbalance has been overlooked. Our study addresses this gap in the existing literature by revealing the crucial role of motivation and identifying differences between Big4 and Non-Big4 firms. Using questionnaire data from 301 auditors, analysed using structural equation modelling, we find that work overload is positively but indirectly related to turnover intention via work–life balance. Additionally, organisational commitment (job satisfaction) is directly (indirectly) and negatively related to turnover intention. Moreover, and considering that, due to work overload, a lack of work–life balance can be responsible for increasing auditors’ turnover intention, our study suggests that motivation can mitigate this effect. Finally, our study suggests that work–life balance can directly reduce turnover intention for Big4 firms, while for Non-Big4 firms this reduction can only occur via organisational commitment (a channel that is weaker for Big4 firms).

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们