{"title":"股市崩盘的预警信号:利用非线性方法的经验和分析见解","authors":"Shijia Song, Handong Li","doi":"10.1140/epjds/s13688-024-00457-2","DOIUrl":null,"url":null,"abstract":"<p>This study introduces a comprehensive framework grounded in recurrence analysis, a tool of nonlinear dynamics, to detect potential early warning signals (EWS) for imminent phase transitions in financial systems, with the primary goal of anticipating severe financial crashes. We first conduct a simulation experiment to demonstrate that the indicators based on multiplex recurrence networks (MRNs), namely the average mutual information and the average edge overlap, can indicate state transitions in complex systems. Subsequently, we consider the constituent stocks of the China’s and the U.S. stock markets as empirical subjects, and establish MRNs based on multidimensional returns to monitor the nonlinear dynamics of market through the corresponding the indicators and topological structures. Empirical findings indicate that the primary indicators of MRNs offer valuable insights into significant financial events or periods of extreme instability. Notably, average mutual information demonstrates promise as an effective EWS for forecasting forthcoming financial crashes. An in-depth discussion and elucidation of the theoretical underpinnings for employing indicators of MRNs as EWS, the differences in indicator effectiveness, and the possible reasons for variations in the performance of the EWS across the two markets are provided. This paper contributes to the ongoing discourse on early warning extreme market volatility, emphasizing the applicability of recurrence analysis in predicting financial crashes.</p>","PeriodicalId":11887,"journal":{"name":"EPJ Data Science","volume":"11 1","pages":""},"PeriodicalIF":2.5000,"publicationDate":"2024-03-05","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"","citationCount":"0","resultStr":"{\"title\":\"Early warning signals for stock market crashes: empirical and analytical insights utilizing nonlinear methods\",\"authors\":\"Shijia Song, Handong Li\",\"doi\":\"10.1140/epjds/s13688-024-00457-2\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>This study introduces a comprehensive framework grounded in recurrence analysis, a tool of nonlinear dynamics, to detect potential early warning signals (EWS) for imminent phase transitions in financial systems, with the primary goal of anticipating severe financial crashes. We first conduct a simulation experiment to demonstrate that the indicators based on multiplex recurrence networks (MRNs), namely the average mutual information and the average edge overlap, can indicate state transitions in complex systems. Subsequently, we consider the constituent stocks of the China’s and the U.S. stock markets as empirical subjects, and establish MRNs based on multidimensional returns to monitor the nonlinear dynamics of market through the corresponding the indicators and topological structures. Empirical findings indicate that the primary indicators of MRNs offer valuable insights into significant financial events or periods of extreme instability. Notably, average mutual information demonstrates promise as an effective EWS for forecasting forthcoming financial crashes. An in-depth discussion and elucidation of the theoretical underpinnings for employing indicators of MRNs as EWS, the differences in indicator effectiveness, and the possible reasons for variations in the performance of the EWS across the two markets are provided. This paper contributes to the ongoing discourse on early warning extreme market volatility, emphasizing the applicability of recurrence analysis in predicting financial crashes.</p>\",\"PeriodicalId\":11887,\"journal\":{\"name\":\"EPJ Data Science\",\"volume\":\"11 1\",\"pages\":\"\"},\"PeriodicalIF\":2.5000,\"publicationDate\":\"2024-03-05\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"EPJ Data Science\",\"FirstCategoryId\":\"94\",\"ListUrlMain\":\"https://doi.org/10.1140/epjds/s13688-024-00457-2\",\"RegionNum\":2,\"RegionCategory\":\"计算机科学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q1\",\"JCRName\":\"MATHEMATICS, INTERDISCIPLINARY APPLICATIONS\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"EPJ Data Science","FirstCategoryId":"94","ListUrlMain":"https://doi.org/10.1140/epjds/s13688-024-00457-2","RegionNum":2,"RegionCategory":"计算机科学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q1","JCRName":"MATHEMATICS, INTERDISCIPLINARY APPLICATIONS","Score":null,"Total":0}

Early warning signals for stock market crashes: empirical and analytical insights utilizing nonlinear methods

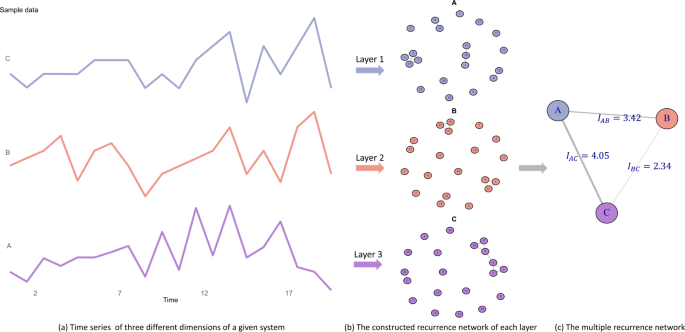

This study introduces a comprehensive framework grounded in recurrence analysis, a tool of nonlinear dynamics, to detect potential early warning signals (EWS) for imminent phase transitions in financial systems, with the primary goal of anticipating severe financial crashes. We first conduct a simulation experiment to demonstrate that the indicators based on multiplex recurrence networks (MRNs), namely the average mutual information and the average edge overlap, can indicate state transitions in complex systems. Subsequently, we consider the constituent stocks of the China’s and the U.S. stock markets as empirical subjects, and establish MRNs based on multidimensional returns to monitor the nonlinear dynamics of market through the corresponding the indicators and topological structures. Empirical findings indicate that the primary indicators of MRNs offer valuable insights into significant financial events or periods of extreme instability. Notably, average mutual information demonstrates promise as an effective EWS for forecasting forthcoming financial crashes. An in-depth discussion and elucidation of the theoretical underpinnings for employing indicators of MRNs as EWS, the differences in indicator effectiveness, and the possible reasons for variations in the performance of the EWS across the two markets are provided. This paper contributes to the ongoing discourse on early warning extreme market volatility, emphasizing the applicability of recurrence analysis in predicting financial crashes.

期刊介绍:

EPJ Data Science covers a broad range of research areas and applications and particularly encourages contributions from techno-socio-economic systems, where it comprises those research lines that now regard the digital “tracks” of human beings as first-order objects for scientific investigation. Topics include, but are not limited to, human behavior, social interaction (including animal societies), economic and financial systems, management and business networks, socio-technical infrastructure, health and environmental systems, the science of science, as well as general risk and crisis scenario forecasting up to and including policy advice.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们