PIERRE COLLIN-DUFRESNE, BENJAMIN JUNGE, ANDERS B. TROLLE

{"title":"信贷市场和股票市场的融合程度如何?指数期权的证据","authors":"PIERRE COLLIN-DUFRESNE, BENJAMIN JUNGE, ANDERS B. TROLLE","doi":"10.1111/jofi.13300","DOIUrl":null,"url":null,"abstract":"<p>We study the extent to which credit index (CDX) options are priced consistent with S&P 500 (SPX) equity index options. We derive analytical expressions for CDX and SPX options within a structural credit-risk model with stochastic volatility and jumps using new results for pricing compound options via multivariate affine transform analysis. The model captures many aspects of the joint dynamics of CDX and SPX options. However, it cannot reconcile the relative levels of option prices, suggesting that credit and equity markets are not fully integrated. A strategy of selling CDX volatility yields significantly higher excess returns than selling SPX volatility.</p>","PeriodicalId":15753,"journal":{"name":"Journal of Finance","volume":"79 2","pages":"949-992"},"PeriodicalIF":9.5000,"publicationDate":"2023-12-12","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1111/jofi.13300","citationCount":"0","resultStr":"{\"title\":\"How Integrated are Credit and Equity Markets? Evidence from Index Options\",\"authors\":\"PIERRE COLLIN-DUFRESNE, BENJAMIN JUNGE, ANDERS B. TROLLE\",\"doi\":\"10.1111/jofi.13300\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>We study the extent to which credit index (CDX) options are priced consistent with S&P 500 (SPX) equity index options. We derive analytical expressions for CDX and SPX options within a structural credit-risk model with stochastic volatility and jumps using new results for pricing compound options via multivariate affine transform analysis. The model captures many aspects of the joint dynamics of CDX and SPX options. However, it cannot reconcile the relative levels of option prices, suggesting that credit and equity markets are not fully integrated. A strategy of selling CDX volatility yields significantly higher excess returns than selling SPX volatility.</p>\",\"PeriodicalId\":15753,\"journal\":{\"name\":\"Journal of Finance\",\"volume\":\"79 2\",\"pages\":\"949-992\"},\"PeriodicalIF\":9.5000,\"publicationDate\":\"2023-12-12\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://onlinelibrary.wiley.com/doi/epdf/10.1111/jofi.13300\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Journal of Finance\",\"FirstCategoryId\":\"96\",\"ListUrlMain\":\"https://onlinelibrary.wiley.com/doi/10.1111/jofi.13300\",\"RegionNum\":1,\"RegionCategory\":\"经济学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q1\",\"JCRName\":\"BUSINESS, FINANCE\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Journal of Finance","FirstCategoryId":"96","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1111/jofi.13300","RegionNum":1,"RegionCategory":"经济学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q1","JCRName":"BUSINESS, FINANCE","Score":null,"Total":0}

How Integrated are Credit and Equity Markets? Evidence from Index Options

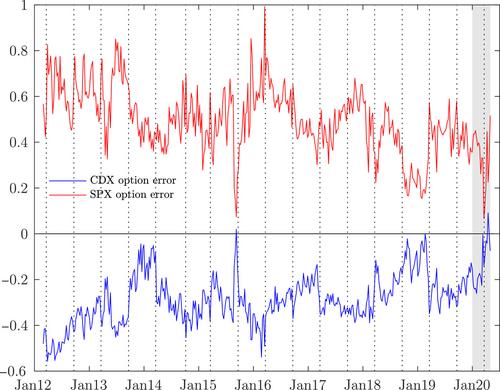

We study the extent to which credit index (CDX) options are priced consistent with S&P 500 (SPX) equity index options. We derive analytical expressions for CDX and SPX options within a structural credit-risk model with stochastic volatility and jumps using new results for pricing compound options via multivariate affine transform analysis. The model captures many aspects of the joint dynamics of CDX and SPX options. However, it cannot reconcile the relative levels of option prices, suggesting that credit and equity markets are not fully integrated. A strategy of selling CDX volatility yields significantly higher excess returns than selling SPX volatility.

期刊介绍:

The Journal of Finance is a renowned publication that disseminates cutting-edge research across all major fields of financial inquiry. Widely regarded as the most cited academic journal in finance, each issue reaches over 8,000 academics, finance professionals, libraries, government entities, and financial institutions worldwide. Published bi-monthly, the journal serves as the official publication of The American Finance Association, the premier academic organization dedicated to advancing knowledge and understanding in financial economics. Join us in exploring the forefront of financial research and scholarship.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们