{"title":"定量比率回归","authors":"Alessio Farcomeni, Marco Geraci","doi":"10.1007/s11222-024-10406-8","DOIUrl":null,"url":null,"abstract":"<p>We introduce quantile ratio regression. Our proposed model assumes that the ratio of two arbitrary quantiles of a continuous response distribution is a function of a linear predictor. Thanks to basic quantile properties, estimation can be carried out on the scale of either the response or the link function. The advantage of using the latter becomes tangible when implementing fast optimizers for linear regression in the presence of large datasets. We show the theoretical properties of the estimator and derive an efficient method to obtain standard errors. The good performance and merit of our methods are illustrated by means of a simulation study and a real data analysis; where we investigate income inequality in the European Union (EU) using data from a sample of about two million households. We find a significant association between inequality, as measured by quantile ratios, and certain macroeconomic indicators; and we identify countries with outlying income inequality relative to the rest of the EU. An <span>R</span> implementation of the proposed methods is freely available.</p>","PeriodicalId":22058,"journal":{"name":"Statistics and Computing","volume":"23 1","pages":""},"PeriodicalIF":1.8000,"publicationDate":"2024-03-14","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"","citationCount":"0","resultStr":"{\"title\":\"Quantile ratio regression\",\"authors\":\"Alessio Farcomeni, Marco Geraci\",\"doi\":\"10.1007/s11222-024-10406-8\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>We introduce quantile ratio regression. Our proposed model assumes that the ratio of two arbitrary quantiles of a continuous response distribution is a function of a linear predictor. Thanks to basic quantile properties, estimation can be carried out on the scale of either the response or the link function. The advantage of using the latter becomes tangible when implementing fast optimizers for linear regression in the presence of large datasets. We show the theoretical properties of the estimator and derive an efficient method to obtain standard errors. The good performance and merit of our methods are illustrated by means of a simulation study and a real data analysis; where we investigate income inequality in the European Union (EU) using data from a sample of about two million households. We find a significant association between inequality, as measured by quantile ratios, and certain macroeconomic indicators; and we identify countries with outlying income inequality relative to the rest of the EU. An <span>R</span> implementation of the proposed methods is freely available.</p>\",\"PeriodicalId\":22058,\"journal\":{\"name\":\"Statistics and Computing\",\"volume\":\"23 1\",\"pages\":\"\"},\"PeriodicalIF\":1.8000,\"publicationDate\":\"2024-03-14\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Statistics and Computing\",\"FirstCategoryId\":\"100\",\"ListUrlMain\":\"https://doi.org/10.1007/s11222-024-10406-8\",\"RegionNum\":2,\"RegionCategory\":\"数学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q2\",\"JCRName\":\"COMPUTER SCIENCE, THEORY & METHODS\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Statistics and Computing","FirstCategoryId":"100","ListUrlMain":"https://doi.org/10.1007/s11222-024-10406-8","RegionNum":2,"RegionCategory":"数学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q2","JCRName":"COMPUTER SCIENCE, THEORY & METHODS","Score":null,"Total":0}

引用次数: 0

摘要

我们介绍量值比回归。我们提出的模型假定连续响应分布的两个任意量级的比值是线性预测因子的函数。利用量值的基本特性,可以在响应或链接函数的尺度上进行估计。当在大型数据集中实施线性回归的快速优化时,使用后者的优势就显而易见了。我们展示了估计器的理论特性,并推导出一种获取标准误差的有效方法。我们通过模拟研究和实际数据分析,对欧盟(EU)的收入不平等现象进行了调查。我们发现,以量子比率衡量的不平等与某些宏观经济指标之间存在重要关联;我们还确定了与欧盟其他国家相比收入不平等程度偏高的国家。我们免费提供所建议方法的 R 实现。

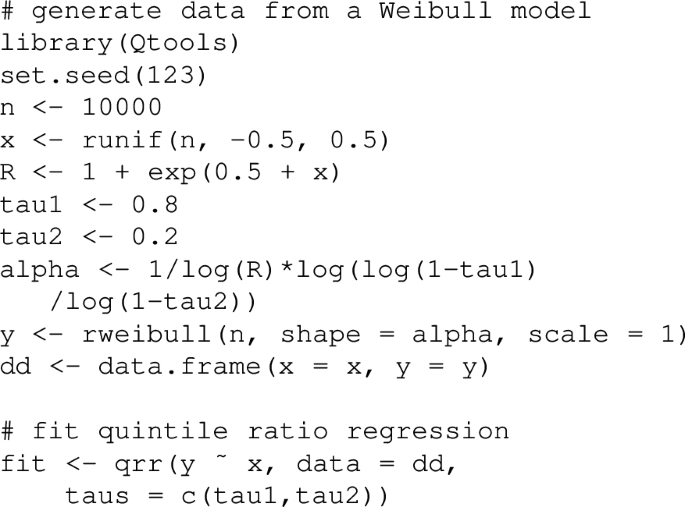

We introduce quantile ratio regression. Our proposed model assumes that the ratio of two arbitrary quantiles of a continuous response distribution is a function of a linear predictor. Thanks to basic quantile properties, estimation can be carried out on the scale of either the response or the link function. The advantage of using the latter becomes tangible when implementing fast optimizers for linear regression in the presence of large datasets. We show the theoretical properties of the estimator and derive an efficient method to obtain standard errors. The good performance and merit of our methods are illustrated by means of a simulation study and a real data analysis; where we investigate income inequality in the European Union (EU) using data from a sample of about two million households. We find a significant association between inequality, as measured by quantile ratios, and certain macroeconomic indicators; and we identify countries with outlying income inequality relative to the rest of the EU. An R implementation of the proposed methods is freely available.

期刊介绍:

Statistics and Computing is a bi-monthly refereed journal which publishes papers covering the range of the interface between the statistical and computing sciences.

In particular, it addresses the use of statistical concepts in computing science, for example in machine learning, computer vision and data analytics, as well as the use of computers in data modelling, prediction and analysis. Specific topics which are covered include: techniques for evaluating analytically intractable problems such as bootstrap resampling, Markov chain Monte Carlo, sequential Monte Carlo, approximate Bayesian computation, search and optimization methods, stochastic simulation and Monte Carlo, graphics, computer environments, statistical approaches to software errors, information retrieval, machine learning, statistics of databases and database technology, huge data sets and big data analytics, computer algebra, graphical models, image processing, tomography, inverse problems and uncertainty quantification.

In addition, the journal contains original research reports, authoritative review papers, discussed papers, and occasional special issues on particular topics or carrying proceedings of relevant conferences. Statistics and Computing also publishes book review and software review sections.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们