{"title":"治理对审计文化、质量和控制问题的中介效应","authors":"Khodor Shatila, Nirjhar Nigam, Cristiane Benetti","doi":"10.1057/s41310-024-00235-6","DOIUrl":null,"url":null,"abstract":"<p>This study investigates whether governance acts as a mediating factor between audit culture, audit quality, and internal control aspects by examining the factors contributing to effective governance. This study uses a quantitative research design; we collect primary data using a structured survey questionnaire. The study was conducted on responses received for 350 respondents and analysed using structural equation models. The results indicate that governance leadership mediates the relationship between audit culture, internal control, and audit quality to some extent. By emphasizing the importance of governance for audit culture and quality, regulators can develop effective policies to promote high-quality audits and financial reporting. Indeed, governance acts as a guiding force in an organization’s culture. Think of it as the compass that sets the direction and promotes transparency, accountability, and ethical behavior, thereby fostering a strong audit culture. Internal control, on the other hand, encompasses the policies, procedures, and practices that protect assets, ensure accurate financial reporting, and comply with regulations. Governance structures provide the framework within which internal control operates, overseeing its functions and establishing mechanisms for accountability and reporting. The results of this research have important practical implications for accounting and audit firms and regulators.</p>","PeriodicalId":45050,"journal":{"name":"International Journal of Disclosure and Governance","volume":"27 1","pages":""},"PeriodicalIF":2.4000,"publicationDate":"2024-03-17","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"","citationCount":"0","resultStr":"{\"title\":\"The mediating effect of governance on audit culture, quality and control issues\",\"authors\":\"Khodor Shatila, Nirjhar Nigam, Cristiane Benetti\",\"doi\":\"10.1057/s41310-024-00235-6\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>This study investigates whether governance acts as a mediating factor between audit culture, audit quality, and internal control aspects by examining the factors contributing to effective governance. This study uses a quantitative research design; we collect primary data using a structured survey questionnaire. The study was conducted on responses received for 350 respondents and analysed using structural equation models. The results indicate that governance leadership mediates the relationship between audit culture, internal control, and audit quality to some extent. By emphasizing the importance of governance for audit culture and quality, regulators can develop effective policies to promote high-quality audits and financial reporting. Indeed, governance acts as a guiding force in an organization’s culture. Think of it as the compass that sets the direction and promotes transparency, accountability, and ethical behavior, thereby fostering a strong audit culture. Internal control, on the other hand, encompasses the policies, procedures, and practices that protect assets, ensure accurate financial reporting, and comply with regulations. Governance structures provide the framework within which internal control operates, overseeing its functions and establishing mechanisms for accountability and reporting. The results of this research have important practical implications for accounting and audit firms and regulators.</p>\",\"PeriodicalId\":45050,\"journal\":{\"name\":\"International Journal of Disclosure and Governance\",\"volume\":\"27 1\",\"pages\":\"\"},\"PeriodicalIF\":2.4000,\"publicationDate\":\"2024-03-17\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"International Journal of Disclosure and Governance\",\"FirstCategoryId\":\"1085\",\"ListUrlMain\":\"https://doi.org/10.1057/s41310-024-00235-6\",\"RegionNum\":0,\"RegionCategory\":null,\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q2\",\"JCRName\":\"MANAGEMENT\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"International Journal of Disclosure and Governance","FirstCategoryId":"1085","ListUrlMain":"https://doi.org/10.1057/s41310-024-00235-6","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q2","JCRName":"MANAGEMENT","Score":null,"Total":0}

The mediating effect of governance on audit culture, quality and control issues

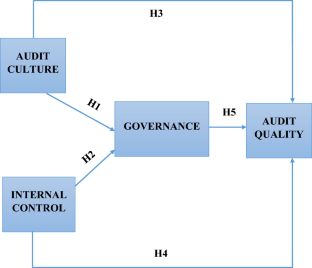

This study investigates whether governance acts as a mediating factor between audit culture, audit quality, and internal control aspects by examining the factors contributing to effective governance. This study uses a quantitative research design; we collect primary data using a structured survey questionnaire. The study was conducted on responses received for 350 respondents and analysed using structural equation models. The results indicate that governance leadership mediates the relationship between audit culture, internal control, and audit quality to some extent. By emphasizing the importance of governance for audit culture and quality, regulators can develop effective policies to promote high-quality audits and financial reporting. Indeed, governance acts as a guiding force in an organization’s culture. Think of it as the compass that sets the direction and promotes transparency, accountability, and ethical behavior, thereby fostering a strong audit culture. Internal control, on the other hand, encompasses the policies, procedures, and practices that protect assets, ensure accurate financial reporting, and comply with regulations. Governance structures provide the framework within which internal control operates, overseeing its functions and establishing mechanisms for accountability and reporting. The results of this research have important practical implications for accounting and audit firms and regulators.

期刊介绍:

The International Journal of Disclosure and Governance publishes a balance between academic and practitioner perspectives in law and accounting on subjects related to corporate governance and disclosure. In its emphasis on practical issues, it is the only such journal in these fields. All rigorous and thoughtful conceptual papers are encouraged.

To date, International Journal of Disclosure and Governance has published articles by a former general counsel and a former commissioner of the SEC, practitioners from Cleary Gottlieb, Skadden Arps, Wachtell Lipton, and Latham & Watkins as well as articles by academics from Harvard, Yale and NYU. The readership of the journal includes lawyers, accountants, and corporate directors and managers.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们