{"title":"对称正定矩阵分布空间内的新型双样本检验及其在金融领域的应用","authors":"Žikica Lukić, Bojana Milošević","doi":"10.1007/s10463-024-00902-z","DOIUrl":null,"url":null,"abstract":"<div><p>This paper introduces a novel two-sample test for a broad class of orthogonally invariant positive definite symmetric matrix distributions. Our test is the first of its kind, and we derive its asymptotic distribution. To estimate the test power, we use a warp-speed bootstrap method and consider the most common matrix distributions. We provide several real data examples, including the data for main cryptocurrencies and stock data of major US companies. The real data examples demonstrate the applicability of our test in the context closely related to algorithmic trading. The popularity of matrix distributions in many applications and the need for such a test in the literature are reconciled by our findings.</p></div>","PeriodicalId":55511,"journal":{"name":"Annals of the Institute of Statistical Mathematics","volume":null,"pages":null},"PeriodicalIF":0.8000,"publicationDate":"2024-04-08","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"","citationCount":"0","resultStr":"{\"title\":\"A novel two-sample test within the space of symmetric positive definite matrix distributions and its application in finance\",\"authors\":\"Žikica Lukić, Bojana Milošević\",\"doi\":\"10.1007/s10463-024-00902-z\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<div><p>This paper introduces a novel two-sample test for a broad class of orthogonally invariant positive definite symmetric matrix distributions. Our test is the first of its kind, and we derive its asymptotic distribution. To estimate the test power, we use a warp-speed bootstrap method and consider the most common matrix distributions. We provide several real data examples, including the data for main cryptocurrencies and stock data of major US companies. The real data examples demonstrate the applicability of our test in the context closely related to algorithmic trading. The popularity of matrix distributions in many applications and the need for such a test in the literature are reconciled by our findings.</p></div>\",\"PeriodicalId\":55511,\"journal\":{\"name\":\"Annals of the Institute of Statistical Mathematics\",\"volume\":null,\"pages\":null},\"PeriodicalIF\":0.8000,\"publicationDate\":\"2024-04-08\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Annals of the Institute of Statistical Mathematics\",\"FirstCategoryId\":\"100\",\"ListUrlMain\":\"https://link.springer.com/article/10.1007/s10463-024-00902-z\",\"RegionNum\":4,\"RegionCategory\":\"数学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q3\",\"JCRName\":\"STATISTICS & PROBABILITY\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Annals of the Institute of Statistical Mathematics","FirstCategoryId":"100","ListUrlMain":"https://link.springer.com/article/10.1007/s10463-024-00902-z","RegionNum":4,"RegionCategory":"数学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q3","JCRName":"STATISTICS & PROBABILITY","Score":null,"Total":0}

A novel two-sample test within the space of symmetric positive definite matrix distributions and its application in finance

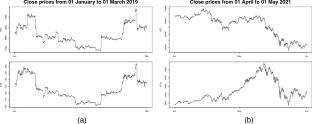

This paper introduces a novel two-sample test for a broad class of orthogonally invariant positive definite symmetric matrix distributions. Our test is the first of its kind, and we derive its asymptotic distribution. To estimate the test power, we use a warp-speed bootstrap method and consider the most common matrix distributions. We provide several real data examples, including the data for main cryptocurrencies and stock data of major US companies. The real data examples demonstrate the applicability of our test in the context closely related to algorithmic trading. The popularity of matrix distributions in many applications and the need for such a test in the literature are reconciled by our findings.

期刊介绍:

Annals of the Institute of Statistical Mathematics (AISM) aims to provide a forum for open communication among statisticians, and to contribute to the advancement of statistics as a science to enable humans to handle information in order to cope with uncertainties. It publishes high-quality papers that shed new light on the theoretical, computational and/or methodological aspects of statistical science. Emphasis is placed on (a) development of new methodologies motivated by real data, (b) development of unifying theories, and (c) analysis and improvement of existing methodologies and theories.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们