{"title":"年报可读性与陷入财务困境企业的盈利管理:印度所有权集中度的调节作用","authors":"Sweta Tiwari, Chanchal Chatterjee","doi":"10.1057/s41310-024-00238-3","DOIUrl":null,"url":null,"abstract":"<p>The present study investigates the impact of earnings management on the readability of financial disclosures of distressed Indian firms. It uses a sample of 545 management discussion and analysis sections of the annual report of 208 Indian financially distressed publicly traded firms for the period 2017–2021. Using multiple regression models, the study reveals a significant positive association between earnings management and the complexity of disclosures. This association is strongly moderated by the concentrated ownership of firms. Further, the impact of such moderation varies with the level of financial distress. The result is consistent for both accrual-based and real activity-based earnings management. This has significant implications for regulators, investors and analysts of the Indian stock market.</p>","PeriodicalId":45050,"journal":{"name":"International Journal of Disclosure and Governance","volume":"23 1","pages":""},"PeriodicalIF":2.4000,"publicationDate":"2024-04-09","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"","citationCount":"0","resultStr":"{\"title\":\"Annual report readability and earnings management of financial distressed firms: the moderating role of ownership concentration in India\",\"authors\":\"Sweta Tiwari, Chanchal Chatterjee\",\"doi\":\"10.1057/s41310-024-00238-3\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>The present study investigates the impact of earnings management on the readability of financial disclosures of distressed Indian firms. It uses a sample of 545 management discussion and analysis sections of the annual report of 208 Indian financially distressed publicly traded firms for the period 2017–2021. Using multiple regression models, the study reveals a significant positive association between earnings management and the complexity of disclosures. This association is strongly moderated by the concentrated ownership of firms. Further, the impact of such moderation varies with the level of financial distress. The result is consistent for both accrual-based and real activity-based earnings management. This has significant implications for regulators, investors and analysts of the Indian stock market.</p>\",\"PeriodicalId\":45050,\"journal\":{\"name\":\"International Journal of Disclosure and Governance\",\"volume\":\"23 1\",\"pages\":\"\"},\"PeriodicalIF\":2.4000,\"publicationDate\":\"2024-04-09\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"International Journal of Disclosure and Governance\",\"FirstCategoryId\":\"1085\",\"ListUrlMain\":\"https://doi.org/10.1057/s41310-024-00238-3\",\"RegionNum\":0,\"RegionCategory\":null,\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q2\",\"JCRName\":\"MANAGEMENT\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"International Journal of Disclosure and Governance","FirstCategoryId":"1085","ListUrlMain":"https://doi.org/10.1057/s41310-024-00238-3","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q2","JCRName":"MANAGEMENT","Score":null,"Total":0}

Annual report readability and earnings management of financial distressed firms: the moderating role of ownership concentration in India

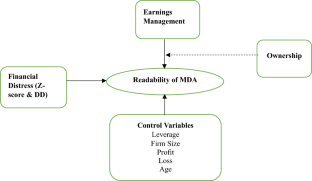

The present study investigates the impact of earnings management on the readability of financial disclosures of distressed Indian firms. It uses a sample of 545 management discussion and analysis sections of the annual report of 208 Indian financially distressed publicly traded firms for the period 2017–2021. Using multiple regression models, the study reveals a significant positive association between earnings management and the complexity of disclosures. This association is strongly moderated by the concentrated ownership of firms. Further, the impact of such moderation varies with the level of financial distress. The result is consistent for both accrual-based and real activity-based earnings management. This has significant implications for regulators, investors and analysts of the Indian stock market.

期刊介绍:

The International Journal of Disclosure and Governance publishes a balance between academic and practitioner perspectives in law and accounting on subjects related to corporate governance and disclosure. In its emphasis on practical issues, it is the only such journal in these fields. All rigorous and thoughtful conceptual papers are encouraged.

To date, International Journal of Disclosure and Governance has published articles by a former general counsel and a former commissioner of the SEC, practitioners from Cleary Gottlieb, Skadden Arps, Wachtell Lipton, and Latham & Watkins as well as articles by academics from Harvard, Yale and NYU. The readership of the journal includes lawyers, accountants, and corporate directors and managers.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们