{"title":"用均值场博弈法研究习惯养成的相对投资-消费博弈","authors":"Zongxia Liang, Keyu Zhang","doi":"10.1007/s11579-024-00360-4","DOIUrl":null,"url":null,"abstract":"<p>This paper studies an optimal investment–consumption problem for competitive agents with exponential or power utilities and a common finite time horizon. Each agent regards the average of habit formation and wealth from all peers as benchmarks to evaluate the performance of her decision. We formulate the <i>n</i>-agent game problems and the corresponding mean field game problems under the two utilities. One mean field equilibrium is derived in a closed form in each problem. In each problem with <i>n</i> agents, an approximate Nash equilibrium is then constructed using the obtained mean field equilibrium when <i>n</i> is sufficiently large. The explicit convergence order in each problem can also be obtained. In addition, we provide some numerical illustrations of our results.</p>","PeriodicalId":48722,"journal":{"name":"Mathematics and Financial Economics","volume":"148 1","pages":""},"PeriodicalIF":1.0000,"publicationDate":"2024-05-02","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"","citationCount":"0","resultStr":"{\"title\":\"A mean field game approach to relative investment–consumption games with habit formation\",\"authors\":\"Zongxia Liang, Keyu Zhang\",\"doi\":\"10.1007/s11579-024-00360-4\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>This paper studies an optimal investment–consumption problem for competitive agents with exponential or power utilities and a common finite time horizon. Each agent regards the average of habit formation and wealth from all peers as benchmarks to evaluate the performance of her decision. We formulate the <i>n</i>-agent game problems and the corresponding mean field game problems under the two utilities. One mean field equilibrium is derived in a closed form in each problem. In each problem with <i>n</i> agents, an approximate Nash equilibrium is then constructed using the obtained mean field equilibrium when <i>n</i> is sufficiently large. The explicit convergence order in each problem can also be obtained. In addition, we provide some numerical illustrations of our results.</p>\",\"PeriodicalId\":48722,\"journal\":{\"name\":\"Mathematics and Financial Economics\",\"volume\":\"148 1\",\"pages\":\"\"},\"PeriodicalIF\":1.0000,\"publicationDate\":\"2024-05-02\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Mathematics and Financial Economics\",\"FirstCategoryId\":\"96\",\"ListUrlMain\":\"https://doi.org/10.1007/s11579-024-00360-4\",\"RegionNum\":3,\"RegionCategory\":\"经济学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q3\",\"JCRName\":\"BUSINESS, FINANCE\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Mathematics and Financial Economics","FirstCategoryId":"96","ListUrlMain":"https://doi.org/10.1007/s11579-024-00360-4","RegionNum":3,"RegionCategory":"经济学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q3","JCRName":"BUSINESS, FINANCE","Score":null,"Total":0}

引用次数: 0

摘要

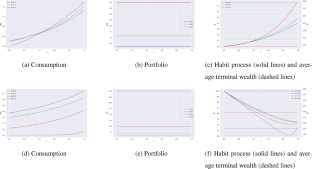

本文研究的是具有指数效用或幂效用以及共同有限时间跨度的竞争代理的最优投资-消费问题。每个代理都将所有同行的习惯养成和财富的平均值视为评估其决策绩效的基准。我们提出了两种效用下的 n 个代理博弈问题和相应的均值场博弈问题。每个问题都有一个均值场均衡。在每个有 n 个代理的问题中,当 n 足够大时,利用得到的均值场均衡构建近似纳什均衡。每个问题的收敛阶数也可以明确得到。此外,我们还提供了一些结果的数值说明。

A mean field game approach to relative investment–consumption games with habit formation

This paper studies an optimal investment–consumption problem for competitive agents with exponential or power utilities and a common finite time horizon. Each agent regards the average of habit formation and wealth from all peers as benchmarks to evaluate the performance of her decision. We formulate the n-agent game problems and the corresponding mean field game problems under the two utilities. One mean field equilibrium is derived in a closed form in each problem. In each problem with n agents, an approximate Nash equilibrium is then constructed using the obtained mean field equilibrium when n is sufficiently large. The explicit convergence order in each problem can also be obtained. In addition, we provide some numerical illustrations of our results.

期刊介绍:

The primary objective of the journal is to provide a forum for work in finance which expresses economic ideas using formal mathematical reasoning. The work should have real economic content and the mathematical reasoning should be new and correct.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们