{"title":"会计职业化(缺乏)进展:葡萄牙非会计师的见解","authors":"Fernanda Leão, Delfina Gomes","doi":"10.1111/auar.12420","DOIUrl":null,"url":null,"abstract":"<p>Concerns about the success of professional accountancy in terms of its social dimension have been expressed in the literature. This study uses data from a questionnaire survey administered to a Portuguese community sample to provide insights for a better understanding of the social dimension of professional accountancy at the macro level. It examines how lay society in accounting posits accountants along the social judgement variables of status, competition, competence and warmth and tests these variables’ influence on accountants’ social image using structural equation modelling. The results indicate that status, competition, competence and warmth are all critical factors in constructing the social image of modern accountants. Accountants are perceived as modestly warm, highly competent and a cooperative lower middle-class group. These findings confirm the profession's difficulties in enhancing accountants’ perceived social standing and reinforce the view of limited social mobility in the accountancy profession. The high level of competence identified suggests weak social power in the case of accountancy. Future research may investigate how soft skills and networking abilities in the perceived prototype of competence can promote the higher social standing of the accountancy group.</p>","PeriodicalId":51552,"journal":{"name":"Australian Accounting Review","volume":"34 2","pages":"133-155"},"PeriodicalIF":3.3000,"publicationDate":"2024-05-05","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1111/auar.12420","citationCount":"0","resultStr":"{\"title\":\"The (Lack of) Progress in Accountancy Professionalisation: Insights from Non-accountants in Portugal\",\"authors\":\"Fernanda Leão, Delfina Gomes\",\"doi\":\"10.1111/auar.12420\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>Concerns about the success of professional accountancy in terms of its social dimension have been expressed in the literature. This study uses data from a questionnaire survey administered to a Portuguese community sample to provide insights for a better understanding of the social dimension of professional accountancy at the macro level. It examines how lay society in accounting posits accountants along the social judgement variables of status, competition, competence and warmth and tests these variables’ influence on accountants’ social image using structural equation modelling. The results indicate that status, competition, competence and warmth are all critical factors in constructing the social image of modern accountants. Accountants are perceived as modestly warm, highly competent and a cooperative lower middle-class group. These findings confirm the profession's difficulties in enhancing accountants’ perceived social standing and reinforce the view of limited social mobility in the accountancy profession. The high level of competence identified suggests weak social power in the case of accountancy. Future research may investigate how soft skills and networking abilities in the perceived prototype of competence can promote the higher social standing of the accountancy group.</p>\",\"PeriodicalId\":51552,\"journal\":{\"name\":\"Australian Accounting Review\",\"volume\":\"34 2\",\"pages\":\"133-155\"},\"PeriodicalIF\":3.3000,\"publicationDate\":\"2024-05-05\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://onlinelibrary.wiley.com/doi/epdf/10.1111/auar.12420\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Australian Accounting Review\",\"FirstCategoryId\":\"91\",\"ListUrlMain\":\"https://onlinelibrary.wiley.com/doi/10.1111/auar.12420\",\"RegionNum\":3,\"RegionCategory\":\"管理学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q2\",\"JCRName\":\"BUSINESS, FINANCE\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Australian Accounting Review","FirstCategoryId":"91","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1111/auar.12420","RegionNum":3,"RegionCategory":"管理学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q2","JCRName":"BUSINESS, FINANCE","Score":null,"Total":0}

The (Lack of) Progress in Accountancy Professionalisation: Insights from Non-accountants in Portugal

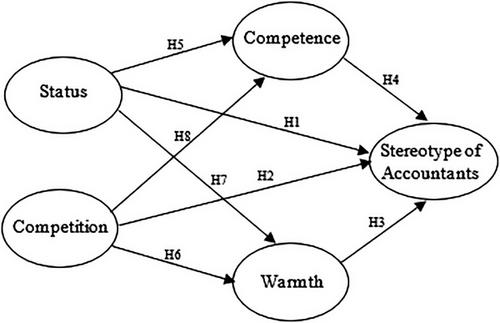

Concerns about the success of professional accountancy in terms of its social dimension have been expressed in the literature. This study uses data from a questionnaire survey administered to a Portuguese community sample to provide insights for a better understanding of the social dimension of professional accountancy at the macro level. It examines how lay society in accounting posits accountants along the social judgement variables of status, competition, competence and warmth and tests these variables’ influence on accountants’ social image using structural equation modelling. The results indicate that status, competition, competence and warmth are all critical factors in constructing the social image of modern accountants. Accountants are perceived as modestly warm, highly competent and a cooperative lower middle-class group. These findings confirm the profession's difficulties in enhancing accountants’ perceived social standing and reinforce the view of limited social mobility in the accountancy profession. The high level of competence identified suggests weak social power in the case of accountancy. Future research may investigate how soft skills and networking abilities in the perceived prototype of competence can promote the higher social standing of the accountancy group.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们