{"title":"南非 Twitter 政策的不确定性与股票回报:来自时变格兰杰因果关系的证据","authors":"Kingstone Nyakurukwa, Yudhvir Seetharam","doi":"10.1002/for.3148","DOIUrl":null,"url":null,"abstract":"<p>The study uses time-varying Granger causality models that incorporate two proxies for Twitter policy uncertainty and South African returns stock returns to investigate the causal relationship between Twitter uncertainty and South African stock returns for the period between 2017 and 2023. The findings demonstrate that Twitter Market Uncertainty and Twitter Economic Uncertainty mostly lead JSE returns around the start of the COVID-19 pandemic and the Russia-Ukranainan war respectively. The findings also show significant out-of-sample forecasts using uncertainty indexes from Twitter.</p>","PeriodicalId":47835,"journal":{"name":"Journal of Forecasting","volume":"43 7","pages":"2675-2684"},"PeriodicalIF":2.7000,"publicationDate":"2024-05-10","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1002/for.3148","citationCount":"0","resultStr":"{\"title\":\"Twitter policy uncertainty and stock returns in South Africa: Evidence from time-varying Granger causality\",\"authors\":\"Kingstone Nyakurukwa, Yudhvir Seetharam\",\"doi\":\"10.1002/for.3148\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>The study uses time-varying Granger causality models that incorporate two proxies for Twitter policy uncertainty and South African returns stock returns to investigate the causal relationship between Twitter uncertainty and South African stock returns for the period between 2017 and 2023. The findings demonstrate that Twitter Market Uncertainty and Twitter Economic Uncertainty mostly lead JSE returns around the start of the COVID-19 pandemic and the Russia-Ukranainan war respectively. The findings also show significant out-of-sample forecasts using uncertainty indexes from Twitter.</p>\",\"PeriodicalId\":47835,\"journal\":{\"name\":\"Journal of Forecasting\",\"volume\":\"43 7\",\"pages\":\"2675-2684\"},\"PeriodicalIF\":2.7000,\"publicationDate\":\"2024-05-10\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://onlinelibrary.wiley.com/doi/epdf/10.1002/for.3148\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Journal of Forecasting\",\"FirstCategoryId\":\"96\",\"ListUrlMain\":\"https://onlinelibrary.wiley.com/doi/10.1002/for.3148\",\"RegionNum\":3,\"RegionCategory\":\"经济学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q1\",\"JCRName\":\"ECONOMICS\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Journal of Forecasting","FirstCategoryId":"96","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1002/for.3148","RegionNum":3,"RegionCategory":"经济学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q1","JCRName":"ECONOMICS","Score":null,"Total":0}

Twitter policy uncertainty and stock returns in South Africa: Evidence from time-varying Granger causality

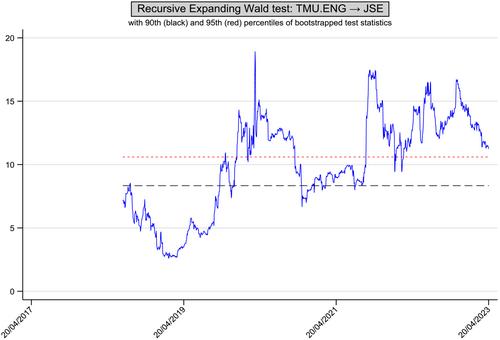

The study uses time-varying Granger causality models that incorporate two proxies for Twitter policy uncertainty and South African returns stock returns to investigate the causal relationship between Twitter uncertainty and South African stock returns for the period between 2017 and 2023. The findings demonstrate that Twitter Market Uncertainty and Twitter Economic Uncertainty mostly lead JSE returns around the start of the COVID-19 pandemic and the Russia-Ukranainan war respectively. The findings also show significant out-of-sample forecasts using uncertainty indexes from Twitter.

期刊介绍:

The Journal of Forecasting is an international journal that publishes refereed papers on forecasting. It is multidisciplinary, welcoming papers dealing with any aspect of forecasting: theoretical, practical, computational and methodological. A broad interpretation of the topic is taken with approaches from various subject areas, such as statistics, economics, psychology, systems engineering and social sciences, all encouraged. Furthermore, the Journal welcomes a wide diversity of applications in such fields as business, government, technology and the environment. Of particular interest are papers dealing with modelling issues and the relationship of forecasting systems to decision-making processes.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们