{"title":"测试基于调查的密度预期差异:组合数据方法","authors":"Jonas Dovern, Alexander Glas, Geoff Kenny","doi":"10.1002/jae.3080","DOIUrl":null,"url":null,"abstract":"<p>We propose to treat survey-based density expectations as compositional data when testing either for heterogeneity in density forecasts across different groups of agents or for changes over time. Monte Carlo simulations show that the proposed test has more power relative to both a bootstrap approach based on the KLIC and an approach that involves multiple testing for differences of individual parts of the density. In addition, the test is computationally much faster than the KLIC-based one, which relies on simulations, and allows for comparisons across multiple groups. Using density expectations from the ECB Survey of Professional Forecasters and the US Survey of Consumer Expectations, we show the usefulness of the test in detecting possible changes in density expectations over time and across different types of forecasters.</p>","PeriodicalId":48363,"journal":{"name":"Journal of Applied Econometrics","volume":"39 6","pages":"1104-1122"},"PeriodicalIF":3.1000,"publicationDate":"2024-06-24","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1002/jae.3080","citationCount":"0","resultStr":"{\"title\":\"Testing for differences in survey-based density expectations: A compositional data approach\",\"authors\":\"Jonas Dovern, Alexander Glas, Geoff Kenny\",\"doi\":\"10.1002/jae.3080\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>We propose to treat survey-based density expectations as compositional data when testing either for heterogeneity in density forecasts across different groups of agents or for changes over time. Monte Carlo simulations show that the proposed test has more power relative to both a bootstrap approach based on the KLIC and an approach that involves multiple testing for differences of individual parts of the density. In addition, the test is computationally much faster than the KLIC-based one, which relies on simulations, and allows for comparisons across multiple groups. Using density expectations from the ECB Survey of Professional Forecasters and the US Survey of Consumer Expectations, we show the usefulness of the test in detecting possible changes in density expectations over time and across different types of forecasters.</p>\",\"PeriodicalId\":48363,\"journal\":{\"name\":\"Journal of Applied Econometrics\",\"volume\":\"39 6\",\"pages\":\"1104-1122\"},\"PeriodicalIF\":3.1000,\"publicationDate\":\"2024-06-24\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://onlinelibrary.wiley.com/doi/epdf/10.1002/jae.3080\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Journal of Applied Econometrics\",\"FirstCategoryId\":\"96\",\"ListUrlMain\":\"https://onlinelibrary.wiley.com/doi/10.1002/jae.3080\",\"RegionNum\":3,\"RegionCategory\":\"经济学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q2\",\"JCRName\":\"ECONOMICS\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Journal of Applied Econometrics","FirstCategoryId":"96","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1002/jae.3080","RegionNum":3,"RegionCategory":"经济学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q2","JCRName":"ECONOMICS","Score":null,"Total":0}

Testing for differences in survey-based density expectations: A compositional data approach

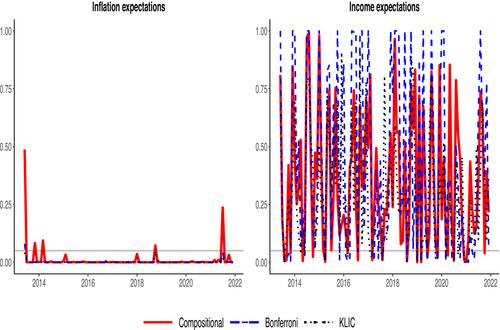

We propose to treat survey-based density expectations as compositional data when testing either for heterogeneity in density forecasts across different groups of agents or for changes over time. Monte Carlo simulations show that the proposed test has more power relative to both a bootstrap approach based on the KLIC and an approach that involves multiple testing for differences of individual parts of the density. In addition, the test is computationally much faster than the KLIC-based one, which relies on simulations, and allows for comparisons across multiple groups. Using density expectations from the ECB Survey of Professional Forecasters and the US Survey of Consumer Expectations, we show the usefulness of the test in detecting possible changes in density expectations over time and across different types of forecasters.

期刊介绍:

The Journal of Applied Econometrics is an international journal published bi-monthly, plus 1 additional issue (total 7 issues). It aims to publish articles of high quality dealing with the application of existing as well as new econometric techniques to a wide variety of problems in economics and related subjects, covering topics in measurement, estimation, testing, forecasting, and policy analysis. The emphasis is on the careful and rigorous application of econometric techniques and the appropriate interpretation of the results. The economic content of the articles is stressed. A special feature of the Journal is its emphasis on the replicability of results by other researchers. To achieve this aim, authors are expected to make available a complete set of the data used as well as any specialised computer programs employed through a readily accessible medium, preferably in a machine-readable form. The use of microcomputers in applied research and transferability of data is emphasised. The Journal also features occasional sections of short papers re-evaluating previously published papers. The intention of the Journal of Applied Econometrics is to provide an outlet for innovative, quantitative research in economics which cuts across areas of specialisation, involves transferable techniques, and is easily replicable by other researchers. Contributions that introduce statistical methods that are applicable to a variety of economic problems are actively encouraged. The Journal also aims to publish review and survey articles that make recent developments in the field of theoretical and applied econometrics more readily accessible to applied economists in general.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们