{"title":"反馈交易:零售衍生品的日内交易案例","authors":"Rainer Baule, Bart Frijns, Sebastian Schlie","doi":"10.1002/fut.22536","DOIUrl":null,"url":null,"abstract":"<p>We analyze retail order flow in terms of intraday feedback trading patterns. Using a unique data set of exchange trades and high-frequency quotes, we first provide evidence that retail investors actively and consciously respond to short-term intraday returns in a negative feedback, contrarian fashion. Second, we show that some retail investors also feedback trade on tick-by-tick returns. Third, we find that on average this behavior leads to significant losses on the day they open a position. These losses are primarily due to the bid-ask spread and to investors' timing inability, but not to market makers taking advantage of investors.</p>","PeriodicalId":15863,"journal":{"name":"Journal of Futures Markets","volume":"44 9","pages":"1487-1507"},"PeriodicalIF":2.3000,"publicationDate":"2024-06-26","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1002/fut.22536","citationCount":"0","resultStr":"{\"title\":\"Feedback Trading: The Intraday Case of Retail Derivatives\",\"authors\":\"Rainer Baule, Bart Frijns, Sebastian Schlie\",\"doi\":\"10.1002/fut.22536\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>We analyze retail order flow in terms of intraday feedback trading patterns. Using a unique data set of exchange trades and high-frequency quotes, we first provide evidence that retail investors actively and consciously respond to short-term intraday returns in a negative feedback, contrarian fashion. Second, we show that some retail investors also feedback trade on tick-by-tick returns. Third, we find that on average this behavior leads to significant losses on the day they open a position. These losses are primarily due to the bid-ask spread and to investors' timing inability, but not to market makers taking advantage of investors.</p>\",\"PeriodicalId\":15863,\"journal\":{\"name\":\"Journal of Futures Markets\",\"volume\":\"44 9\",\"pages\":\"1487-1507\"},\"PeriodicalIF\":2.3000,\"publicationDate\":\"2024-06-26\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://onlinelibrary.wiley.com/doi/epdf/10.1002/fut.22536\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Journal of Futures Markets\",\"FirstCategoryId\":\"96\",\"ListUrlMain\":\"https://onlinelibrary.wiley.com/doi/10.1002/fut.22536\",\"RegionNum\":4,\"RegionCategory\":\"经济学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q2\",\"JCRName\":\"BUSINESS, FINANCE\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Journal of Futures Markets","FirstCategoryId":"96","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1002/fut.22536","RegionNum":4,"RegionCategory":"经济学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q2","JCRName":"BUSINESS, FINANCE","Score":null,"Total":0}

Feedback Trading: The Intraday Case of Retail Derivatives

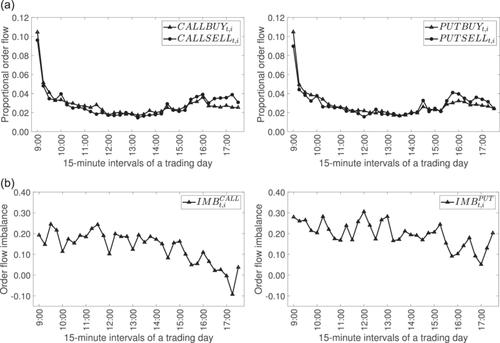

We analyze retail order flow in terms of intraday feedback trading patterns. Using a unique data set of exchange trades and high-frequency quotes, we first provide evidence that retail investors actively and consciously respond to short-term intraday returns in a negative feedback, contrarian fashion. Second, we show that some retail investors also feedback trade on tick-by-tick returns. Third, we find that on average this behavior leads to significant losses on the day they open a position. These losses are primarily due to the bid-ask spread and to investors' timing inability, but not to market makers taking advantage of investors.

期刊介绍:

The Journal of Futures Markets chronicles the latest developments in financial futures and derivatives. It publishes timely, innovative articles written by leading finance academics and professionals. Coverage ranges from the highly practical to theoretical topics that include futures, derivatives, risk management and control, financial engineering, new financial instruments, hedging strategies, analysis of trading systems, legal, accounting, and regulatory issues, and portfolio optimization. This publication contains the very latest research from the top experts.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们