{"title":"重启《社区再投资法","authors":"Lindsay Sain Jones, Goldburn Maynard Jr.","doi":"10.1111/ablj.12247","DOIUrl":null,"url":null,"abstract":"<p>The Community Reinvestment Act (CRA) was passed in 1977 as a response to redlining, the systemic discrimination against loan applicants who resided in predominantly Black neighborhoods. In enacting the CRA, Congress found that banks have a “continuing and affirmative obligation” to help meet the credit needs of the communities in which they are chartered. To that end, the CRA requires bank regulators to rate the record of each bank in fulfilling these obligations. While much has changed since 1977, some things have not. Financial services are now provided by a much broader set of entities including financial technology (fintech) firms, yet the CRA's mandates still just apply to banks. In addition, while the demographic compositions of neighborhoods have changed since 1977, Black applicants are still 2.5 times more likely than White applicants to be rejected for a home loan. On October 24, 2023, the banking agencies jointly issued final rules to “strengthen and modernize” the agencies' CRA regulations. While the updated rules do inject more objectivity in order to address persistent concerns about CRA ratings inflation, we contend that further amendments are needed to account for what has changed and what has not changed since its original enactment. In this article, we argue that the CRA continues to be a worthwhile endeavor, as it addresses gaps left by fair lending laws. To further its impact and address its many shortcomings though, we contend the CRA should be amended to also apply to nonbanks that provide financial services, to counter discrimination more directly, and to calculate CRA ratings more objectively.</p>","PeriodicalId":54186,"journal":{"name":"American Business Law Journal","volume":"61 3","pages":"167-190"},"PeriodicalIF":1.3000,"publicationDate":"2024-07-25","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1111/ablj.12247","citationCount":"0","resultStr":"{\"title\":\"Rebooting the Community Reinvestment Act\",\"authors\":\"Lindsay Sain Jones, Goldburn Maynard Jr.\",\"doi\":\"10.1111/ablj.12247\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>The Community Reinvestment Act (CRA) was passed in 1977 as a response to redlining, the systemic discrimination against loan applicants who resided in predominantly Black neighborhoods. In enacting the CRA, Congress found that banks have a “continuing and affirmative obligation” to help meet the credit needs of the communities in which they are chartered. To that end, the CRA requires bank regulators to rate the record of each bank in fulfilling these obligations. While much has changed since 1977, some things have not. Financial services are now provided by a much broader set of entities including financial technology (fintech) firms, yet the CRA's mandates still just apply to banks. In addition, while the demographic compositions of neighborhoods have changed since 1977, Black applicants are still 2.5 times more likely than White applicants to be rejected for a home loan. On October 24, 2023, the banking agencies jointly issued final rules to “strengthen and modernize” the agencies' CRA regulations. While the updated rules do inject more objectivity in order to address persistent concerns about CRA ratings inflation, we contend that further amendments are needed to account for what has changed and what has not changed since its original enactment. In this article, we argue that the CRA continues to be a worthwhile endeavor, as it addresses gaps left by fair lending laws. To further its impact and address its many shortcomings though, we contend the CRA should be amended to also apply to nonbanks that provide financial services, to counter discrimination more directly, and to calculate CRA ratings more objectively.</p>\",\"PeriodicalId\":54186,\"journal\":{\"name\":\"American Business Law Journal\",\"volume\":\"61 3\",\"pages\":\"167-190\"},\"PeriodicalIF\":1.3000,\"publicationDate\":\"2024-07-25\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://onlinelibrary.wiley.com/doi/epdf/10.1111/ablj.12247\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"American Business Law Journal\",\"FirstCategoryId\":\"90\",\"ListUrlMain\":\"https://onlinelibrary.wiley.com/doi/10.1111/ablj.12247\",\"RegionNum\":3,\"RegionCategory\":\"社会学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q3\",\"JCRName\":\"BUSINESS\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"American Business Law Journal","FirstCategoryId":"90","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1111/ablj.12247","RegionNum":3,"RegionCategory":"社会学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q3","JCRName":"BUSINESS","Score":null,"Total":0}

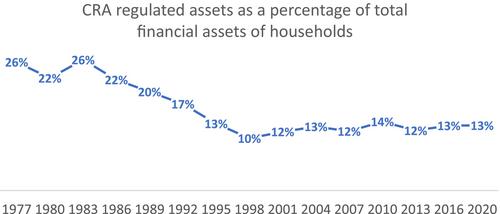

The Community Reinvestment Act (CRA) was passed in 1977 as a response to redlining, the systemic discrimination against loan applicants who resided in predominantly Black neighborhoods. In enacting the CRA, Congress found that banks have a “continuing and affirmative obligation” to help meet the credit needs of the communities in which they are chartered. To that end, the CRA requires bank regulators to rate the record of each bank in fulfilling these obligations. While much has changed since 1977, some things have not. Financial services are now provided by a much broader set of entities including financial technology (fintech) firms, yet the CRA's mandates still just apply to banks. In addition, while the demographic compositions of neighborhoods have changed since 1977, Black applicants are still 2.5 times more likely than White applicants to be rejected for a home loan. On October 24, 2023, the banking agencies jointly issued final rules to “strengthen and modernize” the agencies' CRA regulations. While the updated rules do inject more objectivity in order to address persistent concerns about CRA ratings inflation, we contend that further amendments are needed to account for what has changed and what has not changed since its original enactment. In this article, we argue that the CRA continues to be a worthwhile endeavor, as it addresses gaps left by fair lending laws. To further its impact and address its many shortcomings though, we contend the CRA should be amended to also apply to nonbanks that provide financial services, to counter discrimination more directly, and to calculate CRA ratings more objectively.

期刊介绍:

The ABLJ is a faculty-edited, double blind peer reviewed journal, continuously published since 1963. Our mission is to publish only top quality law review articles that make a scholarly contribution to all areas of law that impact business theory and practice. We search for those articles that articulate a novel research question and make a meaningful contribution directly relevant to scholars and practitioners of business law. The blind peer review process means legal scholars well-versed in the relevant specialty area have determined selected articles are original, thorough, important, and timely. Faculty editors assure the authors’ contribution to scholarship is evident. We aim to elevate legal scholarship and inform responsible business decisions.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们