{"title":"功能性油价预期冲击与通货膨胀","authors":"Christina Anderl, Guglielmo Maria Caporale","doi":"10.1002/fut.22540","DOIUrl":null,"url":null,"abstract":"<p>This paper investigates the inflation effects of oil price expectations shocks constructed as functional shocks, that is, as shifts in the entire oil futures term structure (both standard and risk-adjusted). The latter are then included in a vector autoregressive model with exogenous variables (VARX) to examine the US case. Counterfactual analysis is also carried out to investigate second-round effects on inflation through the inflation expectations channel. These are found to be significant, in contrast to earlier studies based on standard oil price shocks. Additional nonlinear local projections including a shock decomposition exercise show that inflation and inflation expectations are primarily driven by changes in the curvature (level and slope) factor when the latter are anchored (unanchored). These findings provide useful information to policymakers concerning the impact of oil price expectations on inflation and inflation expectations.</p>","PeriodicalId":15863,"journal":{"name":"Journal of Futures Markets","volume":"44 10","pages":"1662-1693"},"PeriodicalIF":2.8000,"publicationDate":"2024-07-23","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1002/fut.22540","citationCount":"0","resultStr":"{\"title\":\"Functional Oil Price Expectations Shocks and Inflation\",\"authors\":\"Christina Anderl, Guglielmo Maria Caporale\",\"doi\":\"10.1002/fut.22540\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>This paper investigates the inflation effects of oil price expectations shocks constructed as functional shocks, that is, as shifts in the entire oil futures term structure (both standard and risk-adjusted). The latter are then included in a vector autoregressive model with exogenous variables (VARX) to examine the US case. Counterfactual analysis is also carried out to investigate second-round effects on inflation through the inflation expectations channel. These are found to be significant, in contrast to earlier studies based on standard oil price shocks. Additional nonlinear local projections including a shock decomposition exercise show that inflation and inflation expectations are primarily driven by changes in the curvature (level and slope) factor when the latter are anchored (unanchored). These findings provide useful information to policymakers concerning the impact of oil price expectations on inflation and inflation expectations.</p>\",\"PeriodicalId\":15863,\"journal\":{\"name\":\"Journal of Futures Markets\",\"volume\":\"44 10\",\"pages\":\"1662-1693\"},\"PeriodicalIF\":2.8000,\"publicationDate\":\"2024-07-23\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://onlinelibrary.wiley.com/doi/epdf/10.1002/fut.22540\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Journal of Futures Markets\",\"FirstCategoryId\":\"96\",\"ListUrlMain\":\"https://onlinelibrary.wiley.com/doi/10.1002/fut.22540\",\"RegionNum\":4,\"RegionCategory\":\"经济学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q2\",\"JCRName\":\"BUSINESS, FINANCE\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Journal of Futures Markets","FirstCategoryId":"96","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1002/fut.22540","RegionNum":4,"RegionCategory":"经济学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q2","JCRName":"BUSINESS, FINANCE","Score":null,"Total":0}

Functional Oil Price Expectations Shocks and Inflation

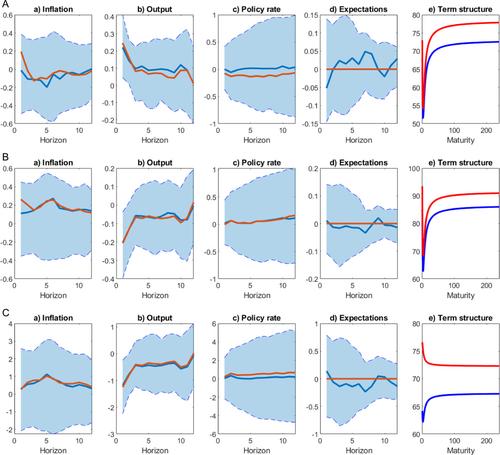

This paper investigates the inflation effects of oil price expectations shocks constructed as functional shocks, that is, as shifts in the entire oil futures term structure (both standard and risk-adjusted). The latter are then included in a vector autoregressive model with exogenous variables (VARX) to examine the US case. Counterfactual analysis is also carried out to investigate second-round effects on inflation through the inflation expectations channel. These are found to be significant, in contrast to earlier studies based on standard oil price shocks. Additional nonlinear local projections including a shock decomposition exercise show that inflation and inflation expectations are primarily driven by changes in the curvature (level and slope) factor when the latter are anchored (unanchored). These findings provide useful information to policymakers concerning the impact of oil price expectations on inflation and inflation expectations.

期刊介绍:

The Journal of Futures Markets chronicles the latest developments in financial futures and derivatives. It publishes timely, innovative articles written by leading finance academics and professionals. Coverage ranges from the highly practical to theoretical topics that include futures, derivatives, risk management and control, financial engineering, new financial instruments, hedging strategies, analysis of trading systems, legal, accounting, and regulatory issues, and portfolio optimization. This publication contains the very latest research from the top experts.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们