{"title":"非因果自回归的预测性能和单位根预检验的重要性","authors":"Frédérique Bec, Heino Bohn Nielsen","doi":"10.1002/for.3172","DOIUrl":null,"url":null,"abstract":"<p>Based on a large simulation study, this paper investigates which strategy to adopt in order to choose the most accurate forecasting model for mixed causal-noncausal autoregressions (MAR) data generating processes: always differencing (D), never differencing (L), or unit root pretesting (P). Relying on recent econometric developments regarding forecasting and unit root testing in the MAR framework, the main results suggest that from a practitioner's point of view, the P strategy at the 10% level is a good compromise. In fact, it never departs too much from the best model in terms of forecast accuracy, unlike the L (respectively, D) strategy when the DGP becomes very persistent (respectively, less persistent). This approach is illustrated using recent monthly Brent crude oil price data.</p>","PeriodicalId":47835,"journal":{"name":"Journal of Forecasting","volume":"43 8","pages":"3072-3088"},"PeriodicalIF":2.7000,"publicationDate":"2024-07-31","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1002/for.3172","citationCount":"0","resultStr":"{\"title\":\"Forecast performance of noncausal autoregressions and the importance of unit root pretesting\",\"authors\":\"Frédérique Bec, Heino Bohn Nielsen\",\"doi\":\"10.1002/for.3172\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>Based on a large simulation study, this paper investigates which strategy to adopt in order to choose the most accurate forecasting model for mixed causal-noncausal autoregressions (MAR) data generating processes: always differencing (D), never differencing (L), or unit root pretesting (P). Relying on recent econometric developments regarding forecasting and unit root testing in the MAR framework, the main results suggest that from a practitioner's point of view, the P strategy at the 10% level is a good compromise. In fact, it never departs too much from the best model in terms of forecast accuracy, unlike the L (respectively, D) strategy when the DGP becomes very persistent (respectively, less persistent). This approach is illustrated using recent monthly Brent crude oil price data.</p>\",\"PeriodicalId\":47835,\"journal\":{\"name\":\"Journal of Forecasting\",\"volume\":\"43 8\",\"pages\":\"3072-3088\"},\"PeriodicalIF\":2.7000,\"publicationDate\":\"2024-07-31\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://onlinelibrary.wiley.com/doi/epdf/10.1002/for.3172\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Journal of Forecasting\",\"FirstCategoryId\":\"96\",\"ListUrlMain\":\"https://onlinelibrary.wiley.com/doi/10.1002/for.3172\",\"RegionNum\":3,\"RegionCategory\":\"经济学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q1\",\"JCRName\":\"ECONOMICS\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Journal of Forecasting","FirstCategoryId":"96","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1002/for.3172","RegionNum":3,"RegionCategory":"经济学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q1","JCRName":"ECONOMICS","Score":null,"Total":0}

引用次数: 0

摘要

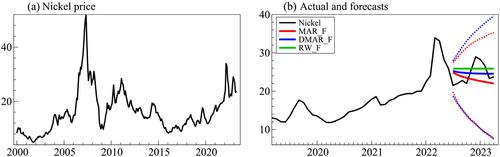

本文基于一项大型模拟研究,探讨了在因果-非因果混合自回归(MAR)数据生成过程中,应采用哪种策略来选择最准确的预测模型:始终差分(D)、从不差分(L)或单位根预测(P)。根据 MAR 框架中有关预测和单位根检验的最新计量经济学发展,主要结果表明,从实践者的角度来看,10% 水平的 P 策略是一个很好的折衷方案。事实上,就预测准确性而言,它从未偏离最佳模型太多,不像 L(分别为 D)策略那样在 DGP 变得非常持久(分别为较不持久)时那样。我们用最近的布伦特原油月度价格数据来说明这种方法。

Forecast performance of noncausal autoregressions and the importance of unit root pretesting

Based on a large simulation study, this paper investigates which strategy to adopt in order to choose the most accurate forecasting model for mixed causal-noncausal autoregressions (MAR) data generating processes: always differencing (D), never differencing (L), or unit root pretesting (P). Relying on recent econometric developments regarding forecasting and unit root testing in the MAR framework, the main results suggest that from a practitioner's point of view, the P strategy at the 10% level is a good compromise. In fact, it never departs too much from the best model in terms of forecast accuracy, unlike the L (respectively, D) strategy when the DGP becomes very persistent (respectively, less persistent). This approach is illustrated using recent monthly Brent crude oil price data.

期刊介绍:

The Journal of Forecasting is an international journal that publishes refereed papers on forecasting. It is multidisciplinary, welcoming papers dealing with any aspect of forecasting: theoretical, practical, computational and methodological. A broad interpretation of the topic is taken with approaches from various subject areas, such as statistics, economics, psychology, systems engineering and social sciences, all encouraged. Furthermore, the Journal welcomes a wide diversity of applications in such fields as business, government, technology and the environment. Of particular interest are papers dealing with modelling issues and the relationship of forecasting systems to decision-making processes.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们