{"title":"投资者情绪、意外通胀和比特币基础风险","authors":"Thomas Conlon, Shaen Corbet, Les Oxley","doi":"10.1002/fut.22541","DOIUrl":null,"url":null,"abstract":"<p>The introduction of regulated CME futures contracts on Bitcoin in 2017 raised an expectation that cryptocurrencies would become part of mainstream financial markets. This also heightened links between traditional markets and Bitcoin, implying that the cryptocurrency would be subject to systematic spillovers. This paper uses high-frequency data to examine whether Bitcoin basis risk is linked to investor sentiment from established financial markets. Our findings indicate that extreme investor sentiment, as reflected by the tail risk in various volatility indices, including the VIX, consistently correlates with a negative Bitcoin basis, where Bitcoin futures prices are lower than spot prices. Fluctuations significantly influence this relationship in the trading volume of Bitcoin futures and are more pronounced during periods of substantial unexpected inflation and deflation. These results underline the complex dynamics between market sentiment and cryptocurrency pricing, offering insights with substantial implications for investors and policymakers.</p>","PeriodicalId":15863,"journal":{"name":"Journal of Futures Markets","volume":"44 11","pages":"1807-1831"},"PeriodicalIF":2.3000,"publicationDate":"2024-08-12","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1002/fut.22541","citationCount":"0","resultStr":"{\"title\":\"Investor Sentiment, Unexpected Inflation, and Bitcoin Basis Risk\",\"authors\":\"Thomas Conlon, Shaen Corbet, Les Oxley\",\"doi\":\"10.1002/fut.22541\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>The introduction of regulated CME futures contracts on Bitcoin in 2017 raised an expectation that cryptocurrencies would become part of mainstream financial markets. This also heightened links between traditional markets and Bitcoin, implying that the cryptocurrency would be subject to systematic spillovers. This paper uses high-frequency data to examine whether Bitcoin basis risk is linked to investor sentiment from established financial markets. Our findings indicate that extreme investor sentiment, as reflected by the tail risk in various volatility indices, including the VIX, consistently correlates with a negative Bitcoin basis, where Bitcoin futures prices are lower than spot prices. Fluctuations significantly influence this relationship in the trading volume of Bitcoin futures and are more pronounced during periods of substantial unexpected inflation and deflation. These results underline the complex dynamics between market sentiment and cryptocurrency pricing, offering insights with substantial implications for investors and policymakers.</p>\",\"PeriodicalId\":15863,\"journal\":{\"name\":\"Journal of Futures Markets\",\"volume\":\"44 11\",\"pages\":\"1807-1831\"},\"PeriodicalIF\":2.3000,\"publicationDate\":\"2024-08-12\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://onlinelibrary.wiley.com/doi/epdf/10.1002/fut.22541\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Journal of Futures Markets\",\"FirstCategoryId\":\"96\",\"ListUrlMain\":\"https://onlinelibrary.wiley.com/doi/10.1002/fut.22541\",\"RegionNum\":4,\"RegionCategory\":\"经济学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q2\",\"JCRName\":\"BUSINESS, FINANCE\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Journal of Futures Markets","FirstCategoryId":"96","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1002/fut.22541","RegionNum":4,"RegionCategory":"经济学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q2","JCRName":"BUSINESS, FINANCE","Score":null,"Total":0}

Investor Sentiment, Unexpected Inflation, and Bitcoin Basis Risk

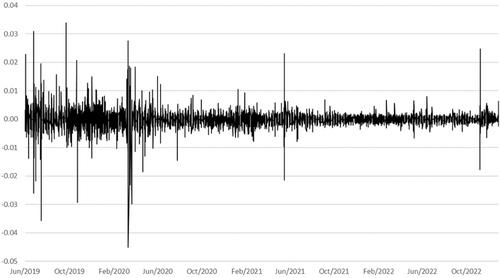

The introduction of regulated CME futures contracts on Bitcoin in 2017 raised an expectation that cryptocurrencies would become part of mainstream financial markets. This also heightened links between traditional markets and Bitcoin, implying that the cryptocurrency would be subject to systematic spillovers. This paper uses high-frequency data to examine whether Bitcoin basis risk is linked to investor sentiment from established financial markets. Our findings indicate that extreme investor sentiment, as reflected by the tail risk in various volatility indices, including the VIX, consistently correlates with a negative Bitcoin basis, where Bitcoin futures prices are lower than spot prices. Fluctuations significantly influence this relationship in the trading volume of Bitcoin futures and are more pronounced during periods of substantial unexpected inflation and deflation. These results underline the complex dynamics between market sentiment and cryptocurrency pricing, offering insights with substantial implications for investors and policymakers.

期刊介绍:

The Journal of Futures Markets chronicles the latest developments in financial futures and derivatives. It publishes timely, innovative articles written by leading finance academics and professionals. Coverage ranges from the highly practical to theoretical topics that include futures, derivatives, risk management and control, financial engineering, new financial instruments, hedging strategies, analysis of trading systems, legal, accounting, and regulatory issues, and portfolio optimization. This publication contains the very latest research from the top experts.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们