{"title":"赫斯顿随机波动率模型下欧式和美式期权定价的计算研究:SUPG-YZ $$\\beta$$ 公式的应用","authors":"Süleyman Cengizci, Ömür Uğur","doi":"10.1007/s10614-024-10704-3","DOIUrl":null,"url":null,"abstract":"<p>The interest of this paper is stabilized finite element approximations for pricing European- and American-type options under Heston’s stochastic volatility model, a generalization of the eminent Black–Scholes–Merton (BSM) framework in which volatility is treated as a constant. For spatial discretizations, the streamline-upwind/Petrov–Galerkin (SUPG) stabilized finite element method is used. The stabilized formulation is also supplemented with a shock-capturing mechanism, the so-called YZ<span>\\(\\beta\\)</span> technique, in order to resolve localized sharp layers. The semi-discrete problems, i.e., the systems of time-dependent ordinary differential equations, are discretized in time with the Crank–Nicolson (CN) time-integration scheme. The resulting nonlinear algebraic equation systems are solved with the Newton–Raphson (NR) iterative process. The stabilized bi-conjugate gradient method, preconditioned with the incomplete lower–upper factorization technique, is employed for solving linearized systems. The linear complementarity problems arising in simulating American-type options are handled with an efficient and practical penalty approach, which comes at the cost of introducing a nonlinear source term to the fully discretized formulation. The in-house-developed solvers are verified first for the Heston model with a manufactured solution. Following that, the performances of the proposed method and techniques are evaluated on various test problems, including the digital options, through comparisons with other reported results. In addition to those studied previously, we also introduce new “challenging” parameter sets through which Heston’s model becomes much more convection-dominated and demonstrate the robustness of the proposed formulation and techniques for such cases. Furthermore, for each test case, the results obtained with the classical Galerkin finite element method and SUPG alone without shock-capturing are also presented, revealing that the SUPG-YZ<span>\\(\\beta\\)</span> does not degrade the accuracy by introducing excessive numerical dissipation.</p>","PeriodicalId":50647,"journal":{"name":"Computational Economics","volume":"59 1","pages":""},"PeriodicalIF":2.2000,"publicationDate":"2024-08-23","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"","citationCount":"0","resultStr":"{\"title\":\"A Computational Study for Pricing European- and American-Type Options Under Heston’s Stochastic Volatility Model: Application of the SUPG-YZ $$\\\\beta$$ Formulation\",\"authors\":\"Süleyman Cengizci, Ömür Uğur\",\"doi\":\"10.1007/s10614-024-10704-3\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>The interest of this paper is stabilized finite element approximations for pricing European- and American-type options under Heston’s stochastic volatility model, a generalization of the eminent Black–Scholes–Merton (BSM) framework in which volatility is treated as a constant. For spatial discretizations, the streamline-upwind/Petrov–Galerkin (SUPG) stabilized finite element method is used. The stabilized formulation is also supplemented with a shock-capturing mechanism, the so-called YZ<span>\\\\(\\\\beta\\\\)</span> technique, in order to resolve localized sharp layers. The semi-discrete problems, i.e., the systems of time-dependent ordinary differential equations, are discretized in time with the Crank–Nicolson (CN) time-integration scheme. The resulting nonlinear algebraic equation systems are solved with the Newton–Raphson (NR) iterative process. The stabilized bi-conjugate gradient method, preconditioned with the incomplete lower–upper factorization technique, is employed for solving linearized systems. The linear complementarity problems arising in simulating American-type options are handled with an efficient and practical penalty approach, which comes at the cost of introducing a nonlinear source term to the fully discretized formulation. The in-house-developed solvers are verified first for the Heston model with a manufactured solution. Following that, the performances of the proposed method and techniques are evaluated on various test problems, including the digital options, through comparisons with other reported results. In addition to those studied previously, we also introduce new “challenging” parameter sets through which Heston’s model becomes much more convection-dominated and demonstrate the robustness of the proposed formulation and techniques for such cases. Furthermore, for each test case, the results obtained with the classical Galerkin finite element method and SUPG alone without shock-capturing are also presented, revealing that the SUPG-YZ<span>\\\\(\\\\beta\\\\)</span> does not degrade the accuracy by introducing excessive numerical dissipation.</p>\",\"PeriodicalId\":50647,\"journal\":{\"name\":\"Computational Economics\",\"volume\":\"59 1\",\"pages\":\"\"},\"PeriodicalIF\":2.2000,\"publicationDate\":\"2024-08-23\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Computational Economics\",\"FirstCategoryId\":\"96\",\"ListUrlMain\":\"https://doi.org/10.1007/s10614-024-10704-3\",\"RegionNum\":4,\"RegionCategory\":\"经济学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q2\",\"JCRName\":\"ECONOMICS\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Computational Economics","FirstCategoryId":"96","ListUrlMain":"https://doi.org/10.1007/s10614-024-10704-3","RegionNum":4,"RegionCategory":"经济学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q2","JCRName":"ECONOMICS","Score":null,"Total":0}

A Computational Study for Pricing European- and American-Type Options Under Heston’s Stochastic Volatility Model: Application of the SUPG-YZ $$\beta$$ Formulation

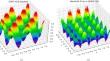

The interest of this paper is stabilized finite element approximations for pricing European- and American-type options under Heston’s stochastic volatility model, a generalization of the eminent Black–Scholes–Merton (BSM) framework in which volatility is treated as a constant. For spatial discretizations, the streamline-upwind/Petrov–Galerkin (SUPG) stabilized finite element method is used. The stabilized formulation is also supplemented with a shock-capturing mechanism, the so-called YZ\(\beta\) technique, in order to resolve localized sharp layers. The semi-discrete problems, i.e., the systems of time-dependent ordinary differential equations, are discretized in time with the Crank–Nicolson (CN) time-integration scheme. The resulting nonlinear algebraic equation systems are solved with the Newton–Raphson (NR) iterative process. The stabilized bi-conjugate gradient method, preconditioned with the incomplete lower–upper factorization technique, is employed for solving linearized systems. The linear complementarity problems arising in simulating American-type options are handled with an efficient and practical penalty approach, which comes at the cost of introducing a nonlinear source term to the fully discretized formulation. The in-house-developed solvers are verified first for the Heston model with a manufactured solution. Following that, the performances of the proposed method and techniques are evaluated on various test problems, including the digital options, through comparisons with other reported results. In addition to those studied previously, we also introduce new “challenging” parameter sets through which Heston’s model becomes much more convection-dominated and demonstrate the robustness of the proposed formulation and techniques for such cases. Furthermore, for each test case, the results obtained with the classical Galerkin finite element method and SUPG alone without shock-capturing are also presented, revealing that the SUPG-YZ\(\beta\) does not degrade the accuracy by introducing excessive numerical dissipation.

期刊介绍:

Computational Economics, the official journal of the Society for Computational Economics, presents new research in a rapidly growing multidisciplinary field that uses advanced computing capabilities to understand and solve complex problems from all branches in economics. The topics of Computational Economics include computational methods in econometrics like filtering, bayesian and non-parametric approaches, markov processes and monte carlo simulation; agent based methods, machine learning, evolutionary algorithms, (neural) network modeling; computational aspects of dynamic systems, optimization, optimal control, games, equilibrium modeling; hardware and software developments, modeling languages, interfaces, symbolic processing, distributed and parallel processing

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们