Umar-Farouk Atipaga, Imhotep Alagidede, George Tweneboah

{"title":"论非洲新兴市场和前沿市场股票收益与汇率的关联性","authors":"Umar-Farouk Atipaga, Imhotep Alagidede, George Tweneboah","doi":"10.1111/ecno.12249","DOIUrl":null,"url":null,"abstract":"<p>The effect of currency volatility on investments in Africa continues to dominate the headlines, especially in the recent period of global crisis and heightened geopolitical tensions. This paper tackles the dynamic relationship between stock returns and exchange rates in nine emerging and frontier African markets. The study departs from the usual VAR and GARCH models and employs a tool that accounts for time–frequency co-movements and lead/lag relationships between exchange rates and stock returns in Africa. The bivariate wavelet technique applied to daily data from 1 April 2013 to 31 March 2022 established a profound negative co-movement between stock returns and exchange rates, especially in the medium to long-term frequencies. With exchange rates dominantly playing a leading role, it presents a case for policy consideration toward currency stability. We employed the partial wavelet approach to determine how stock returns and exchange rates related during the peak period of the COVID-19 pandemic and found negative co-movements within the short-term frequency, revealing that investors preferred the short-term horizon in times of crisis. However, when the covariate (COVID-19) was controlled or suppressed, we discovered the health pandemic failed to drive both stock returns and exchange rates.</p>","PeriodicalId":44298,"journal":{"name":"Economic Notes","volume":"53 3","pages":""},"PeriodicalIF":1.4000,"publicationDate":"2024-09-18","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1111/ecno.12249","citationCount":"0","resultStr":"{\"title\":\"On the connectedness of stock returns and exchange rates in emerging and frontier markets in Africa\",\"authors\":\"Umar-Farouk Atipaga, Imhotep Alagidede, George Tweneboah\",\"doi\":\"10.1111/ecno.12249\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>The effect of currency volatility on investments in Africa continues to dominate the headlines, especially in the recent period of global crisis and heightened geopolitical tensions. This paper tackles the dynamic relationship between stock returns and exchange rates in nine emerging and frontier African markets. The study departs from the usual VAR and GARCH models and employs a tool that accounts for time–frequency co-movements and lead/lag relationships between exchange rates and stock returns in Africa. The bivariate wavelet technique applied to daily data from 1 April 2013 to 31 March 2022 established a profound negative co-movement between stock returns and exchange rates, especially in the medium to long-term frequencies. With exchange rates dominantly playing a leading role, it presents a case for policy consideration toward currency stability. We employed the partial wavelet approach to determine how stock returns and exchange rates related during the peak period of the COVID-19 pandemic and found negative co-movements within the short-term frequency, revealing that investors preferred the short-term horizon in times of crisis. However, when the covariate (COVID-19) was controlled or suppressed, we discovered the health pandemic failed to drive both stock returns and exchange rates.</p>\",\"PeriodicalId\":44298,\"journal\":{\"name\":\"Economic Notes\",\"volume\":\"53 3\",\"pages\":\"\"},\"PeriodicalIF\":1.4000,\"publicationDate\":\"2024-09-18\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://onlinelibrary.wiley.com/doi/epdf/10.1111/ecno.12249\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Economic Notes\",\"FirstCategoryId\":\"1085\",\"ListUrlMain\":\"https://onlinelibrary.wiley.com/doi/10.1111/ecno.12249\",\"RegionNum\":0,\"RegionCategory\":null,\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q3\",\"JCRName\":\"ECONOMICS\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Economic Notes","FirstCategoryId":"1085","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1111/ecno.12249","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q3","JCRName":"ECONOMICS","Score":null,"Total":0}

On the connectedness of stock returns and exchange rates in emerging and frontier markets in Africa

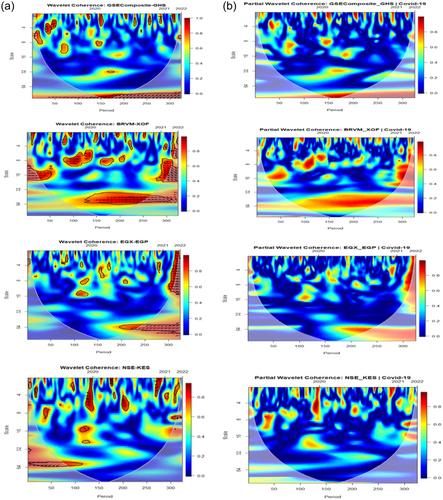

The effect of currency volatility on investments in Africa continues to dominate the headlines, especially in the recent period of global crisis and heightened geopolitical tensions. This paper tackles the dynamic relationship between stock returns and exchange rates in nine emerging and frontier African markets. The study departs from the usual VAR and GARCH models and employs a tool that accounts for time–frequency co-movements and lead/lag relationships between exchange rates and stock returns in Africa. The bivariate wavelet technique applied to daily data from 1 April 2013 to 31 March 2022 established a profound negative co-movement between stock returns and exchange rates, especially in the medium to long-term frequencies. With exchange rates dominantly playing a leading role, it presents a case for policy consideration toward currency stability. We employed the partial wavelet approach to determine how stock returns and exchange rates related during the peak period of the COVID-19 pandemic and found negative co-movements within the short-term frequency, revealing that investors preferred the short-term horizon in times of crisis. However, when the covariate (COVID-19) was controlled or suppressed, we discovered the health pandemic failed to drive both stock returns and exchange rates.

期刊介绍:

With articles that deal with the latest issues in banking, finance and monetary economics internationally, Economic Notes is an essential resource for anyone in the industry, helping you keep abreast of the latest developments in the field. Articles are written by top economists and executives working in financial institutions, firms and the public sector.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们