{"title":"改进机器学习股票交易系统:一种 N 期波动标签和实例选择技术","authors":"Young Hun Song, Myeongseok Park, Jaeyun Kim","doi":"10.1155/2024/5036389","DOIUrl":null,"url":null,"abstract":"<div>\n <p>Financial technology is crucial for the sustainable development of financial systems. Algorithmic trading, a key area in financial technology, involves automated trading based on predefined rules. However, investors cannot manually analyze all market patterns and establish rules, necessitating the development of supervised learning trading systems that can discover market patterns using machine or deep learning techniques. Many studies on supervised learning trading systems rely on up–down labeling based on price differences, which overlooks the issues of nonstationarity, complexity, and noise in stock data. Therefore, this study proposes an N-period volatility trading system that addresses the limitations of up–down labeling systems. The N-period volatility trading system measures price volatility to address uncertainty and enables the construction of a stable, long-term trading system. Additionally, an instance-selection technique is utilized to address the limitations of stock data, including noise, nonlinearity, and complexity, while effectively reducing the data size. The effectiveness of the proposed model is evaluated through trading simulations of stocks comprising the NASDAQ 100 index and compared with up–down labeling trading systems. The experimental results demonstrate that the proposed N-period volatility trading system exhibits higher stability and profitability than other trading systems.</p>\n </div>","PeriodicalId":50653,"journal":{"name":"Complexity","volume":"2024 1","pages":""},"PeriodicalIF":1.7000,"publicationDate":"2024-10-22","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1155/2024/5036389","citationCount":"0","resultStr":"{\"title\":\"Improving the Machine Learning Stock Trading System: An N-Period Volatility Labeling and Instance Selection Technique\",\"authors\":\"Young Hun Song, Myeongseok Park, Jaeyun Kim\",\"doi\":\"10.1155/2024/5036389\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<div>\\n <p>Financial technology is crucial for the sustainable development of financial systems. Algorithmic trading, a key area in financial technology, involves automated trading based on predefined rules. However, investors cannot manually analyze all market patterns and establish rules, necessitating the development of supervised learning trading systems that can discover market patterns using machine or deep learning techniques. Many studies on supervised learning trading systems rely on up–down labeling based on price differences, which overlooks the issues of nonstationarity, complexity, and noise in stock data. Therefore, this study proposes an N-period volatility trading system that addresses the limitations of up–down labeling systems. The N-period volatility trading system measures price volatility to address uncertainty and enables the construction of a stable, long-term trading system. Additionally, an instance-selection technique is utilized to address the limitations of stock data, including noise, nonlinearity, and complexity, while effectively reducing the data size. The effectiveness of the proposed model is evaluated through trading simulations of stocks comprising the NASDAQ 100 index and compared with up–down labeling trading systems. The experimental results demonstrate that the proposed N-period volatility trading system exhibits higher stability and profitability than other trading systems.</p>\\n </div>\",\"PeriodicalId\":50653,\"journal\":{\"name\":\"Complexity\",\"volume\":\"2024 1\",\"pages\":\"\"},\"PeriodicalIF\":1.7000,\"publicationDate\":\"2024-10-22\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://onlinelibrary.wiley.com/doi/epdf/10.1155/2024/5036389\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Complexity\",\"FirstCategoryId\":\"5\",\"ListUrlMain\":\"https://onlinelibrary.wiley.com/doi/10.1155/2024/5036389\",\"RegionNum\":4,\"RegionCategory\":\"工程技术\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q2\",\"JCRName\":\"MATHEMATICS, INTERDISCIPLINARY APPLICATIONS\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Complexity","FirstCategoryId":"5","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1155/2024/5036389","RegionNum":4,"RegionCategory":"工程技术","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q2","JCRName":"MATHEMATICS, INTERDISCIPLINARY APPLICATIONS","Score":null,"Total":0}

引用次数: 0

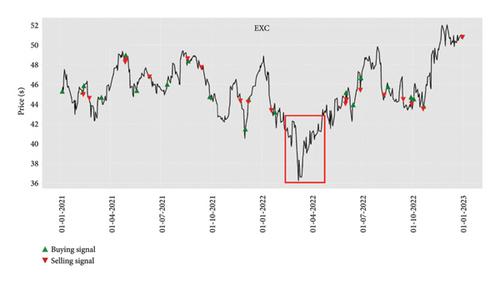

摘要

金融技术对金融体系的可持续发展至关重要。算法交易是金融技术的一个关键领域,涉及基于预定义规则的自动交易。然而,投资者无法手动分析所有市场模式并建立规则,因此有必要开发监督学习交易系统,利用机器或深度学习技术发现市场模式。许多关于监督学习交易系统的研究都依赖于基于价格差异的涨跌标签,这忽略了股票数据的非平稳性、复杂性和噪声等问题。因此,本研究提出了一种 N 期波动率交易系统,以解决上下标注系统的局限性。N 期波动率交易系统通过测量价格波动来解决不确定性问题,从而构建稳定的长期交易系统。此外,还利用实例选择技术来解决股票数据的局限性,包括噪声、非线性和复杂性,同时有效减少数据量。通过对纳斯达克 100 指数中的股票进行模拟交易,评估了所提模型的有效性,并与涨跌标签交易系统进行了比较。实验结果表明,与其他交易系统相比,建议的 N 期波动率交易系统表现出更高的稳定性和盈利能力。

Improving the Machine Learning Stock Trading System: An N-Period Volatility Labeling and Instance Selection Technique

Financial technology is crucial for the sustainable development of financial systems. Algorithmic trading, a key area in financial technology, involves automated trading based on predefined rules. However, investors cannot manually analyze all market patterns and establish rules, necessitating the development of supervised learning trading systems that can discover market patterns using machine or deep learning techniques. Many studies on supervised learning trading systems rely on up–down labeling based on price differences, which overlooks the issues of nonstationarity, complexity, and noise in stock data. Therefore, this study proposes an N-period volatility trading system that addresses the limitations of up–down labeling systems. The N-period volatility trading system measures price volatility to address uncertainty and enables the construction of a stable, long-term trading system. Additionally, an instance-selection technique is utilized to address the limitations of stock data, including noise, nonlinearity, and complexity, while effectively reducing the data size. The effectiveness of the proposed model is evaluated through trading simulations of stocks comprising the NASDAQ 100 index and compared with up–down labeling trading systems. The experimental results demonstrate that the proposed N-period volatility trading system exhibits higher stability and profitability than other trading systems.

期刊介绍:

Complexity is a cross-disciplinary journal focusing on the rapidly expanding science of complex adaptive systems. The purpose of the journal is to advance the science of complexity. Articles may deal with such methodological themes as chaos, genetic algorithms, cellular automata, neural networks, and evolutionary game theory. Papers treating applications in any area of natural science or human endeavor are welcome, and especially encouraged are papers integrating conceptual themes and applications that cross traditional disciplinary boundaries. Complexity is not meant to serve as a forum for speculation and vague analogies between words like “chaos,” “self-organization,” and “emergence” that are often used in completely different ways in science and in daily life.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们