Federico P. Cortese, Fulvia Pennoni, Francesco Bartolucci

{"title":"多元时间转换 Student-t Copula 模型的最大似然估计","authors":"Federico P. Cortese, Fulvia Pennoni, Francesco Bartolucci","doi":"10.1111/insr.12562","DOIUrl":null,"url":null,"abstract":"<p>We propose a multivariate regime switching model based on a Student-\n<span></span><math>\n <mi>t</mi></math> copula function with parameters controlling the strength of correlation between variables and that are governed by a latent Markov process. To estimate model parameters by maximum likelihood, we consider a two-step procedure carried out through the Expectation–Maximisation algorithm. To address the main computational burden related to the estimation of the matrix of dependence parameters and the number of degrees of freedom of the Student-\n<span></span><math>\n <mi>t</mi></math> copula, we show a novel use of the Lagrange multipliers, which simplifies the estimation process. The simulation study shows that the estimators have good finite sample properties and the estimation procedure is computationally efficient. An application concerning log-returns of five cryptocurrencies shows that the model permits identifying bull and bear market periods based on the intensity of the correlations between crypto assets.</p>","PeriodicalId":14479,"journal":{"name":"International Statistical Review","volume":"92 3","pages":"327-354"},"PeriodicalIF":1.9000,"publicationDate":"2024-02-26","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1111/insr.12562","citationCount":"0","resultStr":"{\"title\":\"Maximum Likelihood Estimation of Multivariate Regime Switching Student-t Copula Models\",\"authors\":\"Federico P. Cortese, Fulvia Pennoni, Francesco Bartolucci\",\"doi\":\"10.1111/insr.12562\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>We propose a multivariate regime switching model based on a Student-\\n<span></span><math>\\n <mi>t</mi></math> copula function with parameters controlling the strength of correlation between variables and that are governed by a latent Markov process. To estimate model parameters by maximum likelihood, we consider a two-step procedure carried out through the Expectation–Maximisation algorithm. To address the main computational burden related to the estimation of the matrix of dependence parameters and the number of degrees of freedom of the Student-\\n<span></span><math>\\n <mi>t</mi></math> copula, we show a novel use of the Lagrange multipliers, which simplifies the estimation process. The simulation study shows that the estimators have good finite sample properties and the estimation procedure is computationally efficient. An application concerning log-returns of five cryptocurrencies shows that the model permits identifying bull and bear market periods based on the intensity of the correlations between crypto assets.</p>\",\"PeriodicalId\":14479,\"journal\":{\"name\":\"International Statistical Review\",\"volume\":\"92 3\",\"pages\":\"327-354\"},\"PeriodicalIF\":1.9000,\"publicationDate\":\"2024-02-26\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://onlinelibrary.wiley.com/doi/epdf/10.1111/insr.12562\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"International Statistical Review\",\"FirstCategoryId\":\"100\",\"ListUrlMain\":\"https://onlinelibrary.wiley.com/doi/10.1111/insr.12562\",\"RegionNum\":3,\"RegionCategory\":\"数学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q1\",\"JCRName\":\"STATISTICS & PROBABILITY\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"International Statistical Review","FirstCategoryId":"100","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1111/insr.12562","RegionNum":3,"RegionCategory":"数学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q1","JCRName":"STATISTICS & PROBABILITY","Score":null,"Total":0}

引用次数: 0

摘要

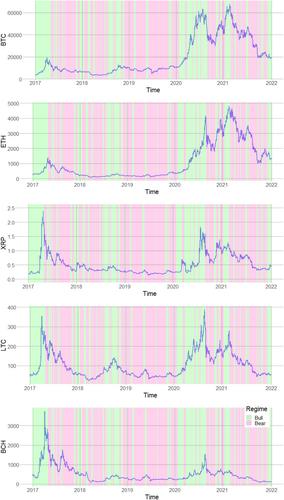

我们提出了一种基于 Student- t copula 函数的多变量制度转换模型,其参数控制着变量之间的相关性强度,并受潜在马尔可夫过程的支配。为了用最大似然法估计模型参数,我们考虑通过期望最大化算法分两步进行。为了解决与估计依赖性参数矩阵和 Student- t 协程自由度数相关的主要计算负担,我们展示了拉格朗日乘数的一种新用法,它简化了估计过程。模拟研究表明,估计器具有良好的有限样本特性,估计过程的计算效率也很高。有关五种加密货币对数收益率的应用表明,该模型可以根据加密资产之间的相关性强度来识别牛市和熊市时期。

Maximum Likelihood Estimation of Multivariate Regime Switching Student-t Copula Models

We propose a multivariate regime switching model based on a Student-

copula function with parameters controlling the strength of correlation between variables and that are governed by a latent Markov process. To estimate model parameters by maximum likelihood, we consider a two-step procedure carried out through the Expectation–Maximisation algorithm. To address the main computational burden related to the estimation of the matrix of dependence parameters and the number of degrees of freedom of the Student-

copula, we show a novel use of the Lagrange multipliers, which simplifies the estimation process. The simulation study shows that the estimators have good finite sample properties and the estimation procedure is computationally efficient. An application concerning log-returns of five cryptocurrencies shows that the model permits identifying bull and bear market periods based on the intensity of the correlations between crypto assets.

期刊介绍:

International Statistical Review is the flagship journal of the International Statistical Institute (ISI) and of its family of Associations. It publishes papers of broad and general interest in statistics and probability. The term Review is to be interpreted broadly. The types of papers that are suitable for publication include (but are not limited to) the following: reviews/surveys of significant developments in theory, methodology, statistical computing and graphics, statistical education, and application areas; tutorials on important topics; expository papers on emerging areas of research or application; papers describing new developments and/or challenges in relevant areas; papers addressing foundational issues; papers on the history of statistics and probability; white papers on topics of importance to the profession or society; and historical assessment of seminal papers in the field and their impact.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们