{"title":"不同年龄组在经济压力下的财务行为:20 年间的预测因素和变化。","authors":"G Silinskas, M Ranta, T-A Wilska","doi":"10.1007/s10603-021-09480-6","DOIUrl":null,"url":null,"abstract":"<p><p>The present study examined the multiple micro- and macro-level factors that affect individuals' financial behaviour under economic strain. The following sociodemographic and economic factors that predict financial behaviour were analysed: age group, year of data gathering, and attitudes towards consumption (economical, deprived, and hedonistic). Subjective financial situations and demographic characteristics were controlled for. Finnish time series data that consisted of five cross-sectional nationally representative surveys were used (<i>n</i> = 10 043). The analyses revealed four types of financial behaviour: cutting expenses, borrowing, increasing income, and gambling. Young adults aged 18-25 reported the lowest frequency of borrowing and gambling and the highest frequency of increasing income (together with young adults aged 26-35). Participants aged 66-75 scored the lowest in cutting expenses and increasing income in comparison to all other age groups. Financial behaviour under economic strain in 2019 can be characterized by lower instances of borrowing than in 2004 and 2009 and higher frequencies in increasing income in comparison to all other years of data gathering. Finally, strong attitudes towards saving were related to lower frequency of borrowing and gambling, whereas stronger hedonistic attitudes were related to lower frequency of cutting expenses and more frequent borrowing. The research results provide tools for consumer policy, consumer education, and consumer regulation.</p>","PeriodicalId":47436,"journal":{"name":"JOURNAL OF CONSUMER POLICY","volume":"44 2","pages":"235-257"},"PeriodicalIF":1.6000,"publicationDate":"2021-01-01","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://www.ncbi.nlm.nih.gov/pmc/articles/PMC7947154/pdf/","citationCount":"0","resultStr":"{\"title\":\"Financial Behaviour Under Economic Strain in Different Age Groups: Predictors and Change Across 20 Years.\",\"authors\":\"G Silinskas, M Ranta, T-A Wilska\",\"doi\":\"10.1007/s10603-021-09480-6\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p><p>The present study examined the multiple micro- and macro-level factors that affect individuals' financial behaviour under economic strain. The following sociodemographic and economic factors that predict financial behaviour were analysed: age group, year of data gathering, and attitudes towards consumption (economical, deprived, and hedonistic). Subjective financial situations and demographic characteristics were controlled for. Finnish time series data that consisted of five cross-sectional nationally representative surveys were used (<i>n</i> = 10 043). The analyses revealed four types of financial behaviour: cutting expenses, borrowing, increasing income, and gambling. Young adults aged 18-25 reported the lowest frequency of borrowing and gambling and the highest frequency of increasing income (together with young adults aged 26-35). Participants aged 66-75 scored the lowest in cutting expenses and increasing income in comparison to all other age groups. Financial behaviour under economic strain in 2019 can be characterized by lower instances of borrowing than in 2004 and 2009 and higher frequencies in increasing income in comparison to all other years of data gathering. Finally, strong attitudes towards saving were related to lower frequency of borrowing and gambling, whereas stronger hedonistic attitudes were related to lower frequency of cutting expenses and more frequent borrowing. The research results provide tools for consumer policy, consumer education, and consumer regulation.</p>\",\"PeriodicalId\":47436,\"journal\":{\"name\":\"JOURNAL OF CONSUMER POLICY\",\"volume\":\"44 2\",\"pages\":\"235-257\"},\"PeriodicalIF\":1.6000,\"publicationDate\":\"2021-01-01\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://www.ncbi.nlm.nih.gov/pmc/articles/PMC7947154/pdf/\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"JOURNAL OF CONSUMER POLICY\",\"FirstCategoryId\":\"1085\",\"ListUrlMain\":\"https://doi.org/10.1007/s10603-021-09480-6\",\"RegionNum\":0,\"RegionCategory\":null,\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"2021/3/11 0:00:00\",\"PubModel\":\"Epub\",\"JCR\":\"Q3\",\"JCRName\":\"BUSINESS\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"JOURNAL OF CONSUMER POLICY","FirstCategoryId":"1085","ListUrlMain":"https://doi.org/10.1007/s10603-021-09480-6","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"2021/3/11 0:00:00","PubModel":"Epub","JCR":"Q3","JCRName":"BUSINESS","Score":null,"Total":0}

Financial Behaviour Under Economic Strain in Different Age Groups: Predictors and Change Across 20 Years.

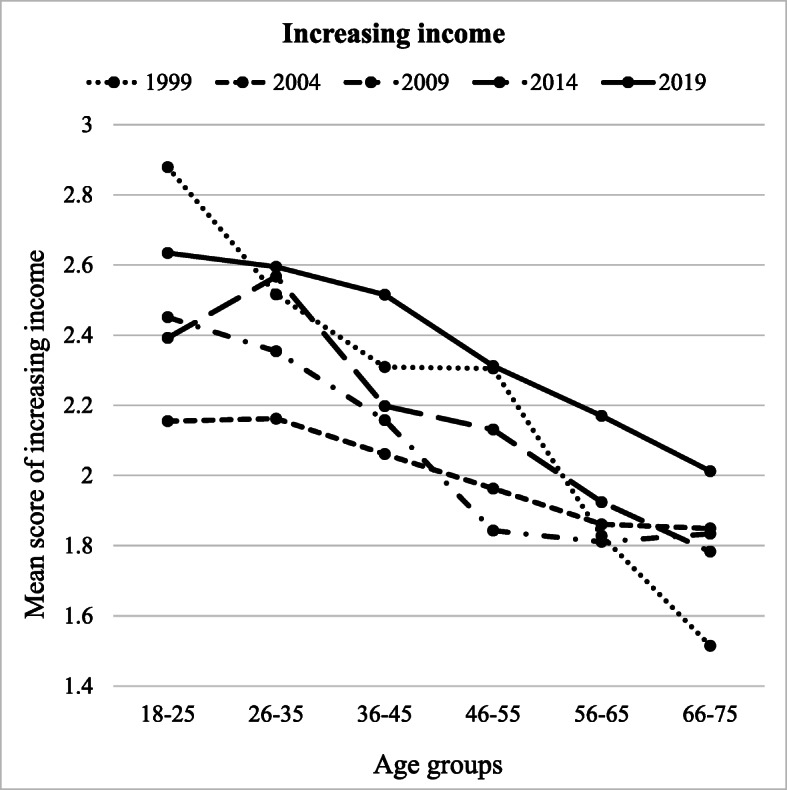

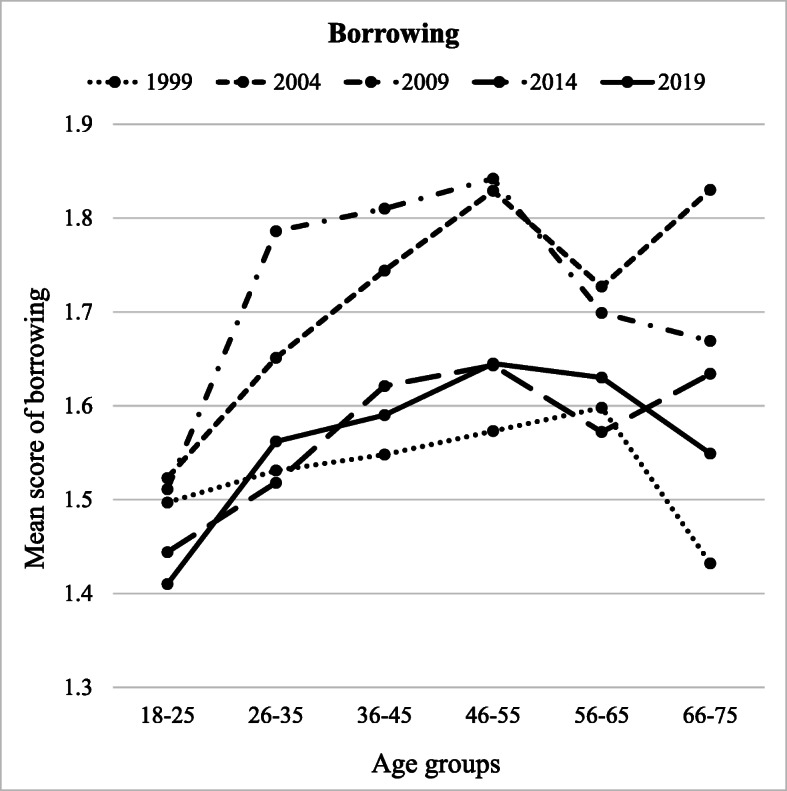

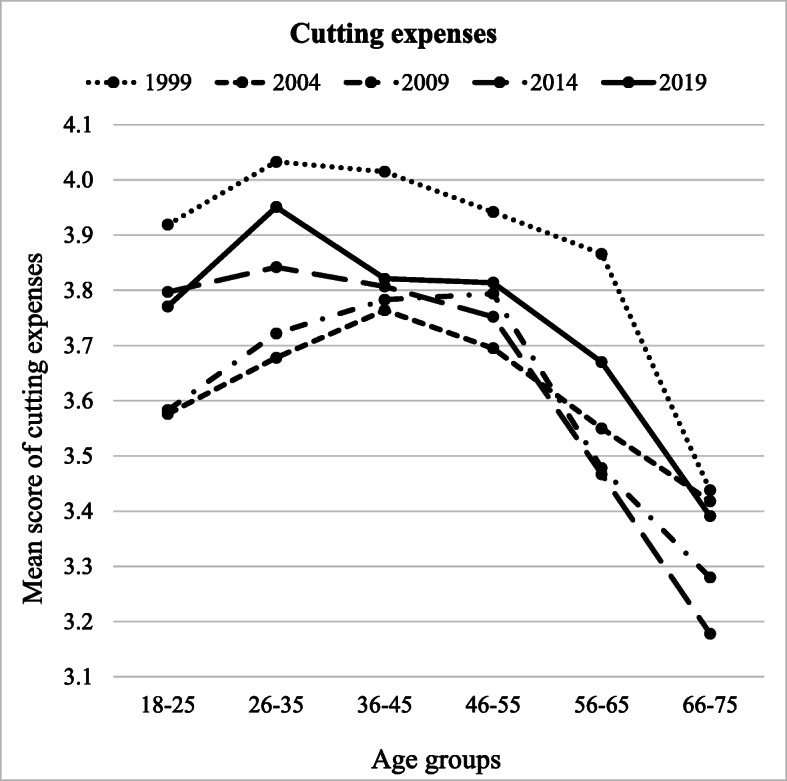

The present study examined the multiple micro- and macro-level factors that affect individuals' financial behaviour under economic strain. The following sociodemographic and economic factors that predict financial behaviour were analysed: age group, year of data gathering, and attitudes towards consumption (economical, deprived, and hedonistic). Subjective financial situations and demographic characteristics were controlled for. Finnish time series data that consisted of five cross-sectional nationally representative surveys were used (n = 10 043). The analyses revealed four types of financial behaviour: cutting expenses, borrowing, increasing income, and gambling. Young adults aged 18-25 reported the lowest frequency of borrowing and gambling and the highest frequency of increasing income (together with young adults aged 26-35). Participants aged 66-75 scored the lowest in cutting expenses and increasing income in comparison to all other age groups. Financial behaviour under economic strain in 2019 can be characterized by lower instances of borrowing than in 2004 and 2009 and higher frequencies in increasing income in comparison to all other years of data gathering. Finally, strong attitudes towards saving were related to lower frequency of borrowing and gambling, whereas stronger hedonistic attitudes were related to lower frequency of cutting expenses and more frequent borrowing. The research results provide tools for consumer policy, consumer education, and consumer regulation.

期刊介绍:

The Journal of Consumer Policy is a refereed, international journal which encompasses a broad range of issues concerned with consumer affairs. It looks at the consumer''s dependence on existing social and economic structures, helps to define the consumer''s interest, and discusses the ways in which consumer welfare can be fostered - or restrained - through actions and policies of consumers, industry, organizations, government, educational institutions, and the mass media.

The Journal of Consumer Policy publishes theoretical and empirical research on consumer and producer conduct, emphasizing the implications for consumers and increasing communication between the parties in the marketplace.

Articles cover consumer issues in law, economics, and behavioural sciences. Current areas of topical interest include the impact of new information technologies, the economics of information, the consequences of regulation or deregulation of markets, problems related to an increasing internationalization of trade and marketing practices, consumers in less affluent societies, the efficacy of economic cooperation, consumers and the environment, problems with products and services provided by the public sector, the setting of priorities by consumer organizations and agencies, gender issues, product safety and product liability, and the interaction between consumption and associated forms of behaviour such as work and leisure.

The Journal of Consumer Policy reports regularly on developments in legal policy with a bearing on consumer issues. It covers the integration of consumer law in the European Union and other transnational communities and analyzes trends in the application and implementation of consumer legislation through administrative agencies, courts, trade associations, and consumer organizations. It also considers the impact of consumer legislation on the supply side and discusses comparative legal approaches to issues of cons umer policy in different parts of the world.

The Journal of Consumer Policy informs readers about a broad array of consumer policy issues by publishing regularly both extended book reviews and brief, non-evaluative book notes on new publications in the field.

Officially cited as: J Consum Policy

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们