{"title":"合作合规对企业税收风险、税收风险管理和合规成本的影响。","authors":"Eva Eberhartinger, Maximilian Zieser","doi":"10.1007/s41471-021-00108-6","DOIUrl":null,"url":null,"abstract":"<p><p>In cooperative compliance programs, firms and tax administrations agree on cooperation instead of confrontation. Firms provide full transparency and advanced tax control frameworks. Tax administrations, in turn, offer certainty as to the tax treatment of complex transactions. In this study, we test how firms' perceptions of tax risk, the quality of tax risk management, and compliance costs are related to cooperative compliance. To our knowledge, this is the first study that attempts to analyze both reasons for and consequences of participation in cooperative compliance programs. We examine the Austrian cooperative compliance pilot project known as horizontal monitoring that was aimed at large businesses and launched in 2011. We use survey data from representatives of firms participating in the pilot project and a sample of comparable firms under a traditional ex-post audit regime. We conduct group comparisons to test differences between these groups, as well as mediation analyses to shed light on more complex relationships between variables. Results show that horizontal monitoring firms perceive a significantly higher increase in tax certainty, which is associated with significant relative decreases in tax risk and compliance costs. Furthermore, while the quality of tax risk management upon entering the pilot project appears significantly higher for horizontal monitoring firms, they do not report greater improvement in tax risk management compared to the control group. These results are relevant for the development of cooperative compliance programs and the decision to participate in them.</p>","PeriodicalId":74759,"journal":{"name":"Schmalenbachs Zeitschrift fur betriebswirtschaftliche Forschung = Schmalenbach journal of business research","volume":"73 1","pages":"125-178"},"PeriodicalIF":0.0000,"publicationDate":"2021-01-01","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://sci-hub-pdf.com/10.1007/s41471-021-00108-6","citationCount":"10","resultStr":"{\"title\":\"The Effects of Cooperative Compliance on Firms' Tax Risk, Tax Risk Management and Compliance Costs.\",\"authors\":\"Eva Eberhartinger, Maximilian Zieser\",\"doi\":\"10.1007/s41471-021-00108-6\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p><p>In cooperative compliance programs, firms and tax administrations agree on cooperation instead of confrontation. Firms provide full transparency and advanced tax control frameworks. Tax administrations, in turn, offer certainty as to the tax treatment of complex transactions. In this study, we test how firms' perceptions of tax risk, the quality of tax risk management, and compliance costs are related to cooperative compliance. To our knowledge, this is the first study that attempts to analyze both reasons for and consequences of participation in cooperative compliance programs. We examine the Austrian cooperative compliance pilot project known as horizontal monitoring that was aimed at large businesses and launched in 2011. We use survey data from representatives of firms participating in the pilot project and a sample of comparable firms under a traditional ex-post audit regime. We conduct group comparisons to test differences between these groups, as well as mediation analyses to shed light on more complex relationships between variables. Results show that horizontal monitoring firms perceive a significantly higher increase in tax certainty, which is associated with significant relative decreases in tax risk and compliance costs. Furthermore, while the quality of tax risk management upon entering the pilot project appears significantly higher for horizontal monitoring firms, they do not report greater improvement in tax risk management compared to the control group. These results are relevant for the development of cooperative compliance programs and the decision to participate in them.</p>\",\"PeriodicalId\":74759,\"journal\":{\"name\":\"Schmalenbachs Zeitschrift fur betriebswirtschaftliche Forschung = Schmalenbach journal of business research\",\"volume\":\"73 1\",\"pages\":\"125-178\"},\"PeriodicalIF\":0.0000,\"publicationDate\":\"2021-01-01\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://sci-hub-pdf.com/10.1007/s41471-021-00108-6\",\"citationCount\":\"10\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Schmalenbachs Zeitschrift fur betriebswirtschaftliche Forschung = Schmalenbach journal of business research\",\"FirstCategoryId\":\"1085\",\"ListUrlMain\":\"https://doi.org/10.1007/s41471-021-00108-6\",\"RegionNum\":0,\"RegionCategory\":null,\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"2021/3/23 0:00:00\",\"PubModel\":\"Epub\",\"JCR\":\"\",\"JCRName\":\"\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Schmalenbachs Zeitschrift fur betriebswirtschaftliche Forschung = Schmalenbach journal of business research","FirstCategoryId":"1085","ListUrlMain":"https://doi.org/10.1007/s41471-021-00108-6","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"2021/3/23 0:00:00","PubModel":"Epub","JCR":"","JCRName":"","Score":null,"Total":0}

The Effects of Cooperative Compliance on Firms' Tax Risk, Tax Risk Management and Compliance Costs.

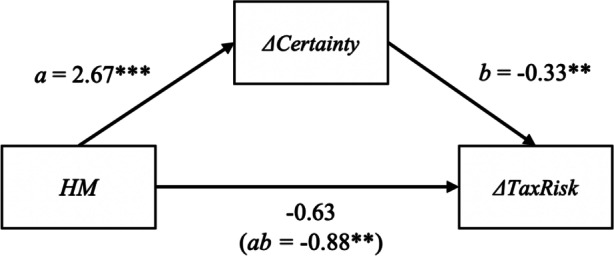

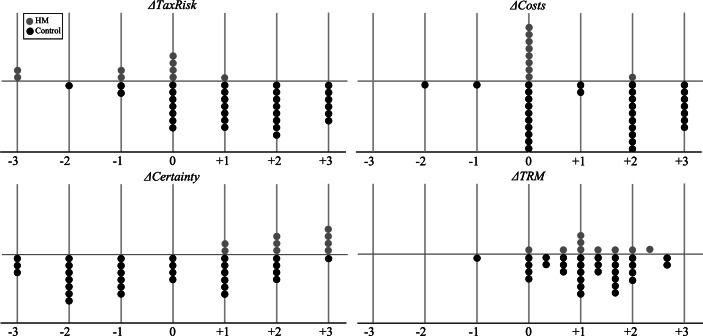

In cooperative compliance programs, firms and tax administrations agree on cooperation instead of confrontation. Firms provide full transparency and advanced tax control frameworks. Tax administrations, in turn, offer certainty as to the tax treatment of complex transactions. In this study, we test how firms' perceptions of tax risk, the quality of tax risk management, and compliance costs are related to cooperative compliance. To our knowledge, this is the first study that attempts to analyze both reasons for and consequences of participation in cooperative compliance programs. We examine the Austrian cooperative compliance pilot project known as horizontal monitoring that was aimed at large businesses and launched in 2011. We use survey data from representatives of firms participating in the pilot project and a sample of comparable firms under a traditional ex-post audit regime. We conduct group comparisons to test differences between these groups, as well as mediation analyses to shed light on more complex relationships between variables. Results show that horizontal monitoring firms perceive a significantly higher increase in tax certainty, which is associated with significant relative decreases in tax risk and compliance costs. Furthermore, while the quality of tax risk management upon entering the pilot project appears significantly higher for horizontal monitoring firms, they do not report greater improvement in tax risk management compared to the control group. These results are relevant for the development of cooperative compliance programs and the decision to participate in them.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们