{"title":"中国原油期货与国际石油市场之间的时变关联性:回报与波动溢出分析》。","authors":"Jiasha Fu, Hui Qiao","doi":"10.1007/s12076-021-00288-z","DOIUrl":null,"url":null,"abstract":"<p><p>This paper examines the relationship between world crude oil markets following the introduction of Shanghai crude oil futures from the perspective of network connectedness based on the vector autoregressive model. The connectedness measurement method proposed by Diebold and Yilmaz (Econ J 119(534):158-171, 2009, Int J Forecast 28(1):57-66, 2012. 10.1016/j.ijforecast.2011.02.006, J Econom 182(1):119-134, 2014. 10.1016/j.jeconom.2014.04.012) is adopted to study a time-varying interdependence relationship. The empirical results show that the world crude oil markets exhibit a high degree of integration from both returns and volatility; however, the direction and magnitude contributed by each market varies significantly. Specifically, the West Texas Intermediate futures and Brent spot and futures markets were found to have the highest contributions to the world oil market over the entire sample period and take leading roles, whereas Dubai futures market was found to be the most important receiver, and has received the most spillover from other markets and passed it throughout the system. Shanghai crude oil futures is not yet highly connected with other markets. Moreover, heterogeneous changes in the direction, intensity, and persistence of the spillover were observed across markets after the outbreak of the COVID-19 pandemic in 2020. This study reveals the integration level of Shanghai crude oil futures and the dynamics of linkages between regional crude oil markets, which is of great significance for market participants, policymakers, and future researchers.</p><p><strong>Supplementary information: </strong>The online version contains supplementary material available at 10.1007/s12076-021-00288-z.</p>","PeriodicalId":44710,"journal":{"name":"Letters in Spatial and Resource Sciences","volume":"15 3","pages":"341-376"},"PeriodicalIF":1.1000,"publicationDate":"2022-01-01","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://www.ncbi.nlm.nih.gov/pmc/articles/PMC8561088/pdf/","citationCount":"0","resultStr":"{\"title\":\"The Time-Varying Connectedness Between China's Crude Oil Futures and International Oil Markets: A Return and Volatility Spillover Analysis.\",\"authors\":\"Jiasha Fu, Hui Qiao\",\"doi\":\"10.1007/s12076-021-00288-z\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p><p>This paper examines the relationship between world crude oil markets following the introduction of Shanghai crude oil futures from the perspective of network connectedness based on the vector autoregressive model. The connectedness measurement method proposed by Diebold and Yilmaz (Econ J 119(534):158-171, 2009, Int J Forecast 28(1):57-66, 2012. 10.1016/j.ijforecast.2011.02.006, J Econom 182(1):119-134, 2014. 10.1016/j.jeconom.2014.04.012) is adopted to study a time-varying interdependence relationship. The empirical results show that the world crude oil markets exhibit a high degree of integration from both returns and volatility; however, the direction and magnitude contributed by each market varies significantly. Specifically, the West Texas Intermediate futures and Brent spot and futures markets were found to have the highest contributions to the world oil market over the entire sample period and take leading roles, whereas Dubai futures market was found to be the most important receiver, and has received the most spillover from other markets and passed it throughout the system. Shanghai crude oil futures is not yet highly connected with other markets. Moreover, heterogeneous changes in the direction, intensity, and persistence of the spillover were observed across markets after the outbreak of the COVID-19 pandemic in 2020. This study reveals the integration level of Shanghai crude oil futures and the dynamics of linkages between regional crude oil markets, which is of great significance for market participants, policymakers, and future researchers.</p><p><strong>Supplementary information: </strong>The online version contains supplementary material available at 10.1007/s12076-021-00288-z.</p>\",\"PeriodicalId\":44710,\"journal\":{\"name\":\"Letters in Spatial and Resource Sciences\",\"volume\":\"15 3\",\"pages\":\"341-376\"},\"PeriodicalIF\":1.1000,\"publicationDate\":\"2022-01-01\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://www.ncbi.nlm.nih.gov/pmc/articles/PMC8561088/pdf/\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Letters in Spatial and Resource Sciences\",\"FirstCategoryId\":\"1085\",\"ListUrlMain\":\"https://doi.org/10.1007/s12076-021-00288-z\",\"RegionNum\":0,\"RegionCategory\":null,\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"2021/11/2 0:00:00\",\"PubModel\":\"Epub\",\"JCR\":\"Q2\",\"JCRName\":\"GEOGRAPHY\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Letters in Spatial and Resource Sciences","FirstCategoryId":"1085","ListUrlMain":"https://doi.org/10.1007/s12076-021-00288-z","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"2021/11/2 0:00:00","PubModel":"Epub","JCR":"Q2","JCRName":"GEOGRAPHY","Score":null,"Total":0}

The Time-Varying Connectedness Between China's Crude Oil Futures and International Oil Markets: A Return and Volatility Spillover Analysis.

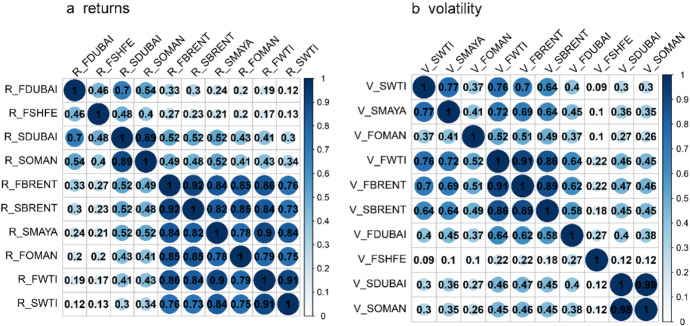

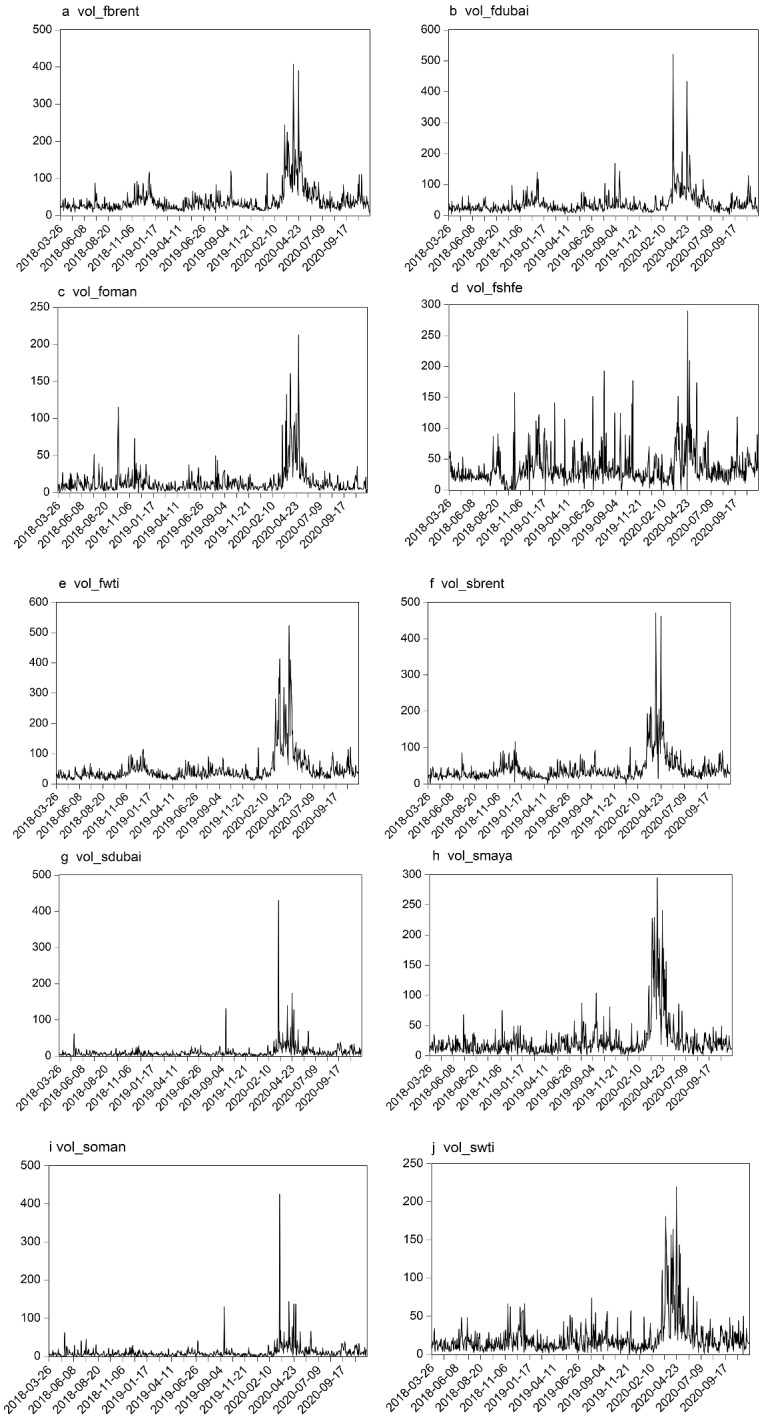

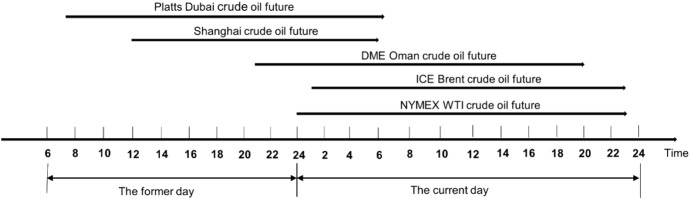

This paper examines the relationship between world crude oil markets following the introduction of Shanghai crude oil futures from the perspective of network connectedness based on the vector autoregressive model. The connectedness measurement method proposed by Diebold and Yilmaz (Econ J 119(534):158-171, 2009, Int J Forecast 28(1):57-66, 2012. 10.1016/j.ijforecast.2011.02.006, J Econom 182(1):119-134, 2014. 10.1016/j.jeconom.2014.04.012) is adopted to study a time-varying interdependence relationship. The empirical results show that the world crude oil markets exhibit a high degree of integration from both returns and volatility; however, the direction and magnitude contributed by each market varies significantly. Specifically, the West Texas Intermediate futures and Brent spot and futures markets were found to have the highest contributions to the world oil market over the entire sample period and take leading roles, whereas Dubai futures market was found to be the most important receiver, and has received the most spillover from other markets and passed it throughout the system. Shanghai crude oil futures is not yet highly connected with other markets. Moreover, heterogeneous changes in the direction, intensity, and persistence of the spillover were observed across markets after the outbreak of the COVID-19 pandemic in 2020. This study reveals the integration level of Shanghai crude oil futures and the dynamics of linkages between regional crude oil markets, which is of great significance for market participants, policymakers, and future researchers.

Supplementary information: The online version contains supplementary material available at 10.1007/s12076-021-00288-z.

期刊介绍:

Letters in Spatial and Resource Sciences (LSRS) publishes high-quality, shorter papers on new theoretical or empirical results and on models and methods in the social sciences that contain a spatial dimension. Coverage includes environmental and resource economics, regional and urban economics, spatial econometrics, regional science, geography, demography, agricultural economics, GIS and city and regional planning. Examples of topics include, but are not limited to, environmental damage, urbanization, resource allocation, spatial-temporal data use, regional economic development and the application of existing and new methodologies.LSRS contributes to the communication of theories and methodologies across disciplinary borders. It offers quick dissemination and easy accessibility of new results. Officially cited as: Lett Spat Resour Sci

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们