{"title":"权益性金融资产的保监呈报是否重要?","authors":"Zeting Zang, Humayun Kabir, Tom Scott","doi":"10.1111/auar.12385","DOIUrl":null,"url":null,"abstract":"<p>One significant change in International Financial Reporting Standard (IFRS) 9 <i>Financial Instruments</i> is how firms’ equity financial assets (EFA) are presented. The default EFA presentation is at fair value through profit or loss (FVTPL); however, IFRS 9 allows irrevocable presentation of fair value through other comprehensive income (FVTOCI). Although FVTOCI is the most common presentation for EFA both before and after IFRS 9, there is a significant increase in the use of FVTPL post IFRS 9 via an improvement in disclosure clarity about presentation location. To assess the impact of EFA presentation, we recalculate profitability ratios assuming different presentation locations and find some evidence of significant differences for financial firms. We also provide descriptive evidence that EFA use and presentation behaviour vary between sectors and firm size quartiles. This study expands the literature on EFA accounting and provides a timely response to IFRS 9 post-implementation review by shedding some light on EFA use and presentation locations under IFRS 9.</p>","PeriodicalId":51552,"journal":{"name":"Australian Accounting Review","volume":"32 4","pages":"427-439"},"PeriodicalIF":3.3000,"publicationDate":"2022-08-31","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1111/auar.12385","citationCount":"1","resultStr":"{\"title\":\"Does OCI Presentation for Equity Financial Assets Matter?\",\"authors\":\"Zeting Zang, Humayun Kabir, Tom Scott\",\"doi\":\"10.1111/auar.12385\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>One significant change in International Financial Reporting Standard (IFRS) 9 <i>Financial Instruments</i> is how firms’ equity financial assets (EFA) are presented. The default EFA presentation is at fair value through profit or loss (FVTPL); however, IFRS 9 allows irrevocable presentation of fair value through other comprehensive income (FVTOCI). Although FVTOCI is the most common presentation for EFA both before and after IFRS 9, there is a significant increase in the use of FVTPL post IFRS 9 via an improvement in disclosure clarity about presentation location. To assess the impact of EFA presentation, we recalculate profitability ratios assuming different presentation locations and find some evidence of significant differences for financial firms. We also provide descriptive evidence that EFA use and presentation behaviour vary between sectors and firm size quartiles. This study expands the literature on EFA accounting and provides a timely response to IFRS 9 post-implementation review by shedding some light on EFA use and presentation locations under IFRS 9.</p>\",\"PeriodicalId\":51552,\"journal\":{\"name\":\"Australian Accounting Review\",\"volume\":\"32 4\",\"pages\":\"427-439\"},\"PeriodicalIF\":3.3000,\"publicationDate\":\"2022-08-31\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://onlinelibrary.wiley.com/doi/epdf/10.1111/auar.12385\",\"citationCount\":\"1\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Australian Accounting Review\",\"FirstCategoryId\":\"91\",\"ListUrlMain\":\"https://onlinelibrary.wiley.com/doi/10.1111/auar.12385\",\"RegionNum\":3,\"RegionCategory\":\"管理学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q2\",\"JCRName\":\"BUSINESS, FINANCE\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Australian Accounting Review","FirstCategoryId":"91","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1111/auar.12385","RegionNum":3,"RegionCategory":"管理学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q2","JCRName":"BUSINESS, FINANCE","Score":null,"Total":0}

Does OCI Presentation for Equity Financial Assets Matter?

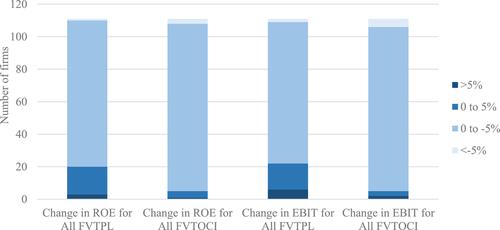

One significant change in International Financial Reporting Standard (IFRS) 9 Financial Instruments is how firms’ equity financial assets (EFA) are presented. The default EFA presentation is at fair value through profit or loss (FVTPL); however, IFRS 9 allows irrevocable presentation of fair value through other comprehensive income (FVTOCI). Although FVTOCI is the most common presentation for EFA both before and after IFRS 9, there is a significant increase in the use of FVTPL post IFRS 9 via an improvement in disclosure clarity about presentation location. To assess the impact of EFA presentation, we recalculate profitability ratios assuming different presentation locations and find some evidence of significant differences for financial firms. We also provide descriptive evidence that EFA use and presentation behaviour vary between sectors and firm size quartiles. This study expands the literature on EFA accounting and provides a timely response to IFRS 9 post-implementation review by shedding some light on EFA use and presentation locations under IFRS 9.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们