{"title":"内部审计:内部控制审计的影响和质量的案例研究","authors":"Leif Christensen","doi":"10.1111/ijau.12280","DOIUrl":null,"url":null,"abstract":"<p>Traditionally, when companies needed assistance regarding internal controls, they turned to an external auditor (EA). However, now, due to an ongoing tightening of legal requirements and practices regarding the independence of EAs, this assistance has been restricted. As an alternative, companies are increasingly requesting internal audits to deliver this support. Even though internal audit function (IAF) are an important player in internal control, however, there is little academic knowledge about their impact. Based on a single-case study in a large financial institution, this paper explores to what extent and how IAF affect internal controls. Furthermore, it assesses whether IAF add value to the company. The results suggest that the management letter process, including a step-by-step settlement of interactions, leads to a joint problem solving, an acceptance of all IAF's recommendations and a value-adding outcome improving the level of internal controls.</p>","PeriodicalId":47092,"journal":{"name":"International Journal of Auditing","volume":"26 3","pages":"339-353"},"PeriodicalIF":1.4000,"publicationDate":"2022-05-12","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1111/ijau.12280","citationCount":"3","resultStr":"{\"title\":\"Internal audit: A case study of impact and quality of an internal control audit\",\"authors\":\"Leif Christensen\",\"doi\":\"10.1111/ijau.12280\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>Traditionally, when companies needed assistance regarding internal controls, they turned to an external auditor (EA). However, now, due to an ongoing tightening of legal requirements and practices regarding the independence of EAs, this assistance has been restricted. As an alternative, companies are increasingly requesting internal audits to deliver this support. Even though internal audit function (IAF) are an important player in internal control, however, there is little academic knowledge about their impact. Based on a single-case study in a large financial institution, this paper explores to what extent and how IAF affect internal controls. Furthermore, it assesses whether IAF add value to the company. The results suggest that the management letter process, including a step-by-step settlement of interactions, leads to a joint problem solving, an acceptance of all IAF's recommendations and a value-adding outcome improving the level of internal controls.</p>\",\"PeriodicalId\":47092,\"journal\":{\"name\":\"International Journal of Auditing\",\"volume\":\"26 3\",\"pages\":\"339-353\"},\"PeriodicalIF\":1.4000,\"publicationDate\":\"2022-05-12\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://onlinelibrary.wiley.com/doi/epdf/10.1111/ijau.12280\",\"citationCount\":\"3\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"International Journal of Auditing\",\"FirstCategoryId\":\"91\",\"ListUrlMain\":\"https://onlinelibrary.wiley.com/doi/10.1111/ijau.12280\",\"RegionNum\":4,\"RegionCategory\":\"管理学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q2\",\"JCRName\":\"BUSINESS, FINANCE\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"International Journal of Auditing","FirstCategoryId":"91","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1111/ijau.12280","RegionNum":4,"RegionCategory":"管理学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q2","JCRName":"BUSINESS, FINANCE","Score":null,"Total":0}

Internal audit: A case study of impact and quality of an internal control audit

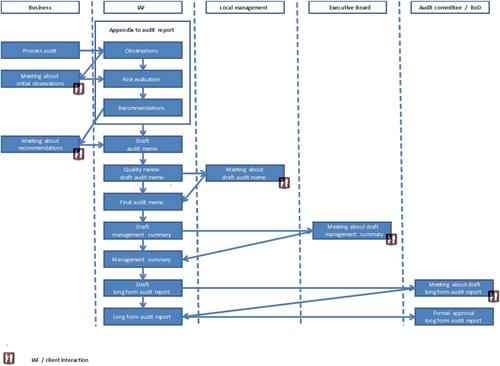

Traditionally, when companies needed assistance regarding internal controls, they turned to an external auditor (EA). However, now, due to an ongoing tightening of legal requirements and practices regarding the independence of EAs, this assistance has been restricted. As an alternative, companies are increasingly requesting internal audits to deliver this support. Even though internal audit function (IAF) are an important player in internal control, however, there is little academic knowledge about their impact. Based on a single-case study in a large financial institution, this paper explores to what extent and how IAF affect internal controls. Furthermore, it assesses whether IAF add value to the company. The results suggest that the management letter process, including a step-by-step settlement of interactions, leads to a joint problem solving, an acceptance of all IAF's recommendations and a value-adding outcome improving the level of internal controls.

期刊介绍:

In addition to communicating the results of original auditing research, the International Journal of Auditing also aims to advance knowledge in auditing by publishing critiques, thought leadership papers and literature reviews on specific aspects of auditing. The journal seeks to publish articles that have international appeal either due to the topic transcending national frontiers or due to the clear potential for readers to apply the results or ideas in their local environments. While articles must be methodologically and theoretically sound, any research orientation is acceptable. This means that papers may have an analytical and statistical, behavioural, economic and financial (including agency), sociological, critical, or historical basis. The editors consider articles for publication which fit into one or more of the following subject categories: • Financial statement audits • Public sector/governmental auditing • Internal auditing • Audit education and methods of teaching auditing (including case studies) • Audit aspects of corporate governance, including audit committees • Audit quality • Audit fees and related issues • Environmental, social and sustainability audits • Audit related ethical issues • Audit regulation • Independence issues • Legal liability and other legal issues • Auditing history • New and emerging audit and assurance issues

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们