{"title":"贝叶斯投资者信念更新速度与市场对收益公告的反应不足","authors":"Yan Han, Xin Cui, Gloria Y. Tian, Peipei Wang","doi":"10.1111/auar.12395","DOIUrl":null,"url":null,"abstract":"<p>Building on the Bayesian Theorem, we propose a multi-period market microstructure model to understand how Bayesian investors underact new information and the duration of market underreaction. Applying the model to post-earnings-announcement drifts, our simulation and regression analyses show that the duration of the post-announcement price adjustment process and the post-announcement drifts can be explained by the new measure of belief updating speed that quantifies the uncertainties faced by Bayesian investors when incorporating new information into prices. Our study highlights the importance of incorporating the belief uncertainties of uninformed investors in explaining market underreaction in the Bayesian framework.</p>","PeriodicalId":51552,"journal":{"name":"Australian Accounting Review","volume":"33 1","pages":"66-85"},"PeriodicalIF":3.1000,"publicationDate":"2023-02-21","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1111/auar.12395","citationCount":"1","resultStr":"{\"title\":\"Bayesian Investor Belief Updating Speed and Market Underreaction to Earnings Announcements\",\"authors\":\"Yan Han, Xin Cui, Gloria Y. Tian, Peipei Wang\",\"doi\":\"10.1111/auar.12395\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>Building on the Bayesian Theorem, we propose a multi-period market microstructure model to understand how Bayesian investors underact new information and the duration of market underreaction. Applying the model to post-earnings-announcement drifts, our simulation and regression analyses show that the duration of the post-announcement price adjustment process and the post-announcement drifts can be explained by the new measure of belief updating speed that quantifies the uncertainties faced by Bayesian investors when incorporating new information into prices. Our study highlights the importance of incorporating the belief uncertainties of uninformed investors in explaining market underreaction in the Bayesian framework.</p>\",\"PeriodicalId\":51552,\"journal\":{\"name\":\"Australian Accounting Review\",\"volume\":\"33 1\",\"pages\":\"66-85\"},\"PeriodicalIF\":3.1000,\"publicationDate\":\"2023-02-21\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://onlinelibrary.wiley.com/doi/epdf/10.1111/auar.12395\",\"citationCount\":\"1\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Australian Accounting Review\",\"FirstCategoryId\":\"91\",\"ListUrlMain\":\"https://onlinelibrary.wiley.com/doi/10.1111/auar.12395\",\"RegionNum\":3,\"RegionCategory\":\"管理学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q2\",\"JCRName\":\"BUSINESS, FINANCE\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Australian Accounting Review","FirstCategoryId":"91","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1111/auar.12395","RegionNum":3,"RegionCategory":"管理学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q2","JCRName":"BUSINESS, FINANCE","Score":null,"Total":0}

Bayesian Investor Belief Updating Speed and Market Underreaction to Earnings Announcements

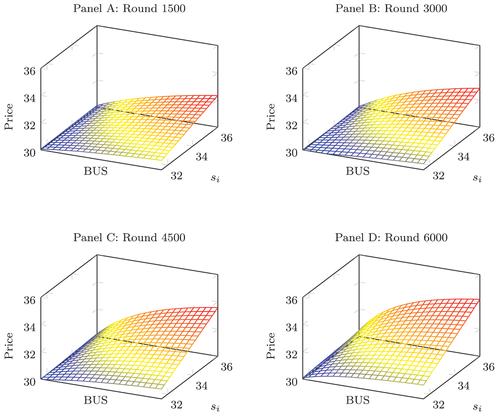

Building on the Bayesian Theorem, we propose a multi-period market microstructure model to understand how Bayesian investors underact new information and the duration of market underreaction. Applying the model to post-earnings-announcement drifts, our simulation and regression analyses show that the duration of the post-announcement price adjustment process and the post-announcement drifts can be explained by the new measure of belief updating speed that quantifies the uncertainties faced by Bayesian investors when incorporating new information into prices. Our study highlights the importance of incorporating the belief uncertainties of uninformed investors in explaining market underreaction in the Bayesian framework.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们