Nupur Moni Das, Bhabani Sankar Rout, Yashmin Khatun

{"title":"G7是否克服了2019冠状病毒病的冲击:对市场波动性的评估?","authors":"Nupur Moni Das, Bhabani Sankar Rout, Yashmin Khatun","doi":"10.1007/s10690-023-09398-8","DOIUrl":null,"url":null,"abstract":"<div><p>The paper has emphasized on the downside potential of the stock market faced by G-7 countries in the times of COVID-19 relative to other economic crises. The results of VaR models, ES, and correlation suggests that most of the nations in G-7 group experienced highest risk during COVID-19 relative to other regimes and also increased inter-linkage of different markets within the group is visible during this period. The work can definitely be a reference to the investors for taking investment decisions as well as the governments and regulators for framing policies to keep the market stable by clinging to the policies of those markets which has managed to stay stable even at turbulent times. Moreover, the group as a whole can also rethink of policy measures together to beat the crisis.</p></div>","PeriodicalId":54095,"journal":{"name":"Asia-Pacific Financial Markets","volume":"30 4","pages":"795 - 816"},"PeriodicalIF":2.6000,"publicationDate":"2023-03-16","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"","citationCount":"3","resultStr":"{\"title\":\"Does G7 Engross the Shock of COVID 19: An Assessment with Market Volatility?\",\"authors\":\"Nupur Moni Das, Bhabani Sankar Rout, Yashmin Khatun\",\"doi\":\"10.1007/s10690-023-09398-8\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<div><p>The paper has emphasized on the downside potential of the stock market faced by G-7 countries in the times of COVID-19 relative to other economic crises. The results of VaR models, ES, and correlation suggests that most of the nations in G-7 group experienced highest risk during COVID-19 relative to other regimes and also increased inter-linkage of different markets within the group is visible during this period. The work can definitely be a reference to the investors for taking investment decisions as well as the governments and regulators for framing policies to keep the market stable by clinging to the policies of those markets which has managed to stay stable even at turbulent times. Moreover, the group as a whole can also rethink of policy measures together to beat the crisis.</p></div>\",\"PeriodicalId\":54095,\"journal\":{\"name\":\"Asia-Pacific Financial Markets\",\"volume\":\"30 4\",\"pages\":\"795 - 816\"},\"PeriodicalIF\":2.6000,\"publicationDate\":\"2023-03-16\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"\",\"citationCount\":\"3\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Asia-Pacific Financial Markets\",\"FirstCategoryId\":\"1085\",\"ListUrlMain\":\"https://link.springer.com/article/10.1007/s10690-023-09398-8\",\"RegionNum\":0,\"RegionCategory\":null,\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q2\",\"JCRName\":\"ECONOMICS\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Asia-Pacific Financial Markets","FirstCategoryId":"1085","ListUrlMain":"https://link.springer.com/article/10.1007/s10690-023-09398-8","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q2","JCRName":"ECONOMICS","Score":null,"Total":0}

Does G7 Engross the Shock of COVID 19: An Assessment with Market Volatility?

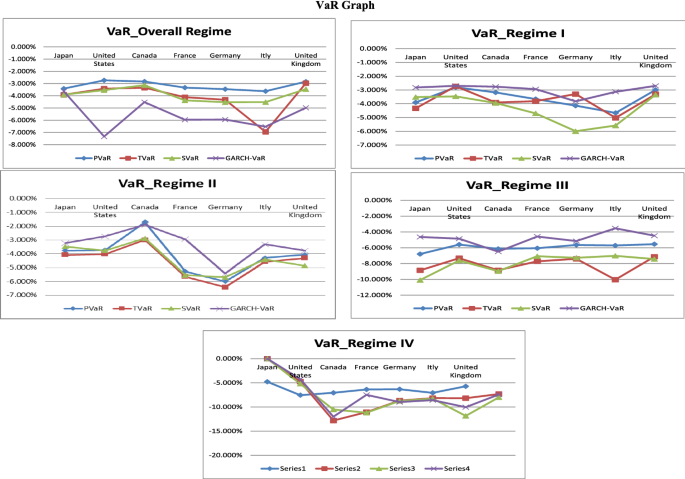

The paper has emphasized on the downside potential of the stock market faced by G-7 countries in the times of COVID-19 relative to other economic crises. The results of VaR models, ES, and correlation suggests that most of the nations in G-7 group experienced highest risk during COVID-19 relative to other regimes and also increased inter-linkage of different markets within the group is visible during this period. The work can definitely be a reference to the investors for taking investment decisions as well as the governments and regulators for framing policies to keep the market stable by clinging to the policies of those markets which has managed to stay stable even at turbulent times. Moreover, the group as a whole can also rethink of policy measures together to beat the crisis.

期刊介绍:

The current remarkable growth in the Asia-Pacific financial markets is certain to continue. These markets are expected to play a further important role in the world capital markets for investment and risk management. In accordance with this development, Asia-Pacific Financial Markets (formerly Financial Engineering and the Japanese Markets), the official journal of the Japanese Association of Financial Econometrics and Engineering (JAFEE), is expected to provide an international forum for researchers and practitioners in academia, industry, and government, who engage in empirical and/or theoretical research into the financial markets. We invite submission of quality papers on all aspects of finance and financial engineering.

Here we interpret the term ''financial engineering'' broadly enough to cover such topics as financial time series, portfolio analysis, global asset allocation, trading strategy for investment, optimization methods, macro monetary economic analysis and pricing models for various financial assets including derivatives We stress that purely theoretical papers, as well as empirical studies that use Asia-Pacific market data, are welcome.

Officially cited as: Asia-Pac Financ Markets

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们