{"title":"股票-债券收益相关性的决定因素","authors":"Ghulam Sarwar","doi":"10.1111/jfir.12329","DOIUrl":null,"url":null,"abstract":"<p>I study the options-implied market risks that affect US stock–bond correlations from 2007 to 2021. I discover that US stock and bond market uncertainty, stock market tail risk, and global credit-default risk are dominant contributors to changing stock–bond correlations during the global financial crisis (GFC) period. However, these market risks collectively contribute much less to time-varying correlations in the post-GFC period. Furthermore, stock–bond correlations rise in times of rising US and global bond market risks. Rising stock market uncertainty raises stock–bond correlations in the GFC period but lowers them in the post-GFC period. My results disentangle the risks of stock and bond markets and show that equity tail risk, bond market risk, and stock market uncertainty are dominant factors in changing stock–bond diversification benefits in periods of market turmoil.</p>","PeriodicalId":47584,"journal":{"name":"Journal of Financial Research","volume":"46 3","pages":"711-732"},"PeriodicalIF":2.1000,"publicationDate":"2023-04-17","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1111/jfir.12329","citationCount":"0","resultStr":"{\"title\":\"The determinants of stock–bond return correlations\",\"authors\":\"Ghulam Sarwar\",\"doi\":\"10.1111/jfir.12329\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>I study the options-implied market risks that affect US stock–bond correlations from 2007 to 2021. I discover that US stock and bond market uncertainty, stock market tail risk, and global credit-default risk are dominant contributors to changing stock–bond correlations during the global financial crisis (GFC) period. However, these market risks collectively contribute much less to time-varying correlations in the post-GFC period. Furthermore, stock–bond correlations rise in times of rising US and global bond market risks. Rising stock market uncertainty raises stock–bond correlations in the GFC period but lowers them in the post-GFC period. My results disentangle the risks of stock and bond markets and show that equity tail risk, bond market risk, and stock market uncertainty are dominant factors in changing stock–bond diversification benefits in periods of market turmoil.</p>\",\"PeriodicalId\":47584,\"journal\":{\"name\":\"Journal of Financial Research\",\"volume\":\"46 3\",\"pages\":\"711-732\"},\"PeriodicalIF\":2.1000,\"publicationDate\":\"2023-04-17\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://onlinelibrary.wiley.com/doi/epdf/10.1111/jfir.12329\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Journal of Financial Research\",\"FirstCategoryId\":\"96\",\"ListUrlMain\":\"https://onlinelibrary.wiley.com/doi/10.1111/jfir.12329\",\"RegionNum\":3,\"RegionCategory\":\"经济学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q3\",\"JCRName\":\"BUSINESS, FINANCE\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Journal of Financial Research","FirstCategoryId":"96","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1111/jfir.12329","RegionNum":3,"RegionCategory":"经济学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q3","JCRName":"BUSINESS, FINANCE","Score":null,"Total":0}

The determinants of stock–bond return correlations

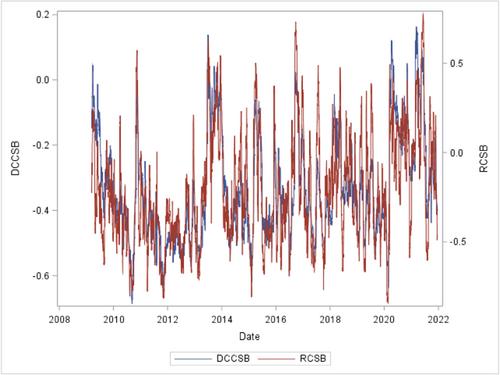

I study the options-implied market risks that affect US stock–bond correlations from 2007 to 2021. I discover that US stock and bond market uncertainty, stock market tail risk, and global credit-default risk are dominant contributors to changing stock–bond correlations during the global financial crisis (GFC) period. However, these market risks collectively contribute much less to time-varying correlations in the post-GFC period. Furthermore, stock–bond correlations rise in times of rising US and global bond market risks. Rising stock market uncertainty raises stock–bond correlations in the GFC period but lowers them in the post-GFC period. My results disentangle the risks of stock and bond markets and show that equity tail risk, bond market risk, and stock market uncertainty are dominant factors in changing stock–bond diversification benefits in periods of market turmoil.

期刊介绍:

The Journal of Financial Research(JFR) is a quarterly academic journal sponsored by the Southern Finance Association (SFA) and the Southwestern Finance Association (SWFA). It has been continuously published since 1978 and focuses on the publication of original scholarly research in various areas of finance such as investment and portfolio management, capital markets and institutions, corporate finance, corporate governance, and capital investment. The JFR, also known as the Journal of Financial Research, provides a platform for researchers to contribute to the advancement of knowledge in the field of finance.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们