{"title":"成本会计信息质量对新冠肺炎疫情与公立医院预算关系的调节作用","authors":"Odysseas Pavlatos, Hara Kostakis","doi":"10.1111/auar.12393","DOIUrl":null,"url":null,"abstract":"<p>Based on new public management, information processing theory and contingency theory, this study investigates the impact of the COVID-19 pandemic on budgeting in public hospitals, focusing on budget use. The research hypotheses were tested using a survey of 82 responses from hospital CFOs. The results show that the organisations that were most affected by the pandemic increased their use of budgets for planning, resource allocation and control, compared to those that were less affected. This study also highlights the moderating role of cost accounting information quality in the relationship between crises and budget use. We find that public hospitals that have been most affected by the pandemic and have simultaneously better cost accounting information have increased their use of budgets for planning, resource allocation and cost control more than those whose costing system does not provide superior cost data.</p>","PeriodicalId":51552,"journal":{"name":"Australian Accounting Review","volume":"33 1","pages":"14-30"},"PeriodicalIF":2.8000,"publicationDate":"2022-12-07","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1111/auar.12393","citationCount":"1","resultStr":"{\"title\":\"Moderating Role of Cost Accounting Information Quality on the Relationship Between the COVID-19 Pandemic and Budgeting in Public Hospitals\",\"authors\":\"Odysseas Pavlatos, Hara Kostakis\",\"doi\":\"10.1111/auar.12393\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>Based on new public management, information processing theory and contingency theory, this study investigates the impact of the COVID-19 pandemic on budgeting in public hospitals, focusing on budget use. The research hypotheses were tested using a survey of 82 responses from hospital CFOs. The results show that the organisations that were most affected by the pandemic increased their use of budgets for planning, resource allocation and control, compared to those that were less affected. This study also highlights the moderating role of cost accounting information quality in the relationship between crises and budget use. We find that public hospitals that have been most affected by the pandemic and have simultaneously better cost accounting information have increased their use of budgets for planning, resource allocation and cost control more than those whose costing system does not provide superior cost data.</p>\",\"PeriodicalId\":51552,\"journal\":{\"name\":\"Australian Accounting Review\",\"volume\":\"33 1\",\"pages\":\"14-30\"},\"PeriodicalIF\":2.8000,\"publicationDate\":\"2022-12-07\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://onlinelibrary.wiley.com/doi/epdf/10.1111/auar.12393\",\"citationCount\":\"1\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Australian Accounting Review\",\"FirstCategoryId\":\"91\",\"ListUrlMain\":\"https://onlinelibrary.wiley.com/doi/10.1111/auar.12393\",\"RegionNum\":3,\"RegionCategory\":\"管理学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q2\",\"JCRName\":\"BUSINESS, FINANCE\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Australian Accounting Review","FirstCategoryId":"91","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1111/auar.12393","RegionNum":3,"RegionCategory":"管理学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q2","JCRName":"BUSINESS, FINANCE","Score":null,"Total":0}

Moderating Role of Cost Accounting Information Quality on the Relationship Between the COVID-19 Pandemic and Budgeting in Public Hospitals

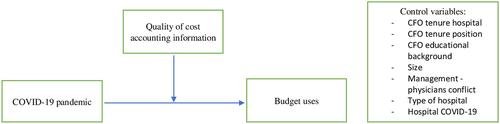

Based on new public management, information processing theory and contingency theory, this study investigates the impact of the COVID-19 pandemic on budgeting in public hospitals, focusing on budget use. The research hypotheses were tested using a survey of 82 responses from hospital CFOs. The results show that the organisations that were most affected by the pandemic increased their use of budgets for planning, resource allocation and control, compared to those that were less affected. This study also highlights the moderating role of cost accounting information quality in the relationship between crises and budget use. We find that public hospitals that have been most affected by the pandemic and have simultaneously better cost accounting information have increased their use of budgets for planning, resource allocation and cost control more than those whose costing system does not provide superior cost data.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们