{"title":"主要环境、社会和治理(ESG)股票指数的动态波动连通性:基于DCC-GARCH模型的证据","authors":"Muneer Shaik, Mohd Ziaur Rehman","doi":"10.1007/s10690-022-09393-5","DOIUrl":null,"url":null,"abstract":"<div><p>This study investigates the dynamic volatility connectivity of important environmental, social, and governance (ESG) stock indexes from May 2010 to March 2021. The empirical research is focused on five major S&P ESG stock indexes from the US, Latin America, Europe, the Middle East and Africa, and Asia Pacific regions. The study reveals that ESG stock indexes in the Middle East Africa, and Latin America are net shock transmitters, whereas the United States and Asia Pacific are net volatility receivers. Furthermore, the study finds that bilateral intercorrelations are higher among US, Latin America, and Europe region group pairs and weaker in relation to Middle East Africa and Asia Pacific region group pairs, indicating the presence of contagion within developed and/or emerging regions, which has relevance for portfolio and risk management.</p></div>","PeriodicalId":54095,"journal":{"name":"Asia-Pacific Financial Markets","volume":"30 1","pages":"231 - 246"},"PeriodicalIF":2.6000,"publicationDate":"2022-10-31","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"","citationCount":"5","resultStr":"{\"title\":\"The Dynamic Volatility Connectedness of Major Environmental, Social, and Governance (ESG) Stock Indices: Evidence Based on DCC-GARCH Model\",\"authors\":\"Muneer Shaik, Mohd Ziaur Rehman\",\"doi\":\"10.1007/s10690-022-09393-5\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<div><p>This study investigates the dynamic volatility connectivity of important environmental, social, and governance (ESG) stock indexes from May 2010 to March 2021. The empirical research is focused on five major S&P ESG stock indexes from the US, Latin America, Europe, the Middle East and Africa, and Asia Pacific regions. The study reveals that ESG stock indexes in the Middle East Africa, and Latin America are net shock transmitters, whereas the United States and Asia Pacific are net volatility receivers. Furthermore, the study finds that bilateral intercorrelations are higher among US, Latin America, and Europe region group pairs and weaker in relation to Middle East Africa and Asia Pacific region group pairs, indicating the presence of contagion within developed and/or emerging regions, which has relevance for portfolio and risk management.</p></div>\",\"PeriodicalId\":54095,\"journal\":{\"name\":\"Asia-Pacific Financial Markets\",\"volume\":\"30 1\",\"pages\":\"231 - 246\"},\"PeriodicalIF\":2.6000,\"publicationDate\":\"2022-10-31\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"\",\"citationCount\":\"5\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Asia-Pacific Financial Markets\",\"FirstCategoryId\":\"1085\",\"ListUrlMain\":\"https://link.springer.com/article/10.1007/s10690-022-09393-5\",\"RegionNum\":0,\"RegionCategory\":null,\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q2\",\"JCRName\":\"ECONOMICS\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Asia-Pacific Financial Markets","FirstCategoryId":"1085","ListUrlMain":"https://link.springer.com/article/10.1007/s10690-022-09393-5","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q2","JCRName":"ECONOMICS","Score":null,"Total":0}

The Dynamic Volatility Connectedness of Major Environmental, Social, and Governance (ESG) Stock Indices: Evidence Based on DCC-GARCH Model

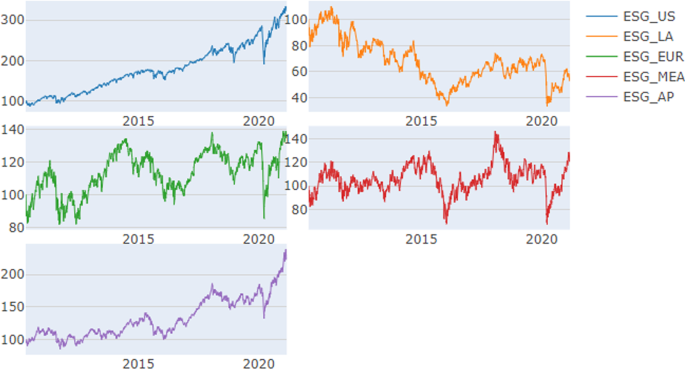

This study investigates the dynamic volatility connectivity of important environmental, social, and governance (ESG) stock indexes from May 2010 to March 2021. The empirical research is focused on five major S&P ESG stock indexes from the US, Latin America, Europe, the Middle East and Africa, and Asia Pacific regions. The study reveals that ESG stock indexes in the Middle East Africa, and Latin America are net shock transmitters, whereas the United States and Asia Pacific are net volatility receivers. Furthermore, the study finds that bilateral intercorrelations are higher among US, Latin America, and Europe region group pairs and weaker in relation to Middle East Africa and Asia Pacific region group pairs, indicating the presence of contagion within developed and/or emerging regions, which has relevance for portfolio and risk management.

期刊介绍:

The current remarkable growth in the Asia-Pacific financial markets is certain to continue. These markets are expected to play a further important role in the world capital markets for investment and risk management. In accordance with this development, Asia-Pacific Financial Markets (formerly Financial Engineering and the Japanese Markets), the official journal of the Japanese Association of Financial Econometrics and Engineering (JAFEE), is expected to provide an international forum for researchers and practitioners in academia, industry, and government, who engage in empirical and/or theoretical research into the financial markets. We invite submission of quality papers on all aspects of finance and financial engineering.

Here we interpret the term ''financial engineering'' broadly enough to cover such topics as financial time series, portfolio analysis, global asset allocation, trading strategy for investment, optimization methods, macro monetary economic analysis and pricing models for various financial assets including derivatives We stress that purely theoretical papers, as well as empirical studies that use Asia-Pacific market data, are welcome.

Officially cited as: Asia-Pac Financ Markets

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们