Aidong Adam Ding, Shaonan Tian, Yan Yu, Xinlei Zhao

{"title":"司法止赎程序是否有助于拖欠次级抵押贷款的借款人?","authors":"Aidong Adam Ding, Shaonan Tian, Yan Yu, Xinlei Zhao","doi":"10.1111/jels.12314","DOIUrl":null,"url":null,"abstract":"<p>We conduct comprehensive analyses on whether and how the judicial foreclosure procedure helps subprime mortgage borrowers to reinstate their delinquent loans outside foreclosure liquidation. Even though the transition rates of various exit types are all higher in non-judicial states, we argue such higher rates can be mechanically driven by the faster shrinking pool of delinquent mortgages in non-judicial states over time. Based on the cumulative proportions of various exit types during a period of up to 5 years post the mortgage first become 90 days past due, we find that judicial states offer more opportunities for delinquent borrowers to reinstate their loans outside foreclosure liquidation, especially during a housing market downturn. Cures, modifications, and paid-offs were all important alternative ways to resolve serious delinquencies during 2007–2008. After modifications became widely available in 2009, loan modifications became the most important alternative for subprime borrowers to reinstate their delinquent mortgages outside foreclosure liquidation. The lion's share of the judicial foreclosure benefit shows up after the start of the foreclosure process.</p>","PeriodicalId":47187,"journal":{"name":"Journal of Empirical Legal Studies","volume":"19 2","pages":"382-422"},"PeriodicalIF":1.3000,"publicationDate":"2022-04-30","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1111/jels.12314","citationCount":"0","resultStr":"{\"title\":\"Does judicial foreclosure procedure help delinquent subprime mortgage borrowers?\",\"authors\":\"Aidong Adam Ding, Shaonan Tian, Yan Yu, Xinlei Zhao\",\"doi\":\"10.1111/jels.12314\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>We conduct comprehensive analyses on whether and how the judicial foreclosure procedure helps subprime mortgage borrowers to reinstate their delinquent loans outside foreclosure liquidation. Even though the transition rates of various exit types are all higher in non-judicial states, we argue such higher rates can be mechanically driven by the faster shrinking pool of delinquent mortgages in non-judicial states over time. Based on the cumulative proportions of various exit types during a period of up to 5 years post the mortgage first become 90 days past due, we find that judicial states offer more opportunities for delinquent borrowers to reinstate their loans outside foreclosure liquidation, especially during a housing market downturn. Cures, modifications, and paid-offs were all important alternative ways to resolve serious delinquencies during 2007–2008. After modifications became widely available in 2009, loan modifications became the most important alternative for subprime borrowers to reinstate their delinquent mortgages outside foreclosure liquidation. The lion's share of the judicial foreclosure benefit shows up after the start of the foreclosure process.</p>\",\"PeriodicalId\":47187,\"journal\":{\"name\":\"Journal of Empirical Legal Studies\",\"volume\":\"19 2\",\"pages\":\"382-422\"},\"PeriodicalIF\":1.3000,\"publicationDate\":\"2022-04-30\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://onlinelibrary.wiley.com/doi/epdf/10.1111/jels.12314\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Journal of Empirical Legal Studies\",\"FirstCategoryId\":\"90\",\"ListUrlMain\":\"https://onlinelibrary.wiley.com/doi/10.1111/jels.12314\",\"RegionNum\":2,\"RegionCategory\":\"社会学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q1\",\"JCRName\":\"LAW\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Journal of Empirical Legal Studies","FirstCategoryId":"90","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1111/jels.12314","RegionNum":2,"RegionCategory":"社会学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q1","JCRName":"LAW","Score":null,"Total":0}

Does judicial foreclosure procedure help delinquent subprime mortgage borrowers?

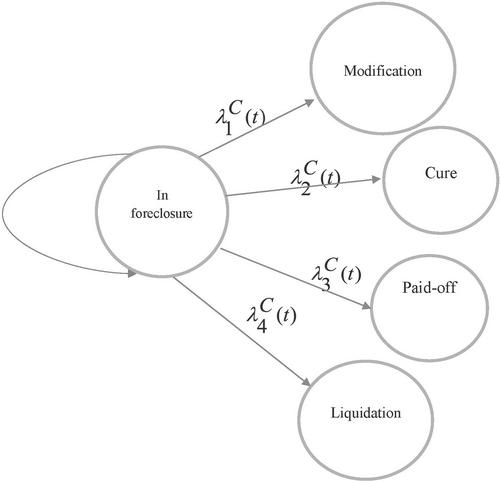

We conduct comprehensive analyses on whether and how the judicial foreclosure procedure helps subprime mortgage borrowers to reinstate their delinquent loans outside foreclosure liquidation. Even though the transition rates of various exit types are all higher in non-judicial states, we argue such higher rates can be mechanically driven by the faster shrinking pool of delinquent mortgages in non-judicial states over time. Based on the cumulative proportions of various exit types during a period of up to 5 years post the mortgage first become 90 days past due, we find that judicial states offer more opportunities for delinquent borrowers to reinstate their loans outside foreclosure liquidation, especially during a housing market downturn. Cures, modifications, and paid-offs were all important alternative ways to resolve serious delinquencies during 2007–2008. After modifications became widely available in 2009, loan modifications became the most important alternative for subprime borrowers to reinstate their delinquent mortgages outside foreclosure liquidation. The lion's share of the judicial foreclosure benefit shows up after the start of the foreclosure process.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们