{"title":"以公民为中心的财务报告翻译:编制者的视角","authors":"Enrico Bracci, Lucia Biondi, Gustaf Kastberg","doi":"10.1111/faam.12298","DOIUrl":null,"url":null,"abstract":"<p>In recent years, the urge to make public sector organizations accountable has resulted in a wide range of citizen-centered financial reporting tools that aim to overcome the limits of traditional financial reporting. To date, the debate on these public accountability innovations has mainly focused on the reasons underpinning their adoption from the users’ perspective, while how preparers affect accountability in the process of constructing such documents is empirically less investigated. By drawing on Callon's concept of translation, this paper aims to analyze how the preparers of citizens-centered financial reports perceive and translate public accountability into practice. In fact, localized translation of public accounting innovation may reveal divergences and ambiguity inherent in the public accountability principles shaped by concurring actors, events, and technologies. The research is qualitative and interpretative, through a longitudinal case study in a municipality, observing the process of construction of a citizen-centered financial reporting tool (i.e., Popular Financial Reporting—PFR). The originality of the paper lies in its contribution to the debate about how public accountability tools are translated into practice by providing evidence of the dynamics that lead an organization along the implementation path. Our findings confirm that the output of the process is the result of the interaction of different networks of interest. Consequently, the final document may vary consistently from the initial project and the general principles of the framework followed.</p>","PeriodicalId":47120,"journal":{"name":"Financial Accountability & Management","volume":"39 1","pages":"18-39"},"PeriodicalIF":2.6000,"publicationDate":"2021-06-03","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://sci-hub-pdf.com/10.1111/faam.12298","citationCount":"7","resultStr":"{\"title\":\"Citizen-centered financial reporting translation: The preparers’ perspective\",\"authors\":\"Enrico Bracci, Lucia Biondi, Gustaf Kastberg\",\"doi\":\"10.1111/faam.12298\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>In recent years, the urge to make public sector organizations accountable has resulted in a wide range of citizen-centered financial reporting tools that aim to overcome the limits of traditional financial reporting. To date, the debate on these public accountability innovations has mainly focused on the reasons underpinning their adoption from the users’ perspective, while how preparers affect accountability in the process of constructing such documents is empirically less investigated. By drawing on Callon's concept of translation, this paper aims to analyze how the preparers of citizens-centered financial reports perceive and translate public accountability into practice. In fact, localized translation of public accounting innovation may reveal divergences and ambiguity inherent in the public accountability principles shaped by concurring actors, events, and technologies. The research is qualitative and interpretative, through a longitudinal case study in a municipality, observing the process of construction of a citizen-centered financial reporting tool (i.e., Popular Financial Reporting—PFR). The originality of the paper lies in its contribution to the debate about how public accountability tools are translated into practice by providing evidence of the dynamics that lead an organization along the implementation path. Our findings confirm that the output of the process is the result of the interaction of different networks of interest. Consequently, the final document may vary consistently from the initial project and the general principles of the framework followed.</p>\",\"PeriodicalId\":47120,\"journal\":{\"name\":\"Financial Accountability & Management\",\"volume\":\"39 1\",\"pages\":\"18-39\"},\"PeriodicalIF\":2.6000,\"publicationDate\":\"2021-06-03\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://sci-hub-pdf.com/10.1111/faam.12298\",\"citationCount\":\"7\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Financial Accountability & Management\",\"FirstCategoryId\":\"1085\",\"ListUrlMain\":\"https://onlinelibrary.wiley.com/doi/10.1111/faam.12298\",\"RegionNum\":0,\"RegionCategory\":null,\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q2\",\"JCRName\":\"BUSINESS, FINANCE\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Financial Accountability & Management","FirstCategoryId":"1085","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1111/faam.12298","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q2","JCRName":"BUSINESS, FINANCE","Score":null,"Total":0}

Citizen-centered financial reporting translation: The preparers’ perspective

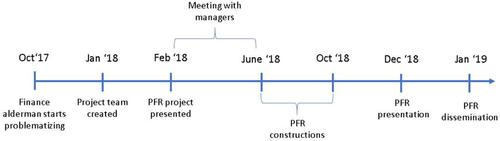

In recent years, the urge to make public sector organizations accountable has resulted in a wide range of citizen-centered financial reporting tools that aim to overcome the limits of traditional financial reporting. To date, the debate on these public accountability innovations has mainly focused on the reasons underpinning their adoption from the users’ perspective, while how preparers affect accountability in the process of constructing such documents is empirically less investigated. By drawing on Callon's concept of translation, this paper aims to analyze how the preparers of citizens-centered financial reports perceive and translate public accountability into practice. In fact, localized translation of public accounting innovation may reveal divergences and ambiguity inherent in the public accountability principles shaped by concurring actors, events, and technologies. The research is qualitative and interpretative, through a longitudinal case study in a municipality, observing the process of construction of a citizen-centered financial reporting tool (i.e., Popular Financial Reporting—PFR). The originality of the paper lies in its contribution to the debate about how public accountability tools are translated into practice by providing evidence of the dynamics that lead an organization along the implementation path. Our findings confirm that the output of the process is the result of the interaction of different networks of interest. Consequently, the final document may vary consistently from the initial project and the general principles of the framework followed.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们