{"title":"股票市场横截面回报与德国商业周期","authors":"Jörg Döpke, Karsten Müller, Lars Tegtmeier","doi":"10.1111/ecno.12219","DOIUrl":null,"url":null,"abstract":"<p>Based on monthly data covering the period from 1987 to 2021, we analyse whether cross-sectional moments of stock market returns may provide information about the future position of the German business cycle. We apply in-sample forecasting regressions with and without leading indicators as control variables, pseudo-out-of-sample exercises, autoregressive distributed lag models, and impulse-response functions estimated by local projections. We find in-sample predictive power of the first and third cross-section moments for the future growth of industrial production, even if one controls for well-established leading indicators for the German business cycle. Out-of-sample tests show that these variables reduce the relative mean squared error compared with benchmark models. We do not find a long-run relation between the moment series and industrial production. The dynamic response of industrial production to a shock on the cross-section moments is in line with the other results.</p>","PeriodicalId":44298,"journal":{"name":"Economic Notes","volume":"52 2","pages":""},"PeriodicalIF":1.4000,"publicationDate":"2023-01-24","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1111/ecno.12219","citationCount":"0","resultStr":"{\"title\":\"Moments of cross-sectional stock market returns and the German business cycle\",\"authors\":\"Jörg Döpke, Karsten Müller, Lars Tegtmeier\",\"doi\":\"10.1111/ecno.12219\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>Based on monthly data covering the period from 1987 to 2021, we analyse whether cross-sectional moments of stock market returns may provide information about the future position of the German business cycle. We apply in-sample forecasting regressions with and without leading indicators as control variables, pseudo-out-of-sample exercises, autoregressive distributed lag models, and impulse-response functions estimated by local projections. We find in-sample predictive power of the first and third cross-section moments for the future growth of industrial production, even if one controls for well-established leading indicators for the German business cycle. Out-of-sample tests show that these variables reduce the relative mean squared error compared with benchmark models. We do not find a long-run relation between the moment series and industrial production. The dynamic response of industrial production to a shock on the cross-section moments is in line with the other results.</p>\",\"PeriodicalId\":44298,\"journal\":{\"name\":\"Economic Notes\",\"volume\":\"52 2\",\"pages\":\"\"},\"PeriodicalIF\":1.4000,\"publicationDate\":\"2023-01-24\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://onlinelibrary.wiley.com/doi/epdf/10.1111/ecno.12219\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Economic Notes\",\"FirstCategoryId\":\"1085\",\"ListUrlMain\":\"https://onlinelibrary.wiley.com/doi/10.1111/ecno.12219\",\"RegionNum\":0,\"RegionCategory\":null,\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q3\",\"JCRName\":\"ECONOMICS\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Economic Notes","FirstCategoryId":"1085","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1111/ecno.12219","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q3","JCRName":"ECONOMICS","Score":null,"Total":0}

Moments of cross-sectional stock market returns and the German business cycle

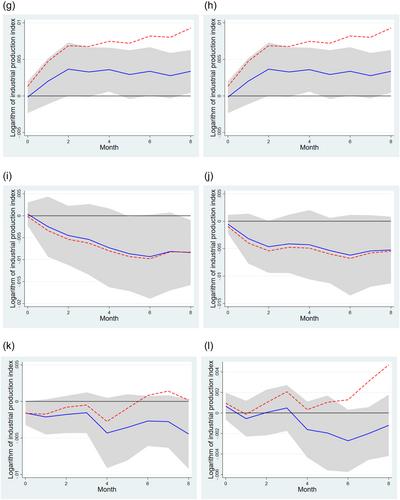

Based on monthly data covering the period from 1987 to 2021, we analyse whether cross-sectional moments of stock market returns may provide information about the future position of the German business cycle. We apply in-sample forecasting regressions with and without leading indicators as control variables, pseudo-out-of-sample exercises, autoregressive distributed lag models, and impulse-response functions estimated by local projections. We find in-sample predictive power of the first and third cross-section moments for the future growth of industrial production, even if one controls for well-established leading indicators for the German business cycle. Out-of-sample tests show that these variables reduce the relative mean squared error compared with benchmark models. We do not find a long-run relation between the moment series and industrial production. The dynamic response of industrial production to a shock on the cross-section moments is in line with the other results.

期刊介绍:

With articles that deal with the latest issues in banking, finance and monetary economics internationally, Economic Notes is an essential resource for anyone in the industry, helping you keep abreast of the latest developments in the field. Articles are written by top economists and executives working in financial institutions, firms and the public sector.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们