Jisma M, Vivek Mohan, Mini Shaji Thomas, Karthik Thirumala

{"title":"使用Rachev比率对P2P交易市场中的清洁能源投资组合进行尾部风险调整","authors":"Jisma M, Vivek Mohan, Mini Shaji Thomas, Karthik Thirumala","doi":"10.1049/enc2.12081","DOIUrl":null,"url":null,"abstract":"<p>Renewable energy sources (RES) and electric vehicles (EVs) pose ‘energy-risk’ in peer energy commitments due to their temporal and spatial uncertainties. Thus, optimistic commitments in the peer-to-peer transactive energy market (P2P TEM) are improbable. This paper proposes a two-stage master–slave portfolio optimization approach for combining energy-risk of RES and EVs, and welfare-risk of peers, in building clean energy portfolios. The master portfolio (MP) refers to the shares of renewable and EVs in P2P market settlement, whereas the slave portfolio (SP) gives the wind-solar mix within renewables. Here, Rachev Ratio (RR), an index used in financial portfolio selection for tail-risk management, is adapted and combined with Markowitz Efficient Frontier (EF) to find the optimal slave portfolio. Both the extreme tails are optimized, encouraging energy outputs far above forecast and discouraging those far below forecast. The master portfolio is obtained by maximizing the sum of the average welfare of the peers at the best (right) and worst (left) tails of the welfare distribution curve using Stochastic Weight Trade-off Particle Swarm Optimization (SWT-PSO). The proposed portfolio selection approach is better in terms of increased expected energy output, improved utilization of RES and EVs, and better collective peer welfare.</p>","PeriodicalId":100467,"journal":{"name":"Energy Conversion and Economics","volume":"4 2","pages":"105-122"},"PeriodicalIF":0.0000,"publicationDate":"2023-03-31","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1049/enc2.12081","citationCount":"0","resultStr":"{\"title\":\"Tail risk adjusted clean energy portfolios in P2P transactive markets using Rachev ratio\",\"authors\":\"Jisma M, Vivek Mohan, Mini Shaji Thomas, Karthik Thirumala\",\"doi\":\"10.1049/enc2.12081\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>Renewable energy sources (RES) and electric vehicles (EVs) pose ‘energy-risk’ in peer energy commitments due to their temporal and spatial uncertainties. Thus, optimistic commitments in the peer-to-peer transactive energy market (P2P TEM) are improbable. This paper proposes a two-stage master–slave portfolio optimization approach for combining energy-risk of RES and EVs, and welfare-risk of peers, in building clean energy portfolios. The master portfolio (MP) refers to the shares of renewable and EVs in P2P market settlement, whereas the slave portfolio (SP) gives the wind-solar mix within renewables. Here, Rachev Ratio (RR), an index used in financial portfolio selection for tail-risk management, is adapted and combined with Markowitz Efficient Frontier (EF) to find the optimal slave portfolio. Both the extreme tails are optimized, encouraging energy outputs far above forecast and discouraging those far below forecast. The master portfolio is obtained by maximizing the sum of the average welfare of the peers at the best (right) and worst (left) tails of the welfare distribution curve using Stochastic Weight Trade-off Particle Swarm Optimization (SWT-PSO). The proposed portfolio selection approach is better in terms of increased expected energy output, improved utilization of RES and EVs, and better collective peer welfare.</p>\",\"PeriodicalId\":100467,\"journal\":{\"name\":\"Energy Conversion and Economics\",\"volume\":\"4 2\",\"pages\":\"105-122\"},\"PeriodicalIF\":0.0000,\"publicationDate\":\"2023-03-31\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://onlinelibrary.wiley.com/doi/epdf/10.1049/enc2.12081\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Energy Conversion and Economics\",\"FirstCategoryId\":\"1085\",\"ListUrlMain\":\"https://onlinelibrary.wiley.com/doi/10.1049/enc2.12081\",\"RegionNum\":0,\"RegionCategory\":null,\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"\",\"JCRName\":\"\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Energy Conversion and Economics","FirstCategoryId":"1085","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1049/enc2.12081","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"","JCRName":"","Score":null,"Total":0}

Tail risk adjusted clean energy portfolios in P2P transactive markets using Rachev ratio

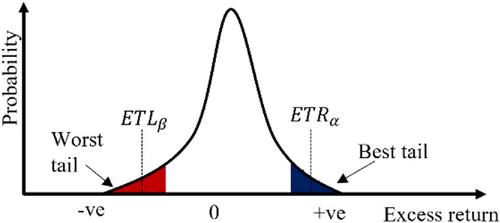

Renewable energy sources (RES) and electric vehicles (EVs) pose ‘energy-risk’ in peer energy commitments due to their temporal and spatial uncertainties. Thus, optimistic commitments in the peer-to-peer transactive energy market (P2P TEM) are improbable. This paper proposes a two-stage master–slave portfolio optimization approach for combining energy-risk of RES and EVs, and welfare-risk of peers, in building clean energy portfolios. The master portfolio (MP) refers to the shares of renewable and EVs in P2P market settlement, whereas the slave portfolio (SP) gives the wind-solar mix within renewables. Here, Rachev Ratio (RR), an index used in financial portfolio selection for tail-risk management, is adapted and combined with Markowitz Efficient Frontier (EF) to find the optimal slave portfolio. Both the extreme tails are optimized, encouraging energy outputs far above forecast and discouraging those far below forecast. The master portfolio is obtained by maximizing the sum of the average welfare of the peers at the best (right) and worst (left) tails of the welfare distribution curve using Stochastic Weight Trade-off Particle Swarm Optimization (SWT-PSO). The proposed portfolio selection approach is better in terms of increased expected energy output, improved utilization of RES and EVs, and better collective peer welfare.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们