Fulvia Pennoni, Francesco Bartolucci, Gianfranco Forte, Ferdinando Ametrano

{"title":"探索主要加密货币日志回报之间的相关性:一个隐马尔可夫模型","authors":"Fulvia Pennoni, Francesco Bartolucci, Gianfranco Forte, Ferdinando Ametrano","doi":"10.1111/ecno.12193","DOIUrl":null,"url":null,"abstract":"<p>A hidden Markov model is proposed for the analysis of time-series of daily log-returns of the last 4 years of Bitcoin, Ethereum, Ripple, Litecoin, and Bitcoin Cash. These log-returns are assumed to have a multivariate Gaussian distribution conditionally on a latent Markov process having a finite number of regimes or states. The hidden regimes represent different market phases identified through distinct vectors of expected values and variance–covariance matrices of the log-returns, so that they also differ in terms of volatility. Maximum-likelihood estimation of the model parameters is carried out by the expectation–maximisation algorithm, and regimes are singularly predicted for every time occasion according to the maximum-a-posteriori rule. Results show three positive and three negative phases of the market. In the most recent period, an increasing tendency towards positive regimes is also predicted. A rather heterogeneous correlation structure is estimated, and evidence of structural medium term trend in the correlation of Bitcoin with the other cryptocurrencies is detected.</p>","PeriodicalId":44298,"journal":{"name":"Economic Notes","volume":"51 1","pages":""},"PeriodicalIF":1.4000,"publicationDate":"2021-11-10","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1111/ecno.12193","citationCount":"3","resultStr":"{\"title\":\"Exploring the dependencies among main cryptocurrency log-returns: A hidden Markov model\",\"authors\":\"Fulvia Pennoni, Francesco Bartolucci, Gianfranco Forte, Ferdinando Ametrano\",\"doi\":\"10.1111/ecno.12193\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>A hidden Markov model is proposed for the analysis of time-series of daily log-returns of the last 4 years of Bitcoin, Ethereum, Ripple, Litecoin, and Bitcoin Cash. These log-returns are assumed to have a multivariate Gaussian distribution conditionally on a latent Markov process having a finite number of regimes or states. The hidden regimes represent different market phases identified through distinct vectors of expected values and variance–covariance matrices of the log-returns, so that they also differ in terms of volatility. Maximum-likelihood estimation of the model parameters is carried out by the expectation–maximisation algorithm, and regimes are singularly predicted for every time occasion according to the maximum-a-posteriori rule. Results show three positive and three negative phases of the market. In the most recent period, an increasing tendency towards positive regimes is also predicted. A rather heterogeneous correlation structure is estimated, and evidence of structural medium term trend in the correlation of Bitcoin with the other cryptocurrencies is detected.</p>\",\"PeriodicalId\":44298,\"journal\":{\"name\":\"Economic Notes\",\"volume\":\"51 1\",\"pages\":\"\"},\"PeriodicalIF\":1.4000,\"publicationDate\":\"2021-11-10\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://onlinelibrary.wiley.com/doi/epdf/10.1111/ecno.12193\",\"citationCount\":\"3\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Economic Notes\",\"FirstCategoryId\":\"1085\",\"ListUrlMain\":\"https://onlinelibrary.wiley.com/doi/10.1111/ecno.12193\",\"RegionNum\":0,\"RegionCategory\":null,\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q3\",\"JCRName\":\"ECONOMICS\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Economic Notes","FirstCategoryId":"1085","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1111/ecno.12193","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q3","JCRName":"ECONOMICS","Score":null,"Total":0}

Exploring the dependencies among main cryptocurrency log-returns: A hidden Markov model

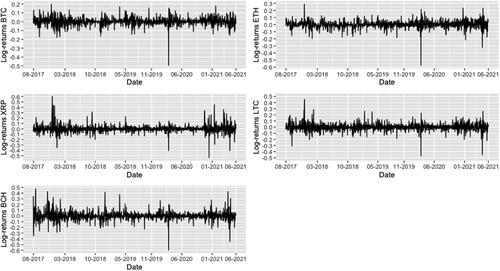

A hidden Markov model is proposed for the analysis of time-series of daily log-returns of the last 4 years of Bitcoin, Ethereum, Ripple, Litecoin, and Bitcoin Cash. These log-returns are assumed to have a multivariate Gaussian distribution conditionally on a latent Markov process having a finite number of regimes or states. The hidden regimes represent different market phases identified through distinct vectors of expected values and variance–covariance matrices of the log-returns, so that they also differ in terms of volatility. Maximum-likelihood estimation of the model parameters is carried out by the expectation–maximisation algorithm, and regimes are singularly predicted for every time occasion according to the maximum-a-posteriori rule. Results show three positive and three negative phases of the market. In the most recent period, an increasing tendency towards positive regimes is also predicted. A rather heterogeneous correlation structure is estimated, and evidence of structural medium term trend in the correlation of Bitcoin with the other cryptocurrencies is detected.

期刊介绍:

With articles that deal with the latest issues in banking, finance and monetary economics internationally, Economic Notes is an essential resource for anyone in the industry, helping you keep abreast of the latest developments in the field. Articles are written by top economists and executives working in financial institutions, firms and the public sector.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们