Meng-Chen Hsieh, Clifford Hurvich, Philippe Soulier

{"title":"在纯跳变过程中对波动的杠杆和长记忆建模","authors":"Meng-Chen Hsieh, Clifford Hurvich, Philippe Soulier","doi":"10.1002/hf2.10042","DOIUrl":null,"url":null,"abstract":"<p>We propose a model for log asset prices in which the underlying transactions and price changes are governed by a marked Cox process. We derive tractable analytical expressions for the autocovariances of the returns, the squared returns, and the covariance of current returns and subsequent squared returns measured at fixed calendar-time frequency. We further prove that statistical properties of the derived return process match the stylized facts observed in empirical financial data such as short memory in returns, long memory in the counts (number of trades), long memory in the realized variance, and the leverage effect. Finally, we provide procedures for estimating the model parameters based on the transaction-level data for a special case of our model.</p>","PeriodicalId":100604,"journal":{"name":"High Frequency","volume":"2 3-4","pages":"124-141"},"PeriodicalIF":0.0000,"publicationDate":"2019-07-02","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://sci-hub-pdf.com/10.1002/hf2.10042","citationCount":"2","resultStr":"{\"title\":\"Modeling leverage and long memory in volatility in a pure-jump process\",\"authors\":\"Meng-Chen Hsieh, Clifford Hurvich, Philippe Soulier\",\"doi\":\"10.1002/hf2.10042\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>We propose a model for log asset prices in which the underlying transactions and price changes are governed by a marked Cox process. We derive tractable analytical expressions for the autocovariances of the returns, the squared returns, and the covariance of current returns and subsequent squared returns measured at fixed calendar-time frequency. We further prove that statistical properties of the derived return process match the stylized facts observed in empirical financial data such as short memory in returns, long memory in the counts (number of trades), long memory in the realized variance, and the leverage effect. Finally, we provide procedures for estimating the model parameters based on the transaction-level data for a special case of our model.</p>\",\"PeriodicalId\":100604,\"journal\":{\"name\":\"High Frequency\",\"volume\":\"2 3-4\",\"pages\":\"124-141\"},\"PeriodicalIF\":0.0000,\"publicationDate\":\"2019-07-02\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://sci-hub-pdf.com/10.1002/hf2.10042\",\"citationCount\":\"2\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"High Frequency\",\"FirstCategoryId\":\"1085\",\"ListUrlMain\":\"https://onlinelibrary.wiley.com/doi/10.1002/hf2.10042\",\"RegionNum\":0,\"RegionCategory\":null,\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"\",\"JCRName\":\"\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"High Frequency","FirstCategoryId":"1085","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1002/hf2.10042","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"","JCRName":"","Score":null,"Total":0}

Modeling leverage and long memory in volatility in a pure-jump process

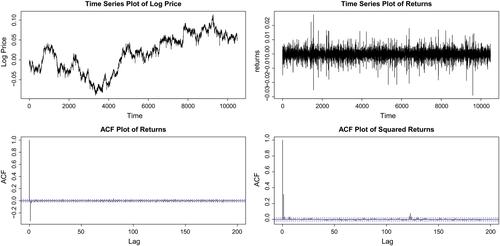

We propose a model for log asset prices in which the underlying transactions and price changes are governed by a marked Cox process. We derive tractable analytical expressions for the autocovariances of the returns, the squared returns, and the covariance of current returns and subsequent squared returns measured at fixed calendar-time frequency. We further prove that statistical properties of the derived return process match the stylized facts observed in empirical financial data such as short memory in returns, long memory in the counts (number of trades), long memory in the realized variance, and the leverage effect. Finally, we provide procedures for estimating the model parameters based on the transaction-level data for a special case of our model.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们