Fan Yang, Tomas Havranek, Zuzana Irsova, Jiri Novak

{"title":"关于对冲基金业绩的研究是否有选择性地发表?定量调查","authors":"Fan Yang, Tomas Havranek, Zuzana Irsova, Jiri Novak","doi":"10.1111/joes.12574","DOIUrl":null,"url":null,"abstract":"<p>We examine whether estimates of hedge fund performance reported in prior empirical research are affected by publication bias. Using a sample of 1019 intercept terms from regressions of hedge fund returns on risk factors (the “alphas”) collected from 74 studies published between 2001 and 2021, we show that the selective publication of empirical results does not significantly contaminate inferences about hedge fund returns. Most of our monthly alpha estimates adjusted for the (small) bias fall within a relatively narrow range of 30–40 basis points, indicating positive abnormal returns of hedge funds: Hedge funds generate money for investors. Studies that explicitly control for potential biases in the underlying data (e.g., backfilling and survivorship biases) report lower but still positive alphas. Our results demonstrate that despite the prevalence of publication selection bias in many other research settings, publication may not be selective when there is no strong a priori theoretical prediction about the sign of the estimated coefficients.</p>","PeriodicalId":51374,"journal":{"name":"Journal of Economic Surveys","volume":"38 4","pages":"1085-1131"},"PeriodicalIF":5.9000,"publicationDate":"2023-06-26","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1111/joes.12574","citationCount":"0","resultStr":"{\"title\":\"Is research on hedge fund performance published selectively? A quantitative survey\",\"authors\":\"Fan Yang, Tomas Havranek, Zuzana Irsova, Jiri Novak\",\"doi\":\"10.1111/joes.12574\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>We examine whether estimates of hedge fund performance reported in prior empirical research are affected by publication bias. Using a sample of 1019 intercept terms from regressions of hedge fund returns on risk factors (the “alphas”) collected from 74 studies published between 2001 and 2021, we show that the selective publication of empirical results does not significantly contaminate inferences about hedge fund returns. Most of our monthly alpha estimates adjusted for the (small) bias fall within a relatively narrow range of 30–40 basis points, indicating positive abnormal returns of hedge funds: Hedge funds generate money for investors. Studies that explicitly control for potential biases in the underlying data (e.g., backfilling and survivorship biases) report lower but still positive alphas. Our results demonstrate that despite the prevalence of publication selection bias in many other research settings, publication may not be selective when there is no strong a priori theoretical prediction about the sign of the estimated coefficients.</p>\",\"PeriodicalId\":51374,\"journal\":{\"name\":\"Journal of Economic Surveys\",\"volume\":\"38 4\",\"pages\":\"1085-1131\"},\"PeriodicalIF\":5.9000,\"publicationDate\":\"2023-06-26\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://onlinelibrary.wiley.com/doi/epdf/10.1111/joes.12574\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Journal of Economic Surveys\",\"FirstCategoryId\":\"96\",\"ListUrlMain\":\"https://onlinelibrary.wiley.com/doi/10.1111/joes.12574\",\"RegionNum\":2,\"RegionCategory\":\"经济学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q1\",\"JCRName\":\"ECONOMICS\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Journal of Economic Surveys","FirstCategoryId":"96","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1111/joes.12574","RegionNum":2,"RegionCategory":"经济学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q1","JCRName":"ECONOMICS","Score":null,"Total":0}

Is research on hedge fund performance published selectively? A quantitative survey

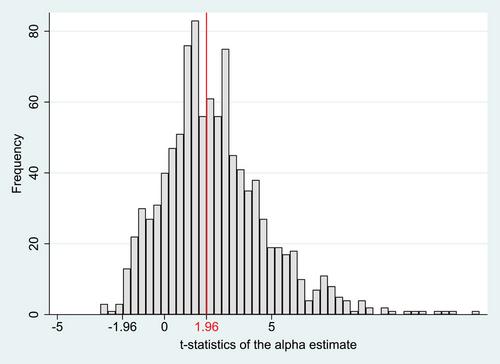

We examine whether estimates of hedge fund performance reported in prior empirical research are affected by publication bias. Using a sample of 1019 intercept terms from regressions of hedge fund returns on risk factors (the “alphas”) collected from 74 studies published between 2001 and 2021, we show that the selective publication of empirical results does not significantly contaminate inferences about hedge fund returns. Most of our monthly alpha estimates adjusted for the (small) bias fall within a relatively narrow range of 30–40 basis points, indicating positive abnormal returns of hedge funds: Hedge funds generate money for investors. Studies that explicitly control for potential biases in the underlying data (e.g., backfilling and survivorship biases) report lower but still positive alphas. Our results demonstrate that despite the prevalence of publication selection bias in many other research settings, publication may not be selective when there is no strong a priori theoretical prediction about the sign of the estimated coefficients.

期刊介绍:

As economics becomes increasingly specialized, communication amongst economists becomes even more important. The Journal of Economic Surveys seeks to improve the communication of new ideas. It provides a means by which economists can keep abreast of recent developments beyond their immediate specialization. Areas covered include: - economics - econometrics - economic history - business economics

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们