{"title":"气候监管成本与企业困境风险","authors":"Neophytos Lambertides, Dimitris Tsouknidis","doi":"10.1111/fmii.12184","DOIUrl":null,"url":null,"abstract":"<p>In 2013, the European Union's Emission Trading Scheme (EU-ETS) entered Phase III. The majority of emission permits in Phase III are auctioned instead of being allocated for free as in Phases I and II. Using a difference-in-differences method, we show that this change has led to an increase in the financial distress risk of the EU-ETS-regulated firms when compared to unregulated firms, suggesting that the EU-ETS imposes a significant financial burden on regulated firms. This result is robust to an array of validation tests, alleviating concerns that it is driven by unobserved factors. In additional analyses we show that the increase in distress risk of regulated firms during Phase III can be explained by, (i) an additional climate regulation cost to purchase pollution permits and (ii) a low average environmental score that possibly (via high sustainability risk) lowers investors expectations regarding firms’ performance. Our findings also show that the distress risk increase is higher for regulated firms operating within countries with lower control of corruption, government effectiveness, political stability, regulatory quality, rule of law, and voice accountability before the EU-ETS implementation.</p>","PeriodicalId":39670,"journal":{"name":"Financial Markets, Institutions and Instruments","volume":"33 1","pages":"3-30"},"PeriodicalIF":0.0000,"publicationDate":"2023-08-27","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1111/fmii.12184","citationCount":"0","resultStr":"{\"title\":\"Climate regulation costs and firms’ distress risk\",\"authors\":\"Neophytos Lambertides, Dimitris Tsouknidis\",\"doi\":\"10.1111/fmii.12184\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>In 2013, the European Union's Emission Trading Scheme (EU-ETS) entered Phase III. The majority of emission permits in Phase III are auctioned instead of being allocated for free as in Phases I and II. Using a difference-in-differences method, we show that this change has led to an increase in the financial distress risk of the EU-ETS-regulated firms when compared to unregulated firms, suggesting that the EU-ETS imposes a significant financial burden on regulated firms. This result is robust to an array of validation tests, alleviating concerns that it is driven by unobserved factors. In additional analyses we show that the increase in distress risk of regulated firms during Phase III can be explained by, (i) an additional climate regulation cost to purchase pollution permits and (ii) a low average environmental score that possibly (via high sustainability risk) lowers investors expectations regarding firms’ performance. Our findings also show that the distress risk increase is higher for regulated firms operating within countries with lower control of corruption, government effectiveness, political stability, regulatory quality, rule of law, and voice accountability before the EU-ETS implementation.</p>\",\"PeriodicalId\":39670,\"journal\":{\"name\":\"Financial Markets, Institutions and Instruments\",\"volume\":\"33 1\",\"pages\":\"3-30\"},\"PeriodicalIF\":0.0000,\"publicationDate\":\"2023-08-27\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://onlinelibrary.wiley.com/doi/epdf/10.1111/fmii.12184\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Financial Markets, Institutions and Instruments\",\"FirstCategoryId\":\"1085\",\"ListUrlMain\":\"https://onlinelibrary.wiley.com/doi/10.1111/fmii.12184\",\"RegionNum\":0,\"RegionCategory\":null,\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q1\",\"JCRName\":\"Economics, Econometrics and Finance\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Financial Markets, Institutions and Instruments","FirstCategoryId":"1085","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1111/fmii.12184","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q1","JCRName":"Economics, Econometrics and Finance","Score":null,"Total":0}

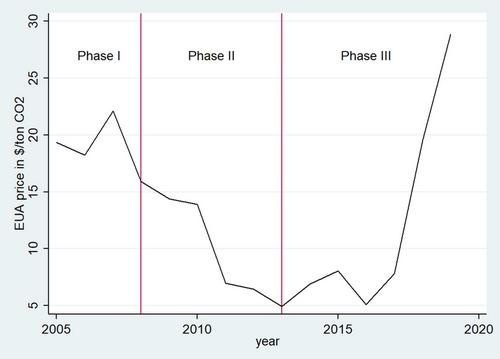

In 2013, the European Union's Emission Trading Scheme (EU-ETS) entered Phase III. The majority of emission permits in Phase III are auctioned instead of being allocated for free as in Phases I and II. Using a difference-in-differences method, we show that this change has led to an increase in the financial distress risk of the EU-ETS-regulated firms when compared to unregulated firms, suggesting that the EU-ETS imposes a significant financial burden on regulated firms. This result is robust to an array of validation tests, alleviating concerns that it is driven by unobserved factors. In additional analyses we show that the increase in distress risk of regulated firms during Phase III can be explained by, (i) an additional climate regulation cost to purchase pollution permits and (ii) a low average environmental score that possibly (via high sustainability risk) lowers investors expectations regarding firms’ performance. Our findings also show that the distress risk increase is higher for regulated firms operating within countries with lower control of corruption, government effectiveness, political stability, regulatory quality, rule of law, and voice accountability before the EU-ETS implementation.

期刊介绍:

Financial Markets, Institutions and Instruments bridges the gap between the academic and professional finance communities. With contributions from leading academics, as well as practitioners from organizations such as the SEC and the Federal Reserve, the journal is equally relevant to both groups. Each issue is devoted to a single topic, which is examined in depth, and a special fifth issue is published annually highlighting the most significant developments in money and banking, derivative securities, corporate finance, and fixed-income securities.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们