{"title":"新兴股票市场的部门整合:多尺度方法。","authors":"Kingstone Nyakurukwa, Yudhvir Seetharam","doi":"10.1007/s11403-023-00383-y","DOIUrl":null,"url":null,"abstract":"<p><p>The purpose of this study is to examine the connectedness of industry sectors on the Johannesburg Stock Exchange in a time-frequency domain. We use econophysics-based methods like the wavelet multiple correlation and wavelet scalogram difference to identify the evolution of the connectedness of the sectors over time and at different frequencies. The findings show that the sectors on the Johannesburg Stock Exchange are especially integrated at lower frequencies. Wavelet multiple correlation peaks in response to local and global shocks like the black-swan COVID-19 pandemic in 2020 and the downgrading of South African debt by Fitch in 2013. Though there are opportunities for sectoral diversification on the JSE, this fails when it is most needed, during crisis periods. Investors should therefore consider other asset classes that could serve as a haven in times of crisis. Though extant literature has examined sectoral dependencies on the stock markets of developed and developing countries, to the best of our knowledge, this is the first study to examine this connectedness in a South African context using multiple nonparametric methods that are robust to non-normality, presence of outliers as well as non-stationary data.</p>","PeriodicalId":45479,"journal":{"name":"Journal of Economic Interaction and Coordination","volume":" ","pages":"1-20"},"PeriodicalIF":1.0000,"publicationDate":"2023-04-13","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://www.ncbi.nlm.nih.gov/pmc/articles/PMC10099005/pdf/","citationCount":"0","resultStr":"{\"title\":\"Sectoral integration on an emerging stock market: a multi-scale approach.\",\"authors\":\"Kingstone Nyakurukwa, Yudhvir Seetharam\",\"doi\":\"10.1007/s11403-023-00383-y\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p><p>The purpose of this study is to examine the connectedness of industry sectors on the Johannesburg Stock Exchange in a time-frequency domain. We use econophysics-based methods like the wavelet multiple correlation and wavelet scalogram difference to identify the evolution of the connectedness of the sectors over time and at different frequencies. The findings show that the sectors on the Johannesburg Stock Exchange are especially integrated at lower frequencies. Wavelet multiple correlation peaks in response to local and global shocks like the black-swan COVID-19 pandemic in 2020 and the downgrading of South African debt by Fitch in 2013. Though there are opportunities for sectoral diversification on the JSE, this fails when it is most needed, during crisis periods. Investors should therefore consider other asset classes that could serve as a haven in times of crisis. Though extant literature has examined sectoral dependencies on the stock markets of developed and developing countries, to the best of our knowledge, this is the first study to examine this connectedness in a South African context using multiple nonparametric methods that are robust to non-normality, presence of outliers as well as non-stationary data.</p>\",\"PeriodicalId\":45479,\"journal\":{\"name\":\"Journal of Economic Interaction and Coordination\",\"volume\":\" \",\"pages\":\"1-20\"},\"PeriodicalIF\":1.0000,\"publicationDate\":\"2023-04-13\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://www.ncbi.nlm.nih.gov/pmc/articles/PMC10099005/pdf/\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Journal of Economic Interaction and Coordination\",\"FirstCategoryId\":\"96\",\"ListUrlMain\":\"https://doi.org/10.1007/s11403-023-00383-y\",\"RegionNum\":4,\"RegionCategory\":\"经济学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q3\",\"JCRName\":\"ECONOMICS\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Journal of Economic Interaction and Coordination","FirstCategoryId":"96","ListUrlMain":"https://doi.org/10.1007/s11403-023-00383-y","RegionNum":4,"RegionCategory":"经济学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q3","JCRName":"ECONOMICS","Score":null,"Total":0}

Sectoral integration on an emerging stock market: a multi-scale approach.

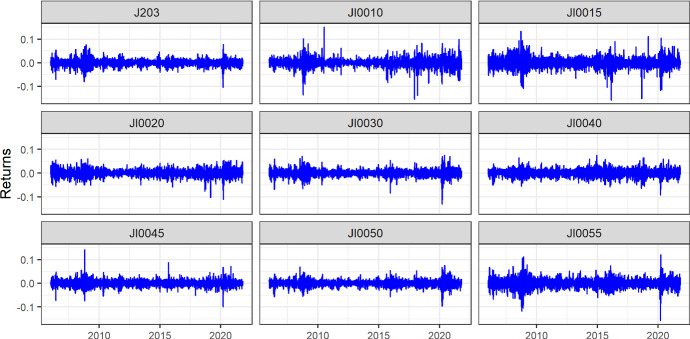

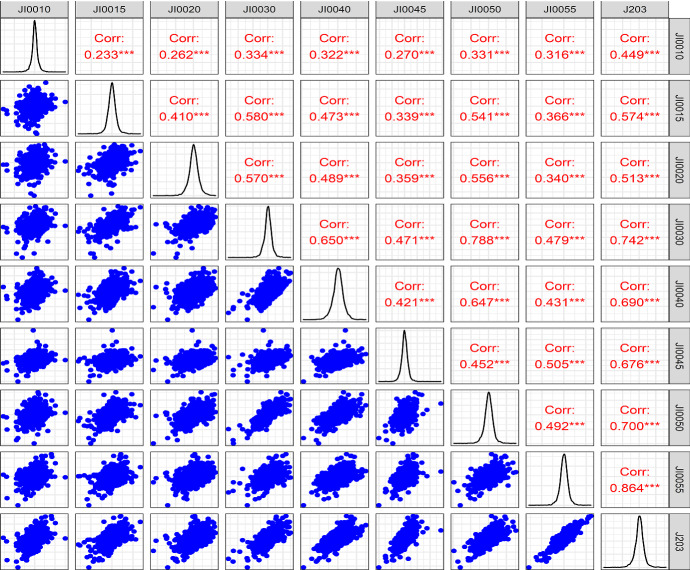

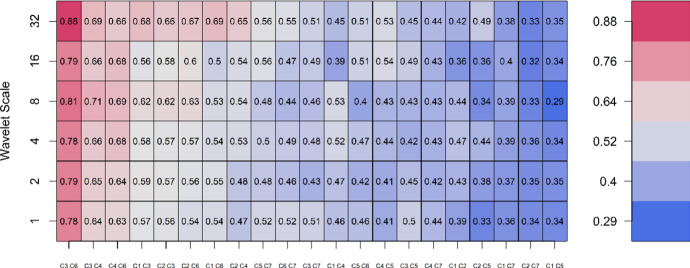

The purpose of this study is to examine the connectedness of industry sectors on the Johannesburg Stock Exchange in a time-frequency domain. We use econophysics-based methods like the wavelet multiple correlation and wavelet scalogram difference to identify the evolution of the connectedness of the sectors over time and at different frequencies. The findings show that the sectors on the Johannesburg Stock Exchange are especially integrated at lower frequencies. Wavelet multiple correlation peaks in response to local and global shocks like the black-swan COVID-19 pandemic in 2020 and the downgrading of South African debt by Fitch in 2013. Though there are opportunities for sectoral diversification on the JSE, this fails when it is most needed, during crisis periods. Investors should therefore consider other asset classes that could serve as a haven in times of crisis. Though extant literature has examined sectoral dependencies on the stock markets of developed and developing countries, to the best of our knowledge, this is the first study to examine this connectedness in a South African context using multiple nonparametric methods that are robust to non-normality, presence of outliers as well as non-stationary data.

期刊介绍:

Journal of Economic Interaction and Coordination addresses the vibrant and interdisciplinary field of agent-based approaches to economics and social sciences.

It focuses on simulating and synthesizing emergent phenomena and collective behavior in order to understand economic and social systems. Relevant topics include, but are not limited to, the following: markets as complex adaptive systems, multi-agents in economics, artificial markets with heterogeneous agents, financial markets with heterogeneous agents, theory and simulation of agent-based models, adaptive agents with artificial intelligence, interacting particle systems in economics, social and complex networks, econophysics, non-linear economic dynamics, evolutionary games, market mechanisms in distributed computing systems, experimental economics, collective decisions.

Contributions are mostly from economics, physics, computer science and related fields and are typically based on sound theoretical models and supported by experimental validation. Survey papers are also welcome.

Journal of Economic Interaction and Coordination is the official journal of the Association of Economic Science with Heterogeneous Interacting Agents.

Officially cited as: J Econ Interact Coord

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们