{"title":"非人寿保险的最低资本要求和投资组合分配:具有条件风险价值(CVaR)约束的半参数模型。","authors":"Alessandro Staino, Emilio Russo, Massimo Costabile, Arturo Leccadito","doi":"10.1007/s10287-023-00439-1","DOIUrl":null,"url":null,"abstract":"<p><p>We present an optimization problem to determine the minimum capital requirement for a non-life insurance company. The optimization problem imposes a non-positive Conditional Value-at-Risk (CVaR) of the insurer's net loss and a portfolio performance constraint. When expressing the optimization problem in a semiparametric form, we demonstrate its convexity for any integrable random variable representing the insurer's liability. Furthermore, we prove that the function defining the CVaR constraint in the semiparametric formulation is continuously differentiable when the insurer's liability has a continuous distribution. We use the Kelley-Cheney-Goldstein algorithm to solve the optimization problem in the semiparametric form and show its convergence. An empirical analysis is carried out by assuming three different liability distributions: a lognormal distribution, a gamma distribution, and a mixture of Erlang distributions with a common scale parameter. The numerical experiments show that the choice of the liability distribution plays a crucial role since marked differences emerge when comparing the mixture distribution with the other two distributions. In particular, the mixture distribution describes better the right tail of the empirical distribution of liabilities with respect to the other two distributions and implies higher capital requirements and different assets in the optimal portfolios.</p>","PeriodicalId":46743,"journal":{"name":"Computational Management Science","volume":"20 1","pages":"12"},"PeriodicalIF":1.3000,"publicationDate":"2023-01-01","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://www.ncbi.nlm.nih.gov/pmc/articles/PMC9982813/pdf/","citationCount":"0","resultStr":"{\"title\":\"Minimum capital requirement and portfolio allocation for non-life insurance: a semiparametric model with Conditional Value-at-Risk (CVaR) constraint.\",\"authors\":\"Alessandro Staino, Emilio Russo, Massimo Costabile, Arturo Leccadito\",\"doi\":\"10.1007/s10287-023-00439-1\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p><p>We present an optimization problem to determine the minimum capital requirement for a non-life insurance company. The optimization problem imposes a non-positive Conditional Value-at-Risk (CVaR) of the insurer's net loss and a portfolio performance constraint. When expressing the optimization problem in a semiparametric form, we demonstrate its convexity for any integrable random variable representing the insurer's liability. Furthermore, we prove that the function defining the CVaR constraint in the semiparametric formulation is continuously differentiable when the insurer's liability has a continuous distribution. We use the Kelley-Cheney-Goldstein algorithm to solve the optimization problem in the semiparametric form and show its convergence. An empirical analysis is carried out by assuming three different liability distributions: a lognormal distribution, a gamma distribution, and a mixture of Erlang distributions with a common scale parameter. The numerical experiments show that the choice of the liability distribution plays a crucial role since marked differences emerge when comparing the mixture distribution with the other two distributions. In particular, the mixture distribution describes better the right tail of the empirical distribution of liabilities with respect to the other two distributions and implies higher capital requirements and different assets in the optimal portfolios.</p>\",\"PeriodicalId\":46743,\"journal\":{\"name\":\"Computational Management Science\",\"volume\":\"20 1\",\"pages\":\"12\"},\"PeriodicalIF\":1.3000,\"publicationDate\":\"2023-01-01\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://www.ncbi.nlm.nih.gov/pmc/articles/PMC9982813/pdf/\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Computational Management Science\",\"FirstCategoryId\":\"1085\",\"ListUrlMain\":\"https://doi.org/10.1007/s10287-023-00439-1\",\"RegionNum\":0,\"RegionCategory\":null,\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"2023/3/3 0:00:00\",\"PubModel\":\"Epub\",\"JCR\":\"Q3\",\"JCRName\":\"SOCIAL SCIENCES, MATHEMATICAL METHODS\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Computational Management Science","FirstCategoryId":"1085","ListUrlMain":"https://doi.org/10.1007/s10287-023-00439-1","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"2023/3/3 0:00:00","PubModel":"Epub","JCR":"Q3","JCRName":"SOCIAL SCIENCES, MATHEMATICAL METHODS","Score":null,"Total":0}

Minimum capital requirement and portfolio allocation for non-life insurance: a semiparametric model with Conditional Value-at-Risk (CVaR) constraint.

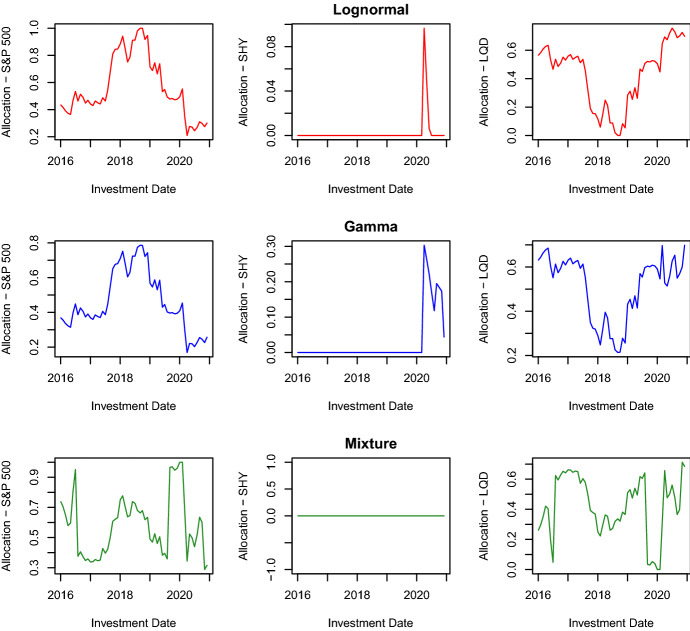

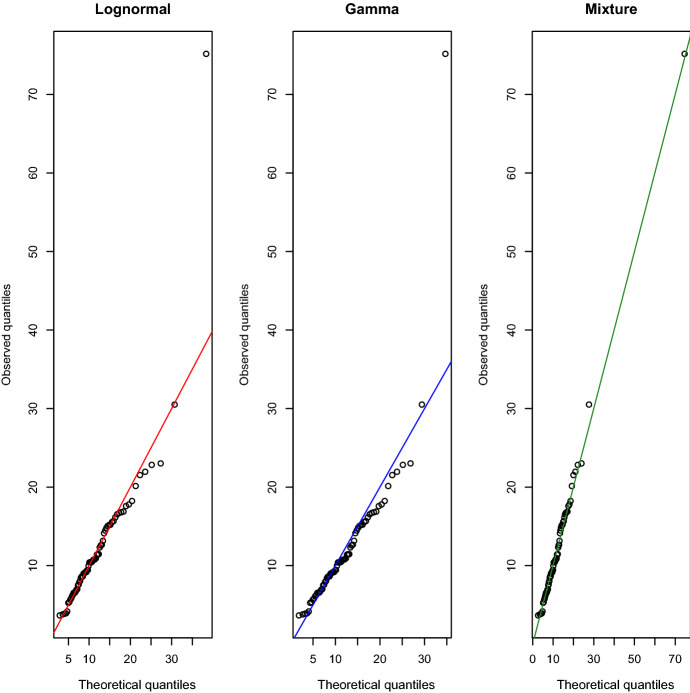

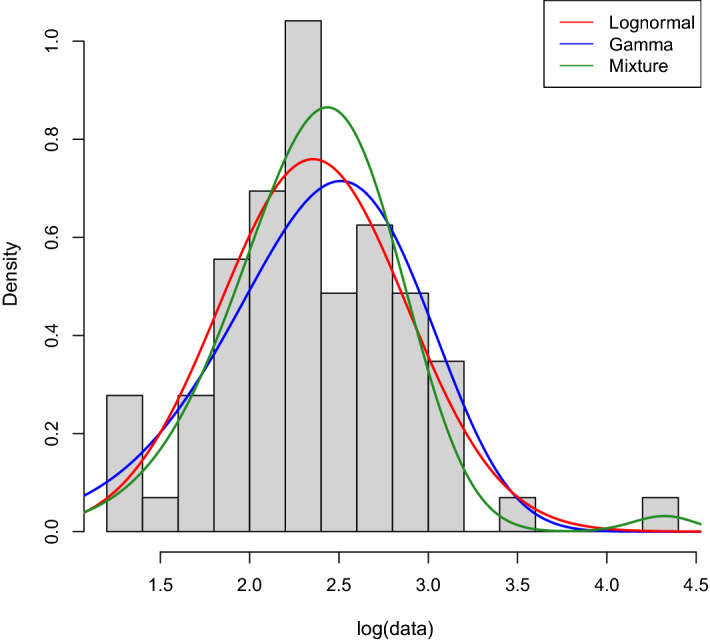

We present an optimization problem to determine the minimum capital requirement for a non-life insurance company. The optimization problem imposes a non-positive Conditional Value-at-Risk (CVaR) of the insurer's net loss and a portfolio performance constraint. When expressing the optimization problem in a semiparametric form, we demonstrate its convexity for any integrable random variable representing the insurer's liability. Furthermore, we prove that the function defining the CVaR constraint in the semiparametric formulation is continuously differentiable when the insurer's liability has a continuous distribution. We use the Kelley-Cheney-Goldstein algorithm to solve the optimization problem in the semiparametric form and show its convergence. An empirical analysis is carried out by assuming three different liability distributions: a lognormal distribution, a gamma distribution, and a mixture of Erlang distributions with a common scale parameter. The numerical experiments show that the choice of the liability distribution plays a crucial role since marked differences emerge when comparing the mixture distribution with the other two distributions. In particular, the mixture distribution describes better the right tail of the empirical distribution of liabilities with respect to the other two distributions and implies higher capital requirements and different assets in the optimal portfolios.

期刊介绍:

Computational Management Science (CMS) is an international journal focusing on all computational aspects of management science. These include theoretical and empirical analysis of computational models; computational statistics; analysis and applications of constrained, unconstrained, robust, stochastic and combinatorial optimisation algorithms; dynamic models, such as dynamic programming and decision trees; new search tools and algorithms for global optimisation, modelling, learning and forecasting; models and tools of knowledge acquisition.

The emphasis on computational paradigms is an intended feature of CMS, distinguishing it from more classical operations research journals.

Officially cited as: Comput Manag Sci

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们