{"title":"Monetary Policy and Mispricing in Stock Markets","authors":"BENJAMIN BECKERS, KERSTIN BERNOTH","doi":"10.1111/jmcb.13090","DOIUrl":null,"url":null,"abstract":"<p>We investigate the role of monetary policy in stock price misalignments and explore whether central banks can attenuate excessive mispricing as suggested by the proponents of a “leaning against the wind” monetary policy. Decomposing stock prices into expected excess dividends, an equity risk premium, and a mispricing component, we find that prices fall more strongly in response to an increase in the policy rate than what is implied by their underlying fundamentals. This systematic overreaction suggests that tighter monetary policy may contain emerging asset price misalignments. Our findings are at odds with the predictions of a rational bubble framework, but can be explained by mispricing arising from false subjective expectations of irrational investors.</p>","PeriodicalId":48328,"journal":{"name":"Journal of Money Credit and Banking","volume":"56 7","pages":"1887-1904"},"PeriodicalIF":1.6000,"publicationDate":"2023-09-25","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1111/jmcb.13090","citationCount":"0","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"Journal of Money Credit and Banking","FirstCategoryId":"96","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1111/jmcb.13090","RegionNum":3,"RegionCategory":"经济学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q3","JCRName":"BUSINESS, FINANCE","Score":null,"Total":0}

引用次数: 0

Abstract

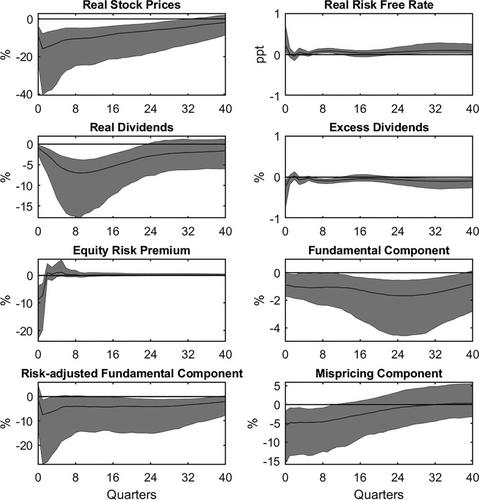

We investigate the role of monetary policy in stock price misalignments and explore whether central banks can attenuate excessive mispricing as suggested by the proponents of a “leaning against the wind” monetary policy. Decomposing stock prices into expected excess dividends, an equity risk premium, and a mispricing component, we find that prices fall more strongly in response to an increase in the policy rate than what is implied by their underlying fundamentals. This systematic overreaction suggests that tighter monetary policy may contain emerging asset price misalignments. Our findings are at odds with the predictions of a rational bubble framework, but can be explained by mispricing arising from false subjective expectations of irrational investors.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们